There is a wide variety of high income stocks, and they are not all created equally. Far too often, investors make the unfortunate mistake of blindly chasing after the highest yielding stocks without realizing many of them are simply value traps. For example, what good is it to buy a stock with a 10% yield if the price declines by 20% every year? And while many of the highest yielding stocks today are simply slowly dying businesses (e.g. value traps), there are plenty of diamonds in the rough, especially when you consider the important concepts of total return and yield on cost (i.e. dividend growth). In this article, we rank our top 10 high-income stocks, starting with #10 and counting down to our #1 top idea.

Dividend Yield Versus Total Return

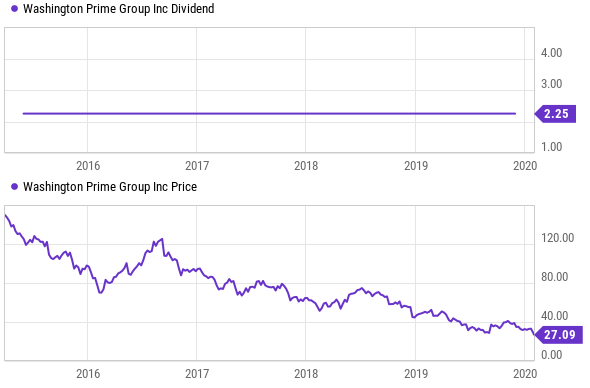

Before we get into the countdown, it’s worth reviewing the concept of total return. Total return is the combination of price gains (or losses) and income (from dividends). For perspective, here is a look at the historical big dividend and share price of once popular retail property REIT, Washington Prime Group (WPG). As you can see, WPG paid a huge $2.25 quarterly dividend that attracted many income-hungry investors for years.

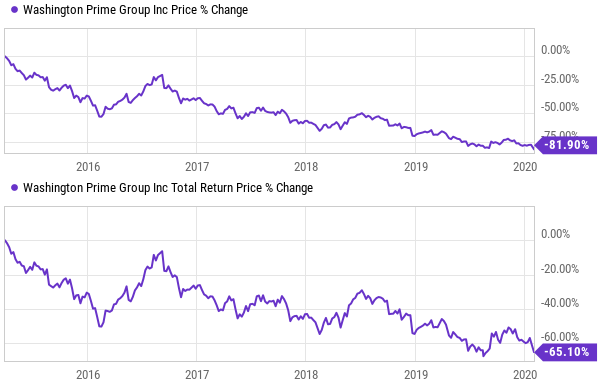

Unfortunately, as you can see in the price chart, the big dividend payments were more than offset by the ugly price decline of the shares. And in aggregate, even though WPG kept paying that big dividend for years, the “total return” (see chart below) was VERY negative over this time period.

Washington Prime Group is an example of an ugly value trap that many unfortunate investors lost a lot of money on. Further, the company eliminated its dividend altogether last year as it simply didn’t have the cash to pay it. WPG is a good example of why even income-focused investors need to be aware of total returns, instead of just blindly chasing after the highest current yields.

Dividend Growth and Yield on Cost

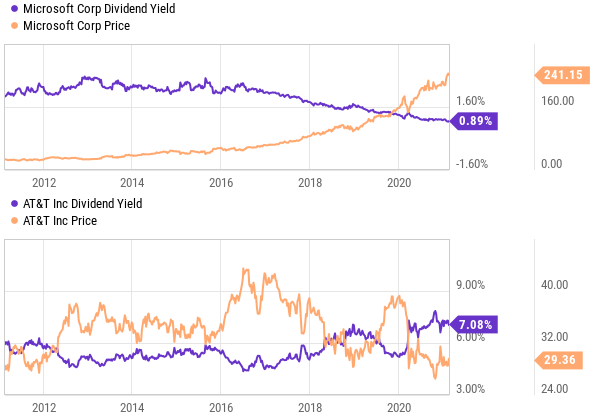

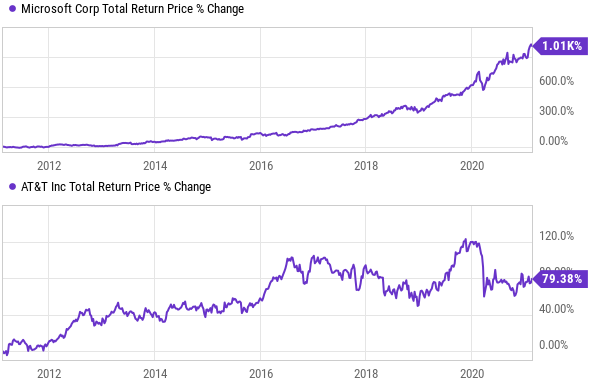

Dividend growth is another important concept for long-term income-focused investors to know because if you are not paying attention—you could overlook A LOT of income opportunities. Specifically, sometimes it is better to buy a lower dividend yield stock, if the dividend payment is growing, because in the long-term you’ll receive MORE INCOME—AND a better total return. We get into more specific examples of this later in the report, but to help you conceptualize, take a look at Microsoft (MSFT) a lower dividend yield stock versus AT&T (T) a very popular higher dividend yield stock.

Specifically, 10 years ago, both AT&T and Microsoft traded at around $26 per share, but AT&T offered a dividend yield of around 6.0%, whereas Microsoft’s was only around 2.2%. However, as you can see in the follow chart, Microsoft’s dividend payment has grow faster, and if you purchased both stocks 10 years ago—Microsoft’s current “yield on cost” is HIGHER than AT&T’s

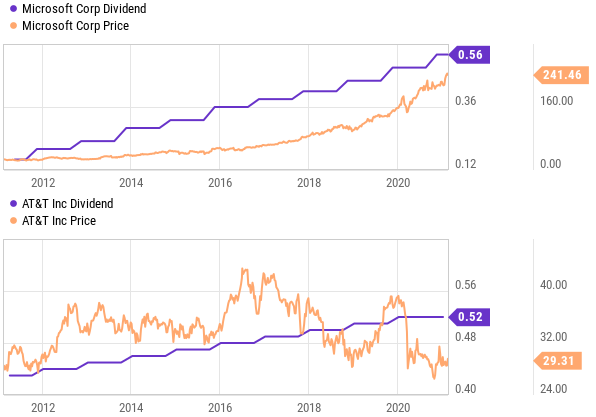

The point here is that investors should not overlook the massive long-term income potential of dividend growth stocks. If you chose to spend your $26 back in 2011 on a share of Microsoft instead of AT&T, you’d actually be receiving a bigger dividend payment today, and you’d also have earned a much much much bigger total return (see chart below).

You personally need to always balance your near-term and long-term needs for income with careful consideration to avoid value traps, optimize total returns and not overlook the amazing power of long-term dividend growth.

Top 10 High Income Stocks

With that backdrop in mind, let’s get into our top 10 countdown. Without further ado, here is our ranking, starting with #10 and counting down to our #1 top idea.

10. PIMCO Income Opportunity (PKO), Yield: 8.9%

The PIMCO Income Opportunity Fund is an attractive closed-end fund considering its big monthly dividend payments, strong and experienced management team, and even its potential for some price appreciation too. It invests in a diversified portfolio of fixed income securities (mostly corporate bonds), prudently uses some leverage, and has continued to pay steady income since its inception in 2007, despite the market’s many ups and downs.

You can get all the latest data and metrics on this one at CEF Connect (here), and you can read our previous full report for our detailed thesis, here:

9. Altria (MO), Yield: 7.9%

Altria Group Inc. (MO) is one of the world’s largest manufacturer and seller of cigarettes, tobacco and related products. Altria is structured as a holding company, and operates via its subsidiaries - Philip Morris USA, U.S. Smokeless Tobacco Company, John Middleton Co., Ste. Michelle Wine Estates Ltd. and Philip Morris Capital Corporation. The company also has a 10% equity stake in Anheuser-Busch InBev (BUD), a 35% stake in e-cigarette maker JUUL (JUUL), and a 45% stake in the cannabis company Cronos Group (CRON). Some of its major brands include Marlboro, Black & Mild, Copenhagen, Skoal.

Altria has a very healthy dividend (with over 50 years of dividend increases), and the shares have significantly less volatility risk than the rest of the market (as per its 0.6, 3-year beta). Furthermore, we like the company’s aggressive share repurchase program. You can read our full write-up on Altria here:

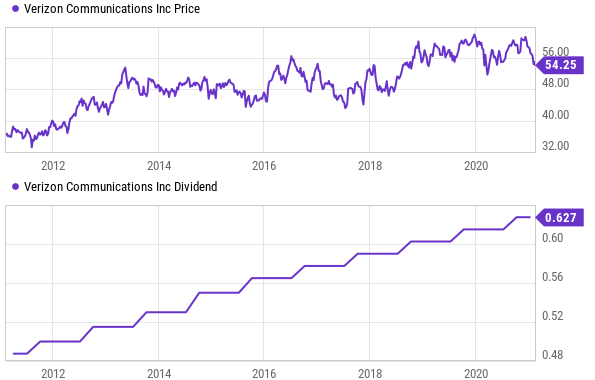

8b. Verizon (VZ), Yield: 4.6%

Verizon’s relative strength comes from the scale of its wireless business, which has positioned it on strong footing as compared to its rivals. And we believe that because of its largely resilient business model with a recurring revenue stream, the company should be able to generate robust free cash flows in the future, thereby strengthening regular dividend payouts. Also, there is plenty of room for dividend growth given that Verizon currently pays just over half of its free cash flows in dividends.

Accordingly, we believe the stock is worth considering if you are a long-term, income-focused investor. You can access our previous full report on Verizon here:

8a. Pfizer (PFE), Yield: 4.5%

The 4.3% dividend yield of mega-cap pharmaceutical company Pfizer (PFE) is worth a closer look. Specifically, its return on capital is above its cost of capital (a good thing), its margins should increase as a result of the Upjohn spinoff, its covid vaccine is in addition to an already strong core business, it’s paid 328 consecutive quarterly dividend (and has increased the dividend 11 years straight), and the share price just dipped.

If you are looking for a healthy growing big dividend, Pfizer’s is worth considering. You can access our full report on Pfizer here:

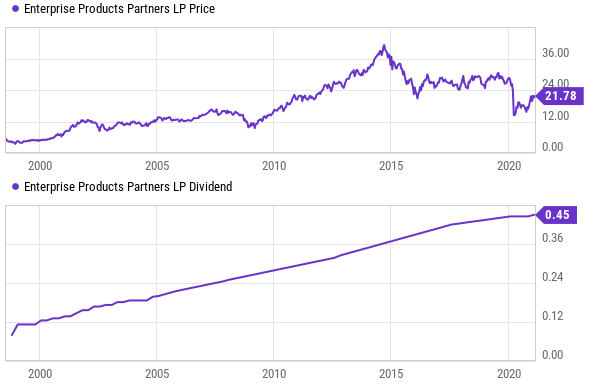

7. Enterprise Products Partners (EPD) 8.4%

If you are looking for big safe income, this midstream operator is attractive. It operates as a Master Limited Partnership (MLP), and has consistently maintained its distribution throughout the pandemic (while other midstream MLPs were cutting). Further, it’s actually increased the distribution 22 years in a row, and insiders have a large stake in the company.

You can access our new report on EPD here:

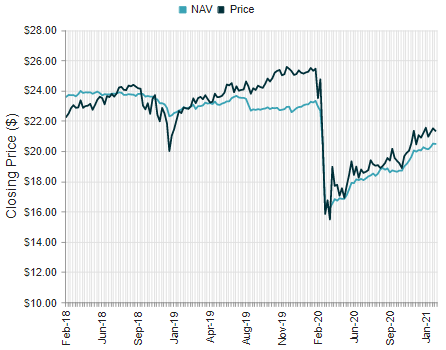

6. PIMCO Dynamic Income Fund (PDI), Yield: 9.9%

If you liked PIMCO’s Income Opportunity Fund at #10, you might like PIMCO’s Dynamic Income Fund (PDI) even more. For starters, it offers a higher yield (also paid monthly), it has the potential for more upside (the underlying bonds trade at an attractive discount to par), and the income has also remained steady and healthy throughout the market’s ups and downs. Plus this fund has a diversified basket of underlying bond holdings, including corporate bonds and asset backed securities, to name a couple. Further, it’s the premium to NAV is small by historical standards, suggesting to us there could be more upside potential to the shares.

You can read our previous write-up on PDI using the following link to get a better idea of all the things that go into our detailed review of this attractive high-income investment opportunity.

5. Realty Income (O), Yield: 4.5%

Realty Income has trademarked itself as ‘The Monthly Dividend Company’. We are impressed by its steady dividend track record (607 consecutive monthly dividend payments—more than 50 years) which is supported by a stable business model and disciplined execution. The company has successfully navigated through past economic downturns without cutting the dividend. This shows the resilient nature of company’s portfolio, conservative approach, and strong management skills. This all gives us confidence that Realty Income will outperform peers as we progress through the pandemic. In the current environment, where survival is the primary strategy, and investors are looking for safety, we believe Realty Income—with its proven track record—is a very solid choice to park your money for safe income and a continuing rebound in share price as the pandemic eventually will be brought under control.

We are currently long shares of Realty Income, and you can read our previous full report and thesis here:

4. BlackRock Multi-Sector Income (BIT), Yield: 8.3%

BlackRock closed-end funds (CEFs) are often not as popular as PIMCO funds, but the BlackRock team is very experienced and has immense resources at their disposal. This one pays big monthly income payments, and unlike the PIMCO funds in this report, BIT actually trades at a discount to NAV (not a premium). Some investors simply cannot get comfortable paying a premium.

Further this fund uses a little less leverage than most PIMCO Funds and it has a lower expense ratio. We have had a lot of historical success owning this fund, and you can view all the latest metrics on BIT at CEF Connect (here), and you can read our previous full write-up (to get a better undertsanding of our investment thesis) here:

3. WP Carey (WPC), Yield: 6.1%

Some of the best investments are made during times of distress. And there is a difference between trying to time the bottom and buying after it’s already bottomed and it has a lot more upside recovery ahead. We believe this is the case for W.P. Carey.

Specifically, WPC is increasingly healthy, and you can access our previous full write up on everything we like about W.P. Carey here:

2. PIMCO Dynamic Credit (PCI), Yield: 9.8%

If you like big monthly income and the potential for some price appreciation too, this one is attractive. Not only has it never reduced it’s dividend, but it occasionally pays additional special dividends, and the income payments are historically backed by the income produced by the holdings instead of a return of capital (a good thing).

PCI holds a diversified portfolio of bonds, and many of them currently trade at a discount to par (which means they have some attractive price appreciation potential). Plus the current price premium to NAV is narrow by historical standards meaning this one have even more upside price appreciation potential. You can check out all the most current stats and data on this one at CEF Connect (here), and you can read our previous report (below) for more information on how we view all the details of this one.

1. AGNC Investment Corp (AGNC), Yield: 8.8%

If you are looking for attractive high income at a discounted price, ACNC is worth considering for a spot in your portfolio. Not only does it trade at a discount to book value, but it holds very safe US agency-backed securities, and the US government has been going to great links to support this market since the onset of the coronavirus pandemic.

We consider these shares particularly safe. We own them. And you can read our latest full report on AGNC here:

The Bottom Line:

As an income-focused investors, you need to understand your own personal goals, and then invest accordingly. Depending on how much current income you need, you might be able to better maximize long-term returns by paying careful attention to dividend growth potential, as well as total returns. And critically important, just because something offers a higher yield, that doesn’t mean it’s a better investment. Investors should do their best to avoid value traps at all costs. At the end of the day, it’s your money. Know your goals, and then stick to your plan. Disciplined long-term investing has proven to be a winning strategy over and over again throughout history. It will this time too.