Dow Inc. (DOW) is one of the largest chemical companies globally. In this report we analyze the company’s business mix, cash flow and income prospects, and finally conclude with our opinion on whether the company’s stock offers an attractive balance between risks and rewards.

Key Takeaways:

Market leading position and a more focused business post reorganization.

Company is set to generate significant amount of cash flows over the next two years.

Trading at nearly 11% 2020 FCF yield and 5.1% dividend yield, a significant discount to peers.

Overview:

Dow Inc. (DOW) produces and markets a variety of chemical products with application in specialty plastics, packaging, Hydrocarbons/energy products as well as home care and personal care products. The company was spun out of DowDuPont in April 2019.

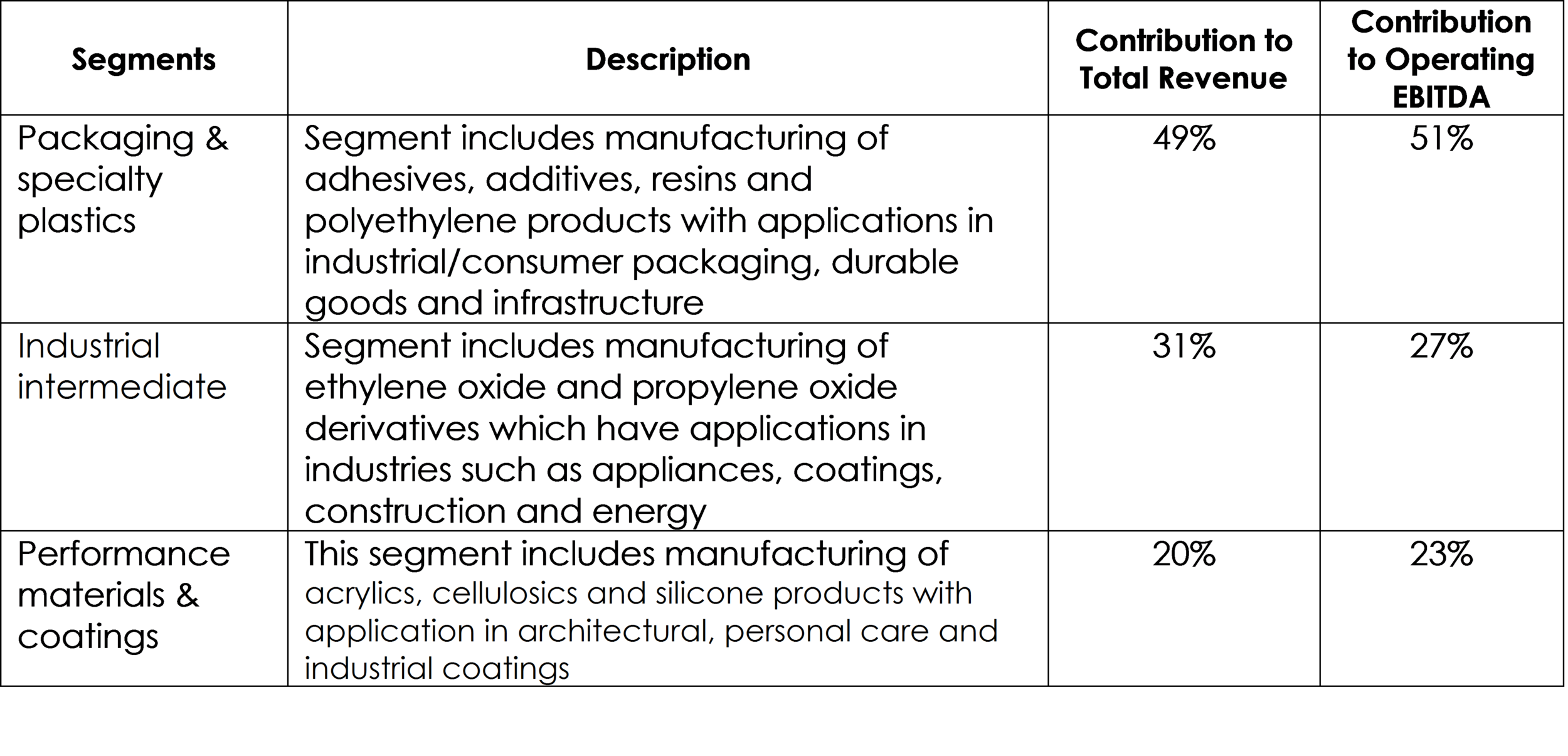

The company divides its products into three segments:

Source: Dow Inc

A global, chemicals behemoth with eventful last few years…

Dow Inc. is a leading chemical company with strong presence across end markets and geographies in the materials science market segment. The company participates in addressable markets worth $350 billion and it generated $50 billion in sales in 2018, implying ~14% share in its addressable markets. The company is a market leader in many important applications such as Polyethylene, Propylene Glyco, Architectural Coatings, Acrylic Acid, Siloxanes & Silicones. Dow derives over 63% of its sales from outside the US and is truly a global barometer of economic activity.

Dow and DuPont decided to merge in 2017 with the aim of combining their competing business segments, extracting synergies and then breaking up the combined business into 3 focused businesses and spinning them out to shareholders. A number of activist hedge funds got involved in the process and had a say on how the businesses should be split.

The new Dow is centered around material sciences as compared to the old Dow that had large exposure to agriculture as well, for example. Additionally, not only is the company more focused, it also has a larger footprint within the focus areas due to combination of material science business from DuPont. The new Dow has 3 segments as compared to 5 earlier, and while revenue is similar, EBITDA margin and asset efficiency of the new Dow is superior.

Source: Dow Inc.

Unfortunately, the spin off happened at a precarious time for the global economy

Recent quarters have been difficult for the chemical sector as a whole as global PMIs remain low and subdued industrial activity has put pressure on pricing of important raw materials such as isocyanate and siloxanes.

In the first 9 months of 2019, the company has reported a 13% decline in revenue. The decline was made up of a 10% decrease in price and 2% decrease in volume. Operating EBITDA during the same period contracted by around 22% YoY. However, it is worth noting that Q3 2019 EBITDA grew sequentially compared to Q2 for the first time in one year and the quarterly result was better than management expectations as well as sell-side estimates. Additionally, it is important to note that the company’s German competitor BASF reported a 24% decline in operating profit in Q3 YoY, highlighting that the decline in profitability is not entirely company specific.

Cost savings are an important offsetting driver

Since the merger of Dow and DuPont, the DOW business has cut over $1.37 billion in costs, primarily from headcount reductions but also as a result of lower variable expenses, meeting its cost savings target earlier than expected. The company also recently raised its 2019 cost savings guidance from $600 million to $700 million. While we expect limited cost savings opportunities going forward relative to the what has already been achieved, the company is set to improve its free cash flow generation further.

Source: Dow Inc.

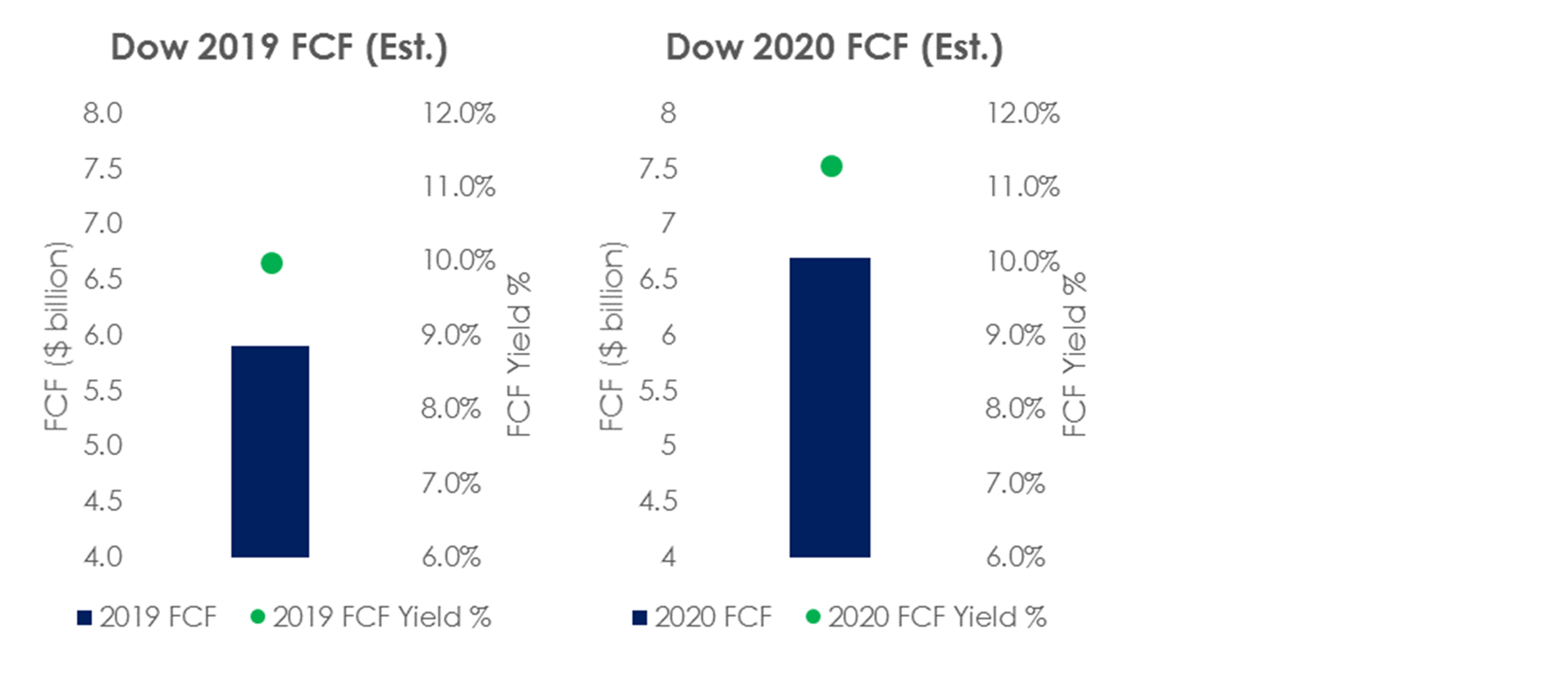

Free cash flows expected to grow

Despite a decline in revenue in the recent quarters, the company has been consistently generating high free cash flow. 2019 YTD, the company has generated $3.2 billion in FCF out of which $1.3 billion was generated in Q3 itself. This was mainly due to improvement in working capital requirement and reduction in integration and separation costs. Not surprisingly, cash flow from operations as a percentage of EBITDA was 96% in Q3 2019. The company’s integration and restructuring costs are expected to see a $1 billion decline in 2020 as compared to 2019. Additionally, the company is further working on reducing investment in working capital in the near to medium term which could further aid FCF. Finally, Dow will also see $100 million in lower interest expense as a result of debt repayment and refinancing. As a result, the company’s 2020 FCF should increase around 15% as compared to 2019 which translates into an attractive FCF yield of 11.3% on the company’s present enterprise value. This favorably compares to BASF’s TTM FCF yield of 2% and 2018 FCF yield of 5%.

Source: Blue Harbinger Research

Superior FCF has enabled deleveraging

The company has done significant refinancing of near debt that has extended its maturity profile with no substantial maturities lined up until 2022. Further, the company negotiated a lower interest rate on part of its term loan. Finally, it redeemed $1.25 billion of debt after it received $0.8 billion from a positive ruling relating to a lawsuit against Nova Chemicals. Total debt has steadily declined over last few quarters. Having said that, the company’s debt to EBITDA has not declined due to fall in EBITDA as a result of ongoing macro issues.

A rare combination of strong cash cushion and high dividend yield

The company is currently providing investors a dividend yield of 5.1%. Pre-merger, the old Dow traded at around 3% dividend yield and therefore the current dividend yield is higher than the yield the company provided in its previous avatar. Additionally, the company’s 2020 FCF is likely to be at least 4 times the dividend payment providing the company with plenty of cushion should there be a protracted cyclical slowdown.

Risks

Cyclicality could overshadow organizational improvements

The company has made significant strides when it comes to resizing the cost structure and improving FCF generation. However at the end of the day it operates in a highly cyclical business which is impacted by global factors, especially demand out of China. A deep and protracted cyclical slowdown will reduce the near term earnings power of the company. Having said that, the company has successfully extended its debt maturities and has ample earnings cushion to weather a storm.

Large international business brings currency risks

The company has a large international presence including exposure to emerging markets. Weakness in emerging market currencies against the dollar could impact the company’s financials however typically these are short term impacts that do not alter the long term thesis on the company.

Conclusion

Post reorganization, the new Dow has emerged stronger and more focused. The company is set to generate significant levels of FCF over the near to medium term despite the current downturn in the macro economy. And despite strong FCF generation and a market leading position, the company’s shares offer an appealing dividend yield of 5.1% which provides investors with a strong risk-reward balance. If you’re looking for a healthy blue chip dividend, and mid to long-term price appreciation potential, Dow is an attractive opportunity that is still flying a bit under the radar (to many dividend investors) simply because it has newly reemerged as a standalone company following its recent reorganization.