The volume of natural gas demanded did not go down appreciably during the Great Recession nor the 2015 oil price crash, and it won't here either. Thus firms whose main business is moving natural gas from here to there for a fixed fee are not going be that heavily affected. This guest article (from Darren McCammon) reviews two such companies that currently offer attractive, well covered, double digit dividend yields (we currently own one of the two). According to Mr. McCammon “these are exactly the type of firms one should be buying greedily as everyone else runs in fear.”

US natural gas demand was down 4% in March (-4.4 B cf/d) with warmer than normal weather, and fog along the Gulf coast preventing LNG export being the main culprits. Electricity based demand is actually increasing as low prices continue to spur the transformation from coal to natural gas based electricity production.

Source: RBN Energy

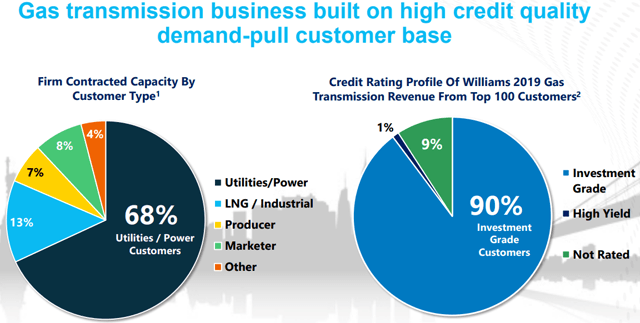

Are these the COVID-19 and oil price war induced volume declines everyone fears? Is this the reason fixed-fee, natural gas volume dependent, Williams (WMB) is down 41% year to date? Are we really worried that Williams 1.8x covered 11.6% dividend yield is going to be cut when natural gas demand continues essentially unabated and 90% of their customers enjoy investment grade credit?

Source: Williams Presentation

How about fixed-fee, natural gas dependent Archrock (AROC), down 62% year to date? Are we really worried that Archrocks 2x covered 16.1% dividend yield is going to be cut when natural gas demand remains solid, and you simply can't move gas to the end user without a compressor? 70% of Archrock's customers enjoy investment grade credit. Are these the counterparties we are worried about because March natural gas volume is down 4%?

Source: Archrock Presentation

Or maybe, just maybe, Mr. Market is over-reacting. Maybe these well covered double digit dividend yield opportunities are exactly what one should be buying greedily as everyone else runs in fear?

The volume of natural gas demanded in the US was unaffected by the Great Recession. It even increased during the 2015 oil price crash.

Source: US Energy Information Administration

This time isn't different. Companies that specialize in moving natural gas from here to there, such as Williams and Archrock, are going to be just fine.