The market opportunities for high-yield Business Development Companies ("BDCs") have changed significantly in recent years, and Triangle Capital’s (TCAP) management is not able to keep up. However, Benefit Street Partners and Barings do have what it takes. And if you are not aware, TCAP announced last month that it is selling its investment portfolio to Benefit Street Partners for cash; and Barings will become the company’s new investment advisor. The deal is expected to close in June or July of this year. And in our view, this liquidation is NOT ideal, however it is still VERY attractive for TCAP shareholders, and we intend to continue holding our TCAP shares within the Blue Harbinger Income Equity portfolio.

The Deal Is NOT Ideal:

Before explaining why this deal is very attractive to current TCAP shareholders (and new investors), we first explain three reasons why we believe this deal is NOT perfect.

1. TCAP should have addressed its challenges sooner.

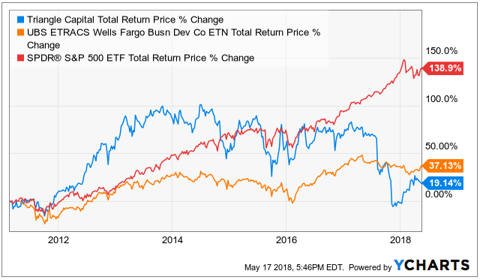

For perspective, here is a look at the total return (dividends plus price appreciation) for TCAP versus a BDC index (BDCS) and the S&P 500 (SPY) since 2011.

TCAP's performance was strong, it leveled off, and then it basically tanked. And here is a look at the dividend yield and the quarterly dividend per share (the dividend was recently cut twice!).

The reason TCAP's performance was strong in 2012 through 2014 is because it had the right strategy for those market conditions. Specifically, it was able to provide loans to middle market companies at a time when market conditions were stressed because banks wouldn't make these loans (too risky), but TCAP would and TCAP was able to charge high interest rates. And as the market improved, so too did the value of TCAP's portfolio.

From 2014-2016, TCAP's performance leveled off because there simply weren't as many attractive very-high-yield loan opportunities because market conditions had improved. And from 2016-2018, the market has been so strong that credit spreads have narrowed, and there really aren't that many attractive new high-yield opportunties for TCAP to pursue, at all. Further the loans that remained on their books (i.e. the ones that hadn't already been repaid or refinanced) were difficult for TCAP to manage (especially after TCAP's CEO then CIO stepped down in 2016 (see: Triangle Capital CIO exits and Triangle Capital CEO steps aside).

The bottom line here is that it would have been better for TCAP shareholders if TCAP addressed changing market conditions sooner, but it did not. And as such, the existing TCAP management team is overwhelmed with the lower quality assets that remain on the books. This is not an ideal situation that TCAP could and should have addressed sooner.

2. Some shareholder rewards will be shifted to Benefit Street Partners.

Because TCAP is selling its entire investment portfolio to Benefit Street Partners (as of 12/31/17), TCAP is essentially transferring some future economic benefits away from current shareholders and instead to Benefit Street Partners. Granted TCAP is not equipped to handle its current investment portfolio (i.e. it is too complicated, too concentrated in high risk opportunities, and the future returns will be too lumpy for TCAP shareholders liking), but there are very significant benefits that Benefit Street will likely recognize at some point in the future (because Benefit is a much larger, more diversified organization that is better equipped to manage the portfolio) otherwise they wouldn't be buying in the first place. Granted the share price of TCAP jumped on the news of this deal, and TCAP shareholders will be receiving a premium (cash in excess of book value), but Benefit Street believes the portfolio has even more long-term value to them, otherwise they would be buying.

3. A lot of non-shareholders have their hands in the cookie jar.

Transaction costs are never free, and in this case a lot of costs (at TCAP shareholder's expense) will be transferred to investment bankers, strategic advisors and lawyers). If TCAP could have avoided this situation (by not getting themselves into this situation in the first place), shareholders would not be coughing up all of the costs associated with this transaction. Further, if TCAP's management was able to manage the existing portfolio, that would have been better for shareholders.

The Deal Is Still Very Attractive:

Despite the three reasons this deal is NOT ideal (as described above) the deal is still very attractive, nonetheless, for the three reasons described below.

1. Shareholders get a much needed portfolio "reset" relatively quickly.

In a move to make other struggling BDCs envious, Triangle's portfolio gets reset relatively quickly. When the transaction is complete (expected in June or July) Benefit Street will take the trouble assets off TCAP's books and replace them with cash. This is much quicker and more efficient than if TCAP tried to reposition the portfolio asset by asset. Further, the new manager, Barings, will invest the cash in highly liquid assets at first, and then reinvest it in more attractive, high quality, middle market investments over the next two years. This is a very attractive situation because it allows the new portfolio to acquire assets that are attractive now, instead of continuing to own legacy assets that were more attractive in the past.

As such, the $0.30 quarterly dividend will be discontinued starting with the second quarter of 2018. However, shareholders will receive a payment of $1.78 per share as part of the Barings externalization transaction, which is expected to close in June or July of this year. Further, new manager Barings has a target 8% long-term dividend yield, but is initially targeting 6% until the cash received is more fully invested over the 2-year period described above. This lower yield is more sustainable than the current yield, it will be more constructive to the security valuation/price, and 8% is still an attractively high long-term dividend yield target.

Very importantly, the "reset" allows the new management team (Barings) to invest in the assets that are most appropriate given current market conditions. And this essentially means higher quality assets, despite the lower (yet still very high) yields. Also, very importantly, TCAP can now take on additional leverage after the legally allowed leverage limit for BDCs was increased to 2x from 1x in March after the White House signed new legislation. This creates a significantly more attractive environment for TCAP, especially given the portfoli reset.

2. TCAP shareholders get a better manager.

Barings, the new external manager, has significantly more experience and expertise than the current TCAP management team. For example, Barings is a leading global asset manager with over $300 billion of assets, over 650 investment professionals, and has significant experience managing both public and private funds. You can read more about Barings and the transaction in this TCAP presentation. Further still, the deal allows the new organization to access lower cost borrowing because of the improvement to the underlying portfolio and because of the financial strength of Benefit Street.

3. The deal also benefits Benefit Street and Barings

This deal also benefits Benefit Street and Barings (otherwise they wouldn't do the deal), and this is a good thing for shareholders. For one thing, Barings and Benefit Street don't have to go through the hassles of creating a new BDC (they're taking over an existing BDC, TCAP). Second, they're getting the 3 SBC licenses that TCAP already has. SBC licenses are particularly adventageous for small BDCs like TCAP (TCAP's market cap is only $545 million) because the attractive SBC financing deals (far better risk/reward tradeoffs than open market deals) makes a significant impact on the bottom line (because TCAP isn't that large). And this falls through to benefit TCAP shareholders.

Conclusion:

The Triangle/BenefitStreet/Barings deal is NOT ideal (for the reasons described earlier), however it is very attractive to existing TCAP shareholders, nonetheless. It benefits shareholders because it allows the portfolio to be reallocated relatively quickly based on current market conditions. It also gives shareholders a better investment manager with wider and deeper skills and resources. And finally, the new deal will result in a new underlying investment portfolio for existing shareholders that is more appropriately constructed and sustainable over the long-term. We view this deal as incrementally very positive, and we continue to own shares of this high-yield BDC in our Blue Harbinger Income Equity portfolio. On a go-forward basis, we expect healthy long-term high-yield and a significantly stronger share price.

You can view all of our current holdings here.