Shares of Digital Realty (DLR) are down 13%, as they’ve recently gotten caught up in the indiscriminate “REIT sell-off” driven largely by macroeconomic noise (i.e. the Fed changed its interest rate posture at the end of October). However, the business (it’s a data center REIT) offers an attractive opportunity for investors seeking steady growing income along with significant long-term price appreciation potential. In particular, DLR has raised its dividend for the past 14 years, and is likely to continue to do so given strong industry tailwinds. This article reviews the health of the business, valuation, risks, dividend safety, and concludes with our opinion on why Digital Realty is worth considering if you are a long-term income-focused investor.

Overview:

Digital Realty is a leading REIT which is engaged in the business of owning, acquiring, developing and operating data centers. DLR recently announced a merger with Netherlands-based data center REIT InterXion Holding (INXN). DLR’s portfolio consists of 211 data centers, including 41 data centers held as investments in unconsolidated joint ventures. These data centers are mainly located throughout North America, with 41 located in Europe, 19 in Latin America, eight in Asia and five in Australia. This excludes any contribution from the recently announced merger with INXN.

A data center is a physical facility that organizations use to house their servers, critical applications and data. These facilities provide a highly reliable and secure environment and are equipped with uninterruptable power supplies, air-cooled chillers and physical security. Data center REITs own and manage these facilities. The computer servers which process and store data are supplied and owned by the customers. While the other components (including building shell, electrical systems and other components) are provided by data center REITs. The need for secure and reliable data storage has exploded and is expected to continue to remain strong. This is fueling demand for data center REITs.

(source: Company Presentation)

Geographically, DLR has presence across the globe but North America is its largest market accounting for 77% of its total rent as of 3Q19. This is followed by Europe at 13%, Asia at 7% and Latin America at 3%. Further, within each geography, the firm's revenues are highly diversified with its largest market (Northern Virginia) accounting for about 23.5% of sales, followed by Chicago at 11.4% and all other markets representing single-digit revenue concentration. Most of its properties are located in metro areas.

Moreover, DLR boasts of high quality and diversified customer base across industries ranging from cloud and information technology services, communications and social networking to financial services, manufacturing, energy, gaming, life sciences and consumer products. The top 20 customers account for just 53.7% of total rent with no single customer accounting for more than 7.8% of rent. More than 50% of its clients have investment grade or equivalent credit ratings.

(source: Company Presentation)

Digital Realty’s Leasing Momentum Is Strong

In 3Q19, DLR achieved its all-time second-best space and power backlog signing figure of $69 million, taking the total ending backlog to $98 million. Interconnection signings were $8 million, further extending DLR's foothold. 3Q19 wins were broad-based across products and geographic regions including a 14 MW deal in the Ashburn market. While DLR continues to monetize well with existing customers, the company also added 64 new logos in 3Q19 quarter. We are encouraged by this strong performance, and given its current backlog—the company is well positioned to deliver solid revenue growth.

Merger with INXN – To Become the Second Largest Data Center REIT

In October 2019, DLR announced plans to merge with Netherlands-based data center REIT InterXion Holding (INXN). The merger which is expected to close in 2020 will further strengthen DLR’s position among data center REITs. Post-merger, DLR will be the second largest (by enterprise value) data center REIT globally with industry leading EBITDA margins. INXN has a strong presence in European metro areas (including Frankfurt, Amsterdam, Paris and Marseille) with ~53 data centers in 11 European countries. We believe this will be complementary to DLR’s European footprint (established presence in London and Dublin). The combination will create a leading pan-European data center presence, offering consistent, high-quality services with low-latency access to ~70% of the GDP in Europe.

INXN has a robust pipeline of data center development projects currently under construction, with over $400 million invested to date and a total expected investment of ~$1 billion. These projects represent roughly a 40% expansion of INXN’s standalone critical load capacity, are significantly pre-leased and are expected to be delivered over the next 24 months, representing a solid pipeline of potential future growth for the combined company.

(source: Company Presentation)

Exposed to Long-Term Secular Demand Drivers

The data center industry is poised for sustainable growth. The demand for data center infrastructure is being driven by many factors, including the explosive growth of data, rapid growth of cloud adoption and greater demand for IT outsourcing. Of these, cloud adoption remains the most significant driver for data center demand.

The majority of enterprises are moving towards private, public and hybrid cloud solutions to meet their IT needs. The overall cloud market has been growing rapidly over the past five years and is likely to continue at double digit growth supported by the major public cloud providers Amazon Web Services (AWS), Microsoft Azure and Google Cloud Platform. These platforms have delivered growth in excess of 30% during 3Q19.

(source: Company Presentation)

DLR’s focus in primarily on the hybrid cloud solutions market. A hybrid cloud solution allows companies to store their sensitive information on private cloud (servers) while using public cloud-based applications (such as Office 365, Salesforce) that reduce IT costs. Hybrid cloud is the largest part of the industry (almost 69% of companies deploying it) followed by public cloud (such as Amazon Web Services, Microsoft Azure). Hybrid cloud models are mostly executed using multi-tenant data centers such as the one’s provided by DLR.

The Internet of Things, 5G, autonomous vehicles and artificial intelligence are some other trends which are driving unprecedented growth of the digital economy, thereby driving demand for data centers.

(source: Company Presentation)

High Occupancy and Retention Ensures Cash Flow Visibility

As of 3Q19, the occupancy rate of DLR’s portfolio was 87.4% and the retention rate was around 85% (above its long-term historical average of ~80%). Occupancy and retention rates are high given high switching costs associated with changing data center facilities. Digital Realty estimates that it costs customers anywhere from $15 million to $20 million to migrate to a new facility. Further, new deployment costs around $15-$30 million creating additional barriers for customers to switch. Once a customer is locked-in, it makes very little sense for them to change data center facility. DLR is beneficiary of this as high occupancy and retention rates ensure robust rental income and cash flow visibility. Moreover, nearly 89% of company’s leases contain base rent escalations that are either fixed (generally ranging from 2% to 4%) or indexed based on a consumer price index. This provides for rental income growth which allows DLR to deliver a high payout and increasing dividends to investors.

(source: Company Presentation)

Favorably Positioned versus Key Competitors

When analyzing DLR’s performance across its Blue-Chip REIT peers and Data Center REIT peers, we note that DLR is favorably positioned when it comes to topline revenue growth, EBITDA margins, dividend yield and payout ratios. Relative to other blue-chip REITs, DLR is the fastest growing REIT with highest FFO per share growth during 2006-2018 as shown in chart below. When benchmarked against data center REITs, DLR is the second-largest data center REIT globally, behind Equinix, the interconnection giant. DLR is the third fastest growing REIT with the highest EBITDA margins; forecasted to be 58.4% in 2019E, a testament to the company’s superior operational efficiency. The company also falls in the upper range of Dividend Yield and AFFO Payout Ratios.

(source: Company Data)

DLR’s EBITDA margins above peers; Payout Ratio Solid as Well

(source: Company Data, Thomson Reuters)

Investment Grade Balance Sheet

Digital Realty is one of only three investment-grade data center providers. This provides easy access to capital which is important in a capital intensive business such as DLR’s. It positions the company to continue to take advantage of strong secular demand trends in the coming years and also allows it to be opportunistic to pick up distressed assets at attractive prices if market conditions deteriorate. The investment grade status enables an estimated interest rate savings of 50- 100 bps compared to the high yield market, resulting in higher Normalized FFO per share. This equates to $5-10 million in annual interest savings for every $1 billion in incremental debt.

As seen in the chart below, there is virtually no near-term debt maturity. Also, half of the debt is non-US dollar denominated acting as a natural FX hedge for investments outside the US, ~82% of the debt is fixed rate to guard against a rising rate environment and 99% of the debt is unsecured, providing the greatest flexibility for capital recycling.

(source: Company Presentation)

Valuation:

On a Price to Adjusted Funds from Operations basis (“AFFO”) basis, DLR is inexpensive relative to its peer group average. As seen below, DLR trades at a P/AFFO multiple of 17.4x, which is a ~10% discount to its peer group average multiple of ~19.3x. In our view, the discount should narrow given DLR’s strong operating performance.

(source: Thomson Reuters)

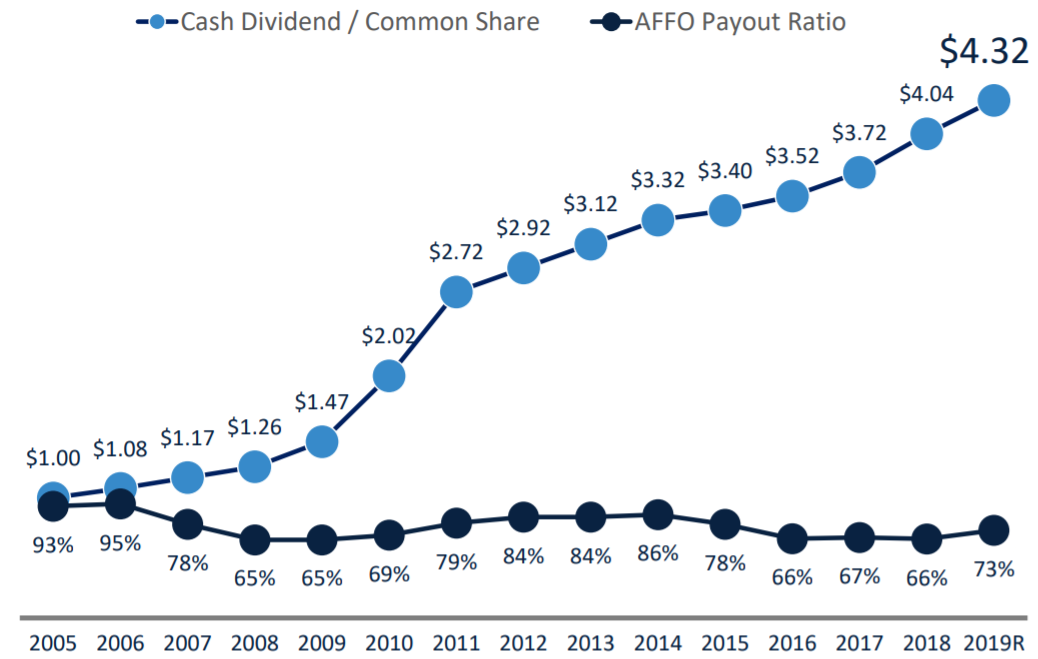

Dividend Safety:

DLR has delivered strong annual dividend growth since 2005, growing its dividend from $1.00 in 2005 to estimated $4.32 in 2019. This represents a CAGR of ~11% during 2005-2019E and also 14 consecutive years of dividend increase. At today’s price near $116.74, DLR current yield equates to ~3.7%. The company estimates its AFFO payout ratio to be ~73% for this year. This is below its historical average of 77% and as such, we believe there is room for DLR to bring this figure out to historic levels and pay out more dividends to shareholders. DLR has no debt maturing until 2021 which provides it with ample cash flow to not only pay its dividend but continue to raise it over time. This contributes to our view that DLR’s dividend is secure, and we are likely to see meaningful increases over time.

(source: Company Presentation)

Risks:

Technology disruption: The current market environment is favorable for data center operators as enterprise and IT customers continue to outsource and decentralize their IT operations. We acknowledge that this could reverse, pushing companies back to sourcing their own requirements internally, thereby decreasing demand for data center space.

Reliable Infrastructure: The business depends on providing customers with highly reliable services, including with respect to power supply, physical security and maintenance of environmental conditions. If these infrastructure components break or are rendered obsolete, it may lead to loss of customers thereby adversely impacting earnings.

Competition: DLR competes with numerous data center providers, many of whom own properties similar to DLR in the same metropolitan areas. Some of competitors and potential competitors have significant advantages, including greater name recognition, longer operating histories, pre-existing relationships with current or potential customers, significantly greater financial, marketing and other resources and more ready access to capital. In addition, many of the competitors have developed and continue to develop additional data center space. If the supply of data center space continues to increase as a result of these activities or otherwise, rental rates may be reduced which will negatively impact operating results.

Conclusion:

Digital Realty presents an attractive opportunity for investors seeking a healthy growing dividend, combined with significant long-term price appreciation potential, thanks to expected growth in data center demand and DLR’s well-run business. Further, we believe many income-focused investors often overlook this attractive opportunity because the yield (currently only 3.7%) is lower than the dividend yields offered by other REITs. For example, we were unable to include Digital Realty on our recent ranking of Top 10 Big-Dividend REITs because a 3.7% yield didn’t make the cut (if you’re curious, our write-ups on EPR Properties’ 6.6% yield and Brookfield Property REIT’s 7.2% yield did make the cut, ranked #10 and #7, respectively). Nonetheless, a 3.7% dividend yield is nothing to bat your eye at, especially considering the powerful dividend growth and attractive long-term price appreciation potential. We currently own Digital Realty within our Blue Harbinger Income Equity portfolio.