Many popular PIMCO closed-end funds (CEFs) have sold off particularly hard as investors fear the potential impacts of a coronavirus-driven recession. Further, large CEF premiums versus net asset values (NAVs) have evaporated into unusually large discounts as selling pressure has been intense. Further still, the price declines have been exacerbated by a drying up of liquidity in the bond markets. And even though the US Fed has dramatically increased its quantitative liquidity easing in the treasury and agency Mortgage Backed Securities (MBS) repo markets, just this week it announced that it will “be moving for the first time into corporate bonds, purchasing the investment-grade securities.” To some investors, the Fed’s essentially unlimited buying power is terrifying, and to others it is highly reassuring. Will you be betting against the Fed?

PIMCO Bond CEFs:

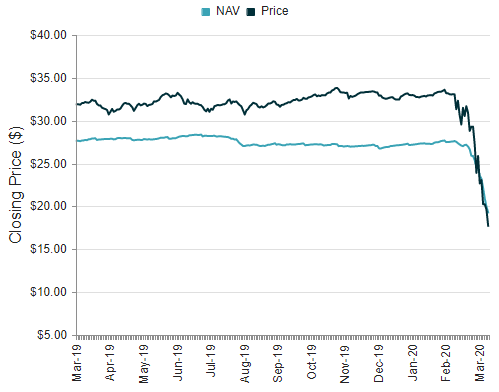

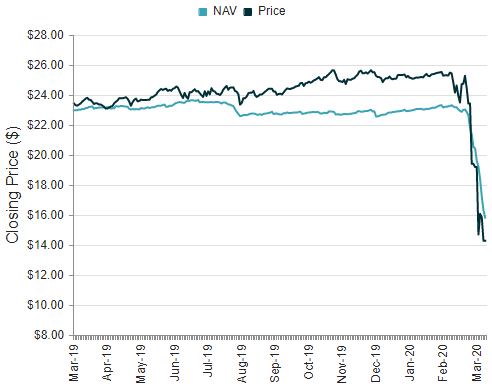

For perspective, here is a look at the recent price action of a couple popular PIMCO CEFs, and it has been ugly.

PIMCO Dynamic Income Fund (PDI), Yield:14.9%

PIMCO Dynamic Credit & Mortgage (PCI), Yield:14.6%

The right types of bonds: Important to note, these funds hold some of the exact types of securities that the fed is currently buying in the repo market (see sector allocation tables above), and this will benefit the funds in multiple ways. First and foremost, the fed’s actions are intended to free up liquidity in these market which should increase the prices of the bonds (part of the reason the bond prices are so low is because there aren’t many natural buyers, supply/demand). Secondly, as the fed frees up liquidity in treasury, agency MBS (and now corporate bond) markets, that liquidity should flow through to other major bond markets and increase prices there as well. Through its stimulative monetary policy, the fed is essentially working to boost the prices of these PIMCO funds.

As a side note, before you ask, the MV% is the notional market value of holdings (including exposures gained through the use of interest rate swaps at the market value of the swaps). Further, DWE% is duration weighted exposure (duration is a measure of interest rate risk). Also, you’ll notice the weights sum to over 100% (more on leverage later, see risks).

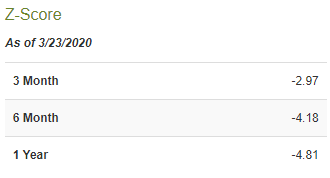

Unusual Discounts to NAV: Also important to note, these bonds are trading at unually large (and attractive, in our view) discounts to NAV. For perspective, the Z-scores of both funds are below negative two for all time frames reported. According to Morningstar:

“The z-statistic is used to measure a fund's discount/premium relative to its average discount/premium. Z = (Current Discount - Average Discount) / Standard Deviation of the Discount. A negative z-score indicates the current discount is lower than the average, and vice versa. The magnitude suggests whether the z-statistic is significant: For instance, a z-statistic of +2 or greater would be expected to occur less than 2.25% of the time.”

What is the Repo Market

The repurchase (or “repo”) market is one of the Federal Reserve’s monetary policy tools. It’s basically a market that allows investors with a lot of securities (e.g. PIMCO) to borrow money cheaply (by pledging their securities as collateral), and also a place for people with a lot of cash to earn a little interest by lending it short-term. The Fed uses the repo market to inject liquidity into the system during times of distress (i.e. right now) by buying securities. And as mentioned earlier they have dramatically expanded their repurchase activity recently in terms of scale and the types of securities they’re willing to buy.

To some, the fed’s recent repo market activity is highly reassuring because they’ve pledged to support the financial system, and there is no limit to how much they can buy in the process. However to others, the fed’s actions are terrifying and the repo market is a dam ready to break.

What Does History Show?

For a little perspective, here is a look at credit spreads now versus during other times of financial distress (such as the financial crises, the energy market turmoil in late 2015 / early 2016 and the tech bubble).

As you can see, spreads are dramatically elevated right now, and they are near other bouts of past volatility. Similarly, bond funds (such as PDI and PCI) tend to follow credit spreads relatively closely. And although they were not around during the financial crisis, these funds have historically risen and fallen as credit spreads have narrowed and widened. Further, their discounts versus NAV have historically widened during times of distress (such as the late 2015 / earnly 206 high yield distress), only to recover to premiums thereafter. In this regard, some investors may consider the current discounts to be attractive buying opportunities.

PDI: Historical Premium / Discount:

PCI: Historical Premium / Discount:

source: CEFConnect

There is certainly no guarantee that the current large discounts (to NAV) for these funds will revert back to premiums (or turn into larger discounts), but it’s worth considering what the PIMCO management team has to say.

What Does PIMCO Have to Say?

PIMCO regularly posts updates on its website, and this one is worth reviewing. In it, the company basically explains that distress in the bond market (particularly the mortgage market) is no where near what it was during the financial crisis (this is a good thing). Specifically, there are no fear as to whether Fannie and Freddie will remain going concerns (like there was during the financial crisis), and this crisis is one of liquidity (which the fed is working to address). It’s worth a listen.

What Are The Risks?

There are obviously a wide variety of risks to investing in PIMCO closed-end funds, such as the two we’ve highlighted in this article.

Leverage (or borrowed money) is an a risk. Specifically, PIMCO recently reported an effective leverage ratio (as of 2/28/20) for PDI and PCI of 38.06% and 43.95%, respectively. That means for each dollar someone has invested in the fund, PIMCO has purchased $1.38 (and $1.44, respectively) worth of securities, ceteris paribus. When times are good, leverage can magnify returns. When times are bad, it can magnify losses. It may be encouraging to some to know that the PIMCO CEFs are borrowing at a much lower interest rate than you probably could, and they have significant risk management and discipline in place that you likely would not. Nonetheless, leverage is a risk.

Fees and expenses are another risk to be aware of. For example, PCI recently reported a management fee of 1.15% and a total expense ratio (excluding leverage) of 2.12% (it rises to 4.63% when you include the cost of leverage). Nonetheless, we believe these expenses are reasonable considering the PIMCO management team gets you exposure to investments you could not easily get on you own, plus the price and discount to NAV are attractive (not to mention they send you distributions monthly so you don’t have to constantly be monitoring and selling individual sub-securities to meet your cash needs).

Market Conditions: As mentioned, current market conditions have been volatile and could get worse. The coronavirus impact on the economy will be massive (mostly from people not working due to social distancing, and the the impacts to business). The fed is working diligently through monetary policy to support the system, and the federal government is working on stimulus plans with a price tag of over $1 trillion. Again, to some this is very reassuring, but to others it is terrifying.

Conclusion:

We recognize that many investors are terrified of what is happening in the bond market and the coming coronavirus recession. They believe fed monetary policy and government stimulus cannot stem the coming damage. We acknowledge openly that the unemployment rate is going to skyrocket and GDP will likely shrink dramatically. However, we believe this too shall pass, and market conditions will eventually get better. We are not betting against the Fed. We are long PCI, and we expect the NAV will eventually rise (as liquidity challenges are resolved), and the large price discount will eventually revert back to a premium (as investor fear eventually subsides). In this case, we agree with famous value investor, Seth Klarman:

“Paying Less is Less Risky. Risk comes from the price you paid… It isn’t uncertainty or volatility. When there is great uncertainty and it drives prices down, you buy with less risk.”