For years, investors have chased healthcare REITs with tenants funded by “private pay” because they feared ongoing government pressure on reimbursement rates. However, in this pandemic, it turns out they had it all wrong. CareTrust (CTRE) is a “mostly skilled nursing facilities” healthcare REIT, and it has benefited from generous government support during this pandemic. And on top of that, the CEO claims COVID hasn’t been as economically devastating as narratives suggest. This article reviews the health of the business, valuation, risks, dividend safety (it yields around 4.8%), and concludes with our opinion on investing.

Overview:

CareTrust REIT Inc. (CTRE) focuses on skilled nursing, senior housing and other healthcare-related properties. Its portfolio includes 212 net-leased healthcare properties (and one operated senior housing property) consisting of 21,652 operating beds/units. Specifically, as of Q1-20, CareTrust had over $1.7 billion in property investments in skilled nursing facilities (SNF), Assisted Living Facilities (ALF) and Independent Living Facilities (ILF), and Campuses that are comprised of SNF + ALF combined. Currently, skilled nursing facilities make up 72% of the overall portfolio.

The portfolio is geographically diversified across 28 states, with concentrations in Texas, California and Louisiana. CTRE is led by CEO Gregory Stapley who has more than 30 years of experience in the real estate industry including healthcare facilities and office, retail and industrial properties. He is supported by William Wagner, CFO who has more than 15 years of experience working extensively for REITs. CTRE’s market cap is approximately $2 billion.

(source: Company Presentation)

Impacts of the COVID-19 Pandemic:

The pandemic has been devastating to lives and to many healthcare facilities as the virus (and fear) spread rapidly in some places. As a result, healthcare REIT share prices were among the biggest decliners at the onset of the pandemic. However, as you can see in our earlier price chart, shares of CTRE have recovered significantly, a testament to the strength of the business (and support of the government—more on this in a moment). CEO Gregory Stapley noted during the most recent earnings call that the things are not as bad as they appear.

“In a minority of cases, we've seen the virus spread like wildfire resulting in multiple COVID-related fatalities. Those relatively few cases are the ones that make the news. However, in most cases, operators are able to contain and isolate and successfully care for the COVID patients in the facilities, only sending out to the hospitals the most critical patients, usually only those requiring ventilators.”

Government Support:

First of all, and importantly, CTRE’s SNF portfolio consists of approximately 75% Medicaid residents and 16% short-term Medicare or managed care patients. This means reimbursement is supported by the government (as opposed to private pay), and CTRE benefits from the longer-term nature of its patients. As a result, CTRE did not experience the dramatic drop in occupancy that some other healthcare REITs did. For example, accoridng to Stapley:

“Outside of the COVID hotspots, hospitals have been in a hurry-up-and-wait mode running incredibly low occupancies. They have largely stopped non-critical and elective procedures, and emergency department volumes have reportedly dropped significantly. Therefore, the skilled nursing facilities that depend most on short-term rehab patients coming from hospitals are being hardest hit. By contrast, the facilities that primarily care for the long-term Medicaid residents are less sensitive to the sharp decline in hospital census.”

Further, and to the great benefit of CTRE, the government has waived the three-day hospital stay rule for Medicaid residents to be eligible to qualify for Medicare skilled services. This means that CTRE’s SNF residents could qualify for higher Medicare rate skilled services without going to the hospital. This resulted in a higher margin skilled occupancy (an increase of 240 bps in April 2020).

“Today, a hypothetical Medicaid resident has a serious change of condition but is stable enough to be cared for in a facility. A new care plan is formulated, appropriate care is rendered. Now, Medicaid and Medicare rates vary widely by geography and patient. But say that yesterday Medicaid was paying about $200 a day for that resident. Today, Medicare begins paying $800 a day for that patient. So while we have seen parts of our portfolio experience drops in overall occupancy, the increase we've seen in skilled mix, which can offset the financial hit from census, declines. This emergency measure is one of several ways the government is helping operators bridge this difficult high risk phase of the pandemic.”

While overall SNF occupancy did decline by 370 bps in April 2020, the higher-margin skilled occupancy increased by 240 bps in April, providing additional revenue to offset the occupancy loss.

Further, under the CARES Act, a substantial number of CTRE’s tenants have received, or are expected to receive, assistance from a $100 billion fund provided for eligible healthcare providers, which includes operators of SNFs. Further still, the Payroll Protection Program also offers additional liquidity support to many of CTRE’s tenants.

For perspective, CTRE has collected virtually all of its rent in April and May 2020. Specifically, in April, CTRE collected 99.3% of contract rents, and collected 99.8% of May rents as of data available though the first week of May. This suggests that tenants are in good shape.

(source: Company Presentation)

Healthy Tenants:

The Top 10 tenants appear healthy with only one tenant reporting a lease coverage (EBITDAR) ratio below 1.0x. The Top 10 tenants account for ~83.7% of total rent. The lease coverage ratio for the overall portfolio (212 properties) is ~1.83x.

(source: Company Presentation)

Dividend Health:

CareTrust recently announced (on March 12th) that it would increase its dividend by ~11% from $0.225 to $0.25 per share. And considering the high ongoing rent collections and government support, we believe CTRE’s dividend is in good shares, and may continue to steadily increase. For example, the payout ratio was only ~73.5% in Q120 (a good thing). And based on the company’s 2020 normalized FFO mid-point guidance of $1.33 per share, the payout ratio is likely to remain at around only ~75% (the dividend is $1.00 per year). Even if CTRE experiences reduced payments from some tenants, it still has plenty of cushion.

(source: Company Presentation)

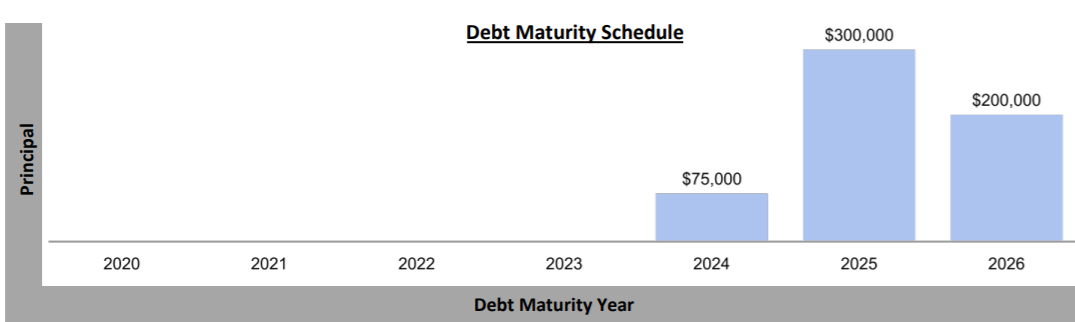

Strong Liquidity:

CareTrust is in a strong liquidity position with no near-term debt maturities and plenty of cash on hand. For example, as of Q1-20 CTRE had $45 million of cash on hand, and $525 million available under its revolving credit facility. Further, there are no debt maturities till 2023, thereby leaving CTRE with ample financial flexibility. For more perspective, balance sheet leverage was 3.5x at the end of Q1-20, hovering near all-time lows. All of these (cash, no near-term maturities and low leverage) provide additional levers to support dividend payment as well continue to aggressively pursue growth opportunities.

(source: Company Presentation)

With regards to acquisition opportunities, CareTrust recently noted that COVID-19 is likely to present more opportunities. For example, CTRE has closed two acquisitions so far in 2020, worth ~$26 million. Per management, CTRE’s current acquisition pipeline is ~$100-$125 million.

“As many banks and traditional buyers have headed to the sidelines both voluntarily and involuntarily, we feel like our balance sheet which was built for times like this, combined with our execution ability and closing certainty, provide us with the competitive advantage as we continue to work to grow our portfolio.”

Also worth mentioning, in a sign of financial strength, and an indication of a potentially attractive (low) market valuation, CareTrust recently announced a $150 million share repurchase program (not insignificant for a $2 billion market cap company)

Valuation:

On a Price to Adjusted Funds from Operations basis (“Price to AFFO”), CTRE is trading at ~15.0x its 2020 estimate, which is below many popular healthcare REIT peers (see table), despite having a stronger payout coverage ratio and lower leverage. Further, we believe there is room for additional multiple expansion, despite the fact that the shares have rallied off mid-March lows (the shares continue to trade well below last year’s highs)

(source: Blue Harbinger Research, Yahoo Finance, Company data)

Also important to note, CareTrust’s largely skilled-nursing facilities focus differentiates it from other types of healthcare REITs. Another popular SNF REIT is Omega Healthcare Investors (OHI), which has performed similarly (see chart below), but trades at only a 12.2x 2020 P/AFFO estimates. However OHI has a higher (riskier) payout ratio (84.4%) and an ongoing history of very troubled operators. Omega was also hit hard by the coronavirus, and has withdrawn its forward earnings guidance).

Risks:

Tenant concentration: The top 2 tenants account for nearly ~49% of total rent. This exposed CTRE to significant risk should one of these tenants face financial trouble. However, the tenants are healthy with rent coverage well above ~1.0x which minimizes any concerns.

Interest rate risk: The Federal Reserve has cut interest rates to zero and even though we expect interest rates to remain relatively tame, dramatically rising rates could create challenges. As REITs are often seen as an alternative to bonds, higher interest rates could mean decreased demand for REITs, thereby causing a decline in the share price. Also, higher interest rates put downward pressure on earnings as interest costs rise. Nonetheless, we don’t see rates going meaningfully higher anytime soon.

Regulatory risk: CareTrust relies on payments from Medicare and Medicaid, which are vulnerable to political interference. Any unfavorable regulation could adversely impact the business. In fact, this risk has kept investor optimism low for CareTrust versus “private pay” healthcare REITs in recent years. However, as we have seen during this pandemic, government support can actually be a good thing in term of cash flow predictability and risk reduction.

Conclusion:

CareTrust has performed remarkably well during this pandemic (especially relative to other REITs), and we view this as a testament to its financial health and strength. However, the shares still trade at a reasonably low price and valuation, providing investors an opportunity to add new shares (or at least continue to own existing shares). The recent dividend increase and low payout ratio are encouraging. As is the new share repurchase program and the ongoing support from the federal government. In our view, CareTrust offers investors relatively safe dividend income (it yields 4.8%) and the potential for ongoing price appreciation.