Oaktree Strategic Income Corp (OCSI) is a Business Development Company (“BDC”) managed at the firm (Oaktree) founded by famous debt investor, Howard Marx. This particular BDC invests primarily in high-yield, first lien, liquid, middle-market debt. And even though its share price has been hit hard by the COVID-19 pandemic (as most BDCs have been), OCSI has been positioning its portfolio and balance sheet conservatively for multiple years in anticipation of stressed market conditions (such as the current market environment), so it can not only weather the storm, but also so it has the financial wherewithal to be opportunistic when other BDCs cannot. This is also a big part of the reason OCSI recently proactively reduced its dividend—a good thing for new investors, in our view. This report reviews the business, COVID-19 impacts, dividend prospects, valuation and risks. We conclude with our opinion about the attractiveness of this 8.0% yield BDC.

Key Investment Thesis Points:

Conservative positioning in the form of a well-diversified portfolio coupled with 91% of the book in first lien investments reduce risk of capital impairment.

Gradual repositioning of investments to higher quality, larger borrowers proving beneficial during current downturn.

Significant decline in NAV and share price due to unprecedented market dislocation in late March however recovery underway and dividend largely safe after the recent adjustment.

Trading at an attractive dividend yield of ~8%, higher than historical average.

Overview:

Incorporated in 2013, Oaktree Strategic Income provides debt capital to middle market companies. OCSI’s investment objective is to generate stable current income with capital appreciation being a secondary objective. As of 31st March 2020, the company had a total investment portfolio of $524 million invested across 88 companies in various industries. Importantly, 91% of the portfolio consists of first lien debt investments (this makes the company less susceptible to capital losses in cases of broader economic distress). OCSI has also entered into an agreement with GF Equity Funding to form Glick JV. The joint venture primarily invests in senior secured loans in middle market companies. The investment in Glick JV makes up 7% of the total portfolio. Finally, and importantly, approximately 66% of the debt investments made by OCSI are publicly traded.

Source: OCSI

In terms of industry exposure, the software sector forms the largest portion of the portfolio (15% of portfolio value). The table below shows the industry classifications of OCSI’s investment portfolio.

OCSI’s top 10 investments make up just 24% of the total portfolio, and none of the investments account for more than 4% (thereby leading to low concentration risk). The table below shows the company’s top 5 portfolio investments.

What Is A Business Development Company (BDC)?

A business development company is a closed-end investment company that invests in privately owned, middle-market companies, providing them capital to grow or recapitalize. BDCs were created by an act of Congress in 1980 to incentivize small business investments through tax advantages.

What Are the Advantages of Investing via a BDC?

High dividend yield as BDCs are required to distribute 90% of their profits to shareholders as per the governing law.

Being a regulated investment company, a BDC is not required to pay corporate income taxes on profits.

They offer diversification as the portfolio consists of companies belonging to varied industries.

Experienced Investment management teams.

Fair amount of liquidity and transparency as BDCs are traded on public exchanges, unlike venture capital funds which are privately placed.

As they are traded on stock exchanges, periods of volatility can lead to shares of BDCs trading at attractive discounts to NAVs.

Seasoned investment team with history of managing credit investments in difficult environments

OCSI appointed Oaktree as its investment manager in 2017. Prior to this, the fund was managed by Fifth Street Asset Management Inc. Founded in 1995 by legendary investor Howard Marks, Oaktree is a leading global asset manager with its primary focus on credit investments and it has a history of managing opportunistic, distressed investments through the ups and downs of economic cycles. As of March 2020, Oaktree had $113 billion in asset under management. The OCSI management team consists of following individuals from Oaktree. The management team is supported by 16 investment professionals including five Managing Directors.

The portfolio structure of OCSI has undergone a major revamp since Oaktree took charge in 2017. The investment approach has shifted from a focus on smaller private borrowers to larger borrowers and more liquid debt investments. OCSI’s portfolio company leverage has also improved significantly from 5.4x in 2017 to current levels of 4.6x which reflects the transition towards higher quality and more defensive debt investments.

Please note that majority of the target repositioning of portfolio investments (from non-core to core sectors) has already taken place. OCSI is left with only 4 non-core (riskier) investments which constitute ~7% of the total portfolio.

COVID-19 led to decline in NAV and income but the portfolio is well positioned to manage through this downturn

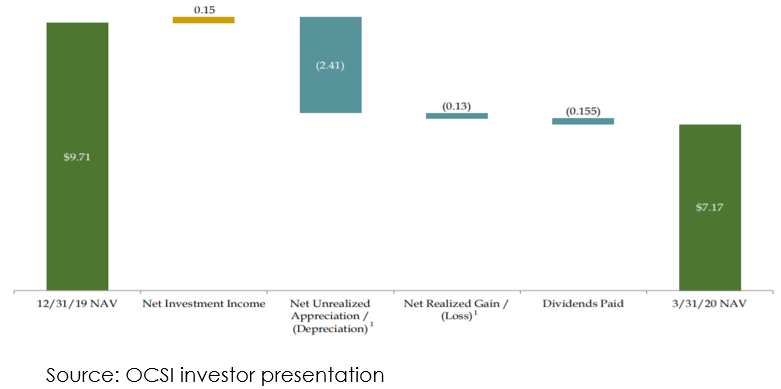

OCSI saw a significant erosion in net asset value in Q2 FY-20 due to the broader market sell off. As mentioned earlier, 66% of OCSI’s portfolio includes liquid credit investments which experience a dramatic sell off in late March. This caused sudden downward pressure on the NAV as OCSI had to record mark to market losses. NAV declined from $9.71 per share in Q1 FY-20 to $7.17 per share in Q2 FY-20 which represents a decline of 26% on QoQ basis.

Total investment income declined by 11% QoQ from $11.6 million in Q1 FY-20 to $10.3 million in Q2 FY-20. The decline was primarily caused by the combination of reduced interest payments from subordinated notes issued by Glick JV, as well as a continued decline in LIBOR. However, net investment income declined only slightly from $4.7 million in Q1 FY-20 to $4.5 million in Q2 FY-20 because of a decrease in incentive fees to the investment manager as well as reduced cost of capital due to falling base rates.

Despite near term hit, we believe OCSI is well positioned to manage its business in this difficult environment. While lenders with high portfolio concentration in stressed industry sectors (such as hospitality, aviation, retail, travel and leisure) are facing considerable compression in interest income due to mounting bad debts and interest deferments, we believe OCSI will face limited stress because of its well-diversified and conservative investment portfolio, as well as limited exposure to stressed sectors. For example, 5.1% of the company’s portfolio is focused on the Energy sector, however the majority of these investments are in midstream industries and refineries which have less direct oil price exposure. Finally, the Leisure and Entertainment sector accounted for only 3.4% of the overall portfolio exposure as of 31st March 2020.

“We are generally confident in the quality of our portfolio, given its defensive posture prior to the pandemic. The portfolio consists predominantly of first lien positions to larger, more diverse companies that we believe can bridge the gap to recovery.” – Armen Panossian, CEO on Q2 2020 call

Meanwhile, Fed intervention has brought some calm back into the high yield space

Coronavirus shutdowns have led to a substantial sell-off in most dividend-oriented names (including BDCs) due to concerns among investors regarding interest and principal deferments by portfolio companies. OCSI dropped 45% in March and has seen some recovery since then, but it is still trading well below its pre-COVID levels. High yield bonds were the most impacted by the dislocation in the markets and saw the sharpest increase in yield spreads since the 2008-09 financial crisis. However, fed intervention in bond markets including in the high yield space has led to substantial compression in spreads.

Source: St Louis Fed

Worth mentioning, with 66% of OCSI’s debt investments traded publicly, but the book value only marked to market quarterly, it’s reasonable to assume OCSI’s portfolio value has rebounded with high yield bonds since the end of the quarter.

OCSI proactively reduced the dividend to protect capital, and further downside from current levels looks limited

In line with many other BDCs, in order to preserve liquidity and prevent further erosion of capital after a decline in NII and NAV, OCSI reduced its quarterly distributions from $0.155 per share to $0.125 per share which represents a decrease of almost 20%.

“We believe that this reduction is prudent and will help OCSI to navigate the current environment. Importantly, we have liquidity to meet existing funding needs and continue to opportunistically invest.” – Matt Pendo, Chief Operating Officer on Q2 2020 call.

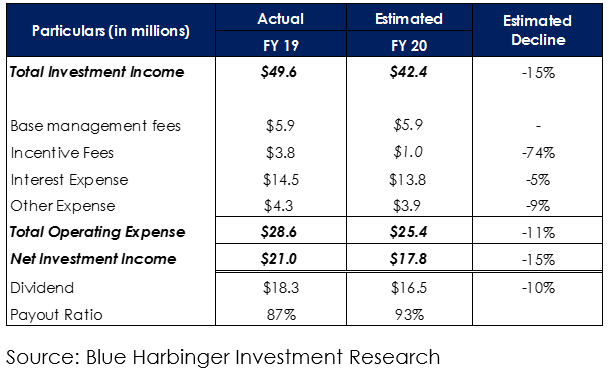

We stress tested the company’s portfolio to analyze the robustness of OCSI’s income and dividend safety. As of FY-19, OCSI’s portfolio companies had a debt to EBITDA of 4.6x and conservatively assuming the average cost of debt at these companies at ~7.5%, the theoretical EBITDA to interest ratio of portfolio companies should be around 2.9x.

Even if we assume that the EBITDA of portfolio companies declines by 50% in the worst case scenario, the average portfolio interest coverage ratio would still end up being 1.4x implying that OCSI’s Interest income has sufficient downside protection during current economic turmoil. However, keeping in mind OCSI’s modest exposure to energy, leisure & entertainment sector, along with the restructuring of Glick JV subordinated notes at lower coupon rates, we have conservatively assumed a 15% decline in interest income for FY 20. Interest expense is projected to be down 5% and base management fees is expected to remain flat, however, incentive fees are expected to decline as it is contingent upon the level of interest income.

As evident in the table below, OCSI will not face any material difficulties in maintaining the current level of distributions.

Sufficient liquidity to opportunistically invest in attractive mispriced debt assets and fund near term commitments

At the end of Q2 FY-20, OCSI had approximately $22 million in cash and $78 million of undrawn credit facility. The available funds will provide sufficient liquidity to meet unfunded commitments as well as invest in attractive business opportunities currently trading at distressed valuations due to market turmoil. The company made new investment commitments to the tune of $94 million while the markets were dislocated in March. In fact, in April, OCSI invested $5 million in first lien debt of Airbnb at LIBOR +7.5% with a 2 year call protection.

“As the volatility took hold in March, we became more active in the public market via our trading desk, and made opportunistic purchases across primary and secondary markets and industries such as healthcare, pharma, infrastructure, and telecom…..While we are maintaining modest overall exposure to virus impacted sectors, we have identified some unique, highly selective opportunities in these industries with very attractive risk-reward profiles. A case in point is our recent investment in Airbnb…. We believe the coming weeks and months will provide OCSI with additional opportunities in both public and private investments.” – Armen Panossian, CEO on Q2-2020 call

Please note that OCSI has a $200 million credit facility maturing in March 2021. Given the defensive first lien debt assets on the balance sheet as well as backing from a large, global asset manager, it is expected to face no material difficulties in refinancing its debt obligations.

Attractive valuation after broad market sell-off

Even after the reduced dividend payment, OCSI is trading at a forward dividend yield of ~8% which is higher than its 3-year historical average of 6.8%. Price-to-NAV also declined considerably in Q2 but has recovered since then. However, please note that OCSI had to book a substantial unrealized mark to market loss in Q2 FY-20 which was the primary reason for the decline in NAV. Since high yield spreads are normalizing after the Fed ramped up intervention, NAV is set to rise as of the next quarterly report.

Risks

A prolonged economic slowdown (i.e. ongoing coronavirus challenges) is the number one risk for OCSI, in our view. This could lead to a substantial increase in interest rate deferrals or requests for debt restructuring. This may materially impact OCSI’s profits and may also lead to considerable erosion of asset value. However, as mentioned earlier the company was well positioned from a risk standpoint going into this downturn and we remain reasonably confident in its future income potential.

Conclusion

While most BDCs have been severely impacted as a result of elevated financial uncertainties in the credit markets, we believe that OCSI is less susceptible to the current downturn because of its well-diversified portfolio, the majority of its book being in first lien debt and its limited exposure to stressed sectors such as oil & gas production, travel, and leisure. The book value will likely be reported significantly higher at the end of this quarter, and the current valuation provides investors an attractive window of opportunity to capture a superior risk/reward.