Triton International (TRTN) is an intermodal shipping container company, and the big-yield common and preferred shares have been impacted dramatically by the worldwide COVID-19 pandemic. The company just released earnings, and gave us some important new insights. This report reviews the impacts of the economic slowdown on Triton’s business, its financial wherewithal (particularly cash), the competitive dynamics of the industry (and what might happen if Triton can weather the COVID-19 storm), valuation and risks. We conclude with our opinion about investing in the common (7% yield) and preferred (+9% yield) shares.

Overview:

Triton International (TRTN) is the world’s largest lessor of intermodal containers (if you don’t know, Intermodal containers are the large, standardized steel boxes used to transport freight by ship, rail or truck). Triton owns a fleet of 3.6 million dry, refrigerated, and specialty containers, and counts the world’s largest shipping companies as its customers. Triton generates the majority of its revenues from leasing equipment to core shipping line customers via long-term and short-term leases. Long-term leases typically have initial contractual terms ranging from three to eight years and provide the company with stable cash flow. As of the end of Q1-20, ~71% of TRTN’s on-hire fleet was under long-term lease.

(source: Company Data)

TRTN is the #1 player in the intermodal container lessor market with a worldwide share of ~28%. The industry has seen consolidation over the recent years and the COVID-19 outbreak could accelerate this trend as companies with weak balance sheets get acquired or shutdown. This should benefit larger and stronger players such as TRTN.

COVID-19 Impact? Near-term pain but Long-term potential intact

Triton just recently released earnings, and noted that COVID-19 had a significant impact on trade volumes during Q1-20 and it will have further impacts in the second quarter as the effect of the widespread business shutdowns fully weigh on economic and trade activity. TRTN’s Executive Vice President, John O’ Callaghan noted in the Q1-20 earnings call:

“COVID-19 is having a significant impact on trade volumes. All manufacturing in China closed for the Chinese New Year holiday period at the end of January and remained closed through February as China implemented extensive work restrictions due to the COVID-19 outbreak. As these restrictions eased in China, export volumes started to recover through March with exports from China starting to approach normal levels by the end of the month. Our customers are now preparing for another significant decrease in cargo volumes in the second quarter resulting from the spread of COVID-19 and the extensive global economic shutdowns.”

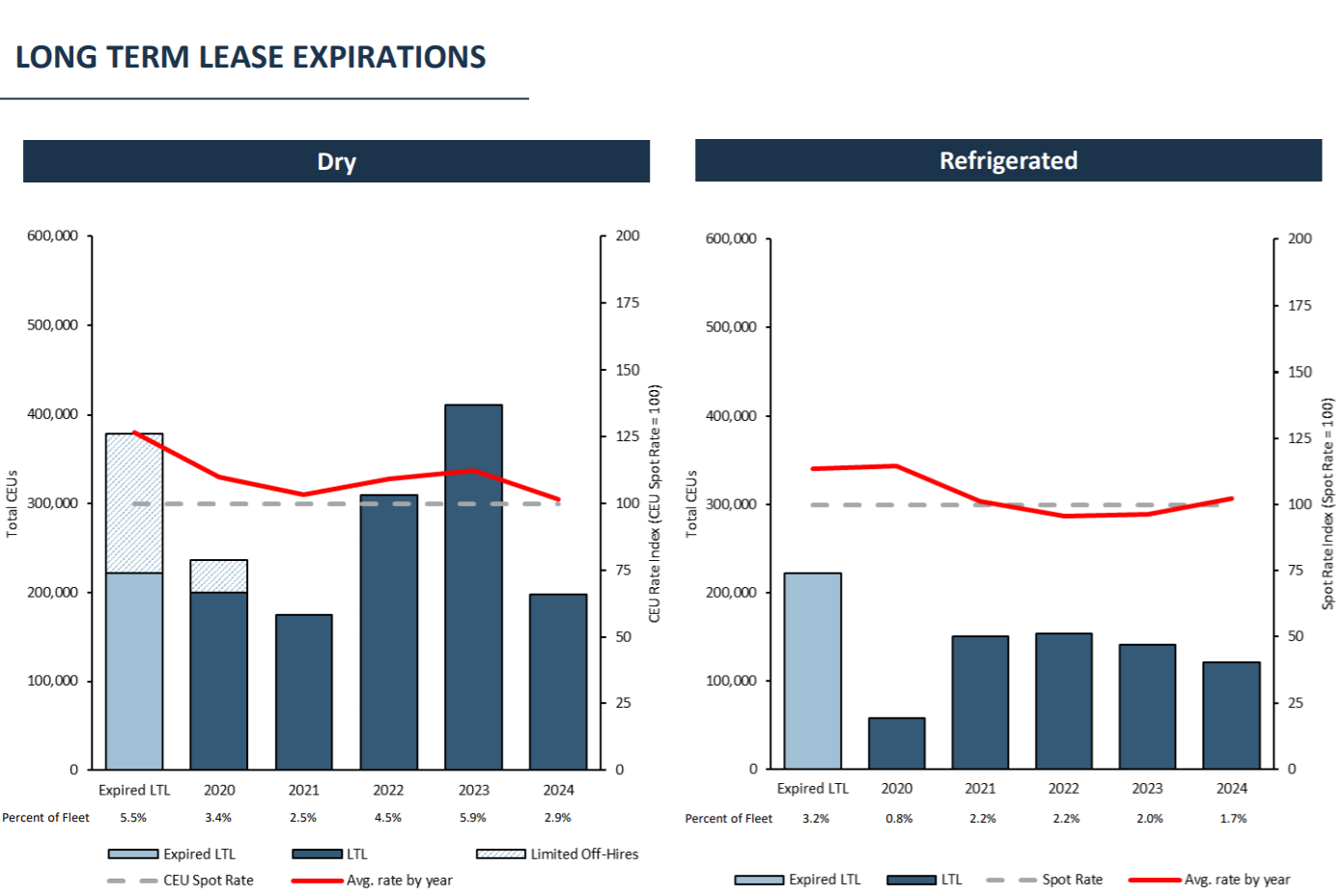

While underlying trade volumes are expected to be very weak in Q2, TRTN noted that it has not seen a major impact on its own operations so far. Though there has not been any pickup activity, but the container off hires are moderate and utilization is holding up well. We note that the average utilization for Q1-20 was 95.4% and has decreased marginally to 95.2% as of mid-April 2020. Importantly, TRTN is well-protected for the near-term drop-off risk due to long-term lease portfolio. As can be seen from the chart below, near-term lease expirations account for a small percentage of the overall fleet portfolio.

(source: Company Presentation)

Another factor supporting TRTN’s performance right now is that operational container flow disruptions actually create more need for containers because containers have been stuck in terminals and movements disrupted by blank sailings.

While the timing of recovery remains uncertain and will be largely dependent on how fast the pandemic is controlled, we believe TRTN has enough firnancial strength (e.g. solid cash flow and a strong balance sheet) to manage the current situation and benefit from the eventual recovery.

Low leverage, solid cash flow and secure dividend

Triton has a strong balance sheet, significant liquidity and a well-structured debt maturity profile. Management has taken a number of actions to strengthen its balance sheet over the last five quarters. For example, since the beginning of 2019, Triton has issued $555 million of preferred shares and due to the challenging market conditions, limited its investment in new containers. Together, these actions have led to a significant reduction in leverage. We note that TRTN focuses on net debt as a percentage of revenue earning assets (REA) as the key leverage metric. As can be seen from chart below, net debt to REA is currently at 67.8%, the lowest in its history validating management’s prudent balance sheet management.

(source: Company Presentation)

Additionally, the company has access to liquidity of ~$3 billion as of the end of Q1-20. And even after considering the next 12 months of major cash obligations (which amount to ~$990 million), TRTN will still be left with ~$2 billion in excess liquidity. In addition to this, the company generated a significant amount of cash flow. As per management, cash flow before capex is expected to be in excess of $700 million for 2020 and more than $750 million for 2021. And by 2023 it is expected to cross $1.5 billion.

(source: Company Presentation)

The current quarterly dividend of $0.52 per share represents an annualized yield of 7.1% based on the current market price of around $29. We think the dividend is extremely safe and sustainable given the ample liquidity, flexible balance sheet and solid cash flow generation. Further, TRTN has been actively repurchasing shares which is another way of return capital to investors. It repurchased 2.1 million shares so far in 2020 and has now purchased over 13% of its outstanding shares since the program started in August 2018.

Preferred Shares:

TRTN has issued four classes of Preferred shares so far – 8.50% Series A, 8.00% Series B, 7.375% Series C and 6.875% Series D. All four classes were issued with liquidation preference of $25.00 per unit, at a price to the public of $25.00 per preference unit. These units that are senior to the common units and as such receive priority over the common units in distributions and liquidation.

All four preferred shares are currently trading at significant discount to their liquidation preference. The discount was recently (based on market prices) as follows: TRTN Series A at 12%, TRTN Series B at 18.6%, TRTN Series C at 20% and TRTN Series D at 24%. While historically these shares have tended to traded at slight premium since listing. We think the current discount is very attractive and provides investors with an opportunity to buy low. The dividend yield on these preferred shares is also much higher versus the common shares. The preferred units typically show much lower price volatility when compared to common units. Thus, it is especially attractive for investors who seek steady income with less volatility.

The existing preferred shares are cumulative (i.e. if Triton misses a dividend payment, they are required to make it up later, so long as they do not go bankrupt). And importantly, the preferred shares are redeemable by the company starting on Mar 15, 2024, for Series A, Sep 15, 2024, for Series B, Dec 15, 2024, for Series C and Mar 15, 2025, for Series D.

The COVID-19 crisis, in our view, has created an opportunity for investors to buy high yield at low price. Risk-averse investors may prefer the preferred shares over common units given their attractive prices and high yields.

(source: QuantumOnline, Blue Harbinger Research)

Valuation:

From a valuation standpoint, we compare TRTN to its historical range of EV-to-EBITDA multiple. TRTN is currently trading at LTM EV to EBITDA of 7.1x, which is at the lower end of its 10-year historical range of 6.7x-14.9x. Therefore, on this important metric, we believe the valuation is significantly attractive and we could see strong capital appreciation once the recovery commences. Also, given its large size, strong balance sheet and proven ability to successfully ride out previous economic downturns, we believe the current valuation offers an attractive opportunity for investors to buy low.

Risks:

Economic downturn: Demand for containers depends largely on the rate of world trade and economic growth. A severe and prolonged economic downturn could result in lower demand thereby reducing revenue and profitability. We believe, Triton will likely come out of the global pandemic stronger, considering trade will continue, and weaker competition may cease to exist or be acquired.

Customer concentration: TRTN’s twenty largest customers account for 85% of its billings. Further, five largest customers accounted for 53% of billings, and two largest customers, CMA CGM and Mediterranean Shipping Company, accounted for 21% and 14%, respectively, of lease billings in 2019. A default by one of the major customers could have a material adverse impact on the business, financial condition and future prospects.

Dividend Return of Capital: Another item for investors to be aware of is that Triton’s dividend has generally been taxed as a return of capital. This means that your investment cost basis is being reduced with each dividend, and that will impact your capital gains tax when you go to sell your position. Triton provides more information here.

Default risk: TRTN faces elevated customer credit risk due to the sharp decrease in freight revenue for its customers. Credit risk will be especially high if the COVID-19 shock results in a sustained economic and trade downturn. However, we believe Triton survives the current COVID-19 economic dowturn (the company may come out stronger on the other side), and a lot of pain is already priced into the shares.

Conclusion:

Triton’s business is being impacted by the COVID-19 economic slowdown. However, its longer-term leases and strong cash position will help it weather the storm. Global economic trade will continue and eventually return to (and above) prior levels. In fact, many of Triton’s smaller peers may not whether the storm, which could ultimately work to Triton’s advantage. We believe the common units are attractive, however we prefer the preferreds. They are trading at an attractive price (i.e. they have some significant upside), they are safer and less volatile than the common, and they offer an attractive big yield. If you are a long-term income-focused investor, Triton is worth considering for a spot in your prudently diversified portfolio. We are currently long TRTN-A.