Our long-term track record of gains and market-beating performance grew in December as we capped off another year of strong performance. This week's Blue Harbinger Weekly provides a quick update on each of our current holdings. We're excited about these stock specific ideas, as well as the additional gains that could be achieved from continuing market wide economic strength. And as a quick reminder, compound growth is a powerful wealth builder, and the tortoise beats the hare.

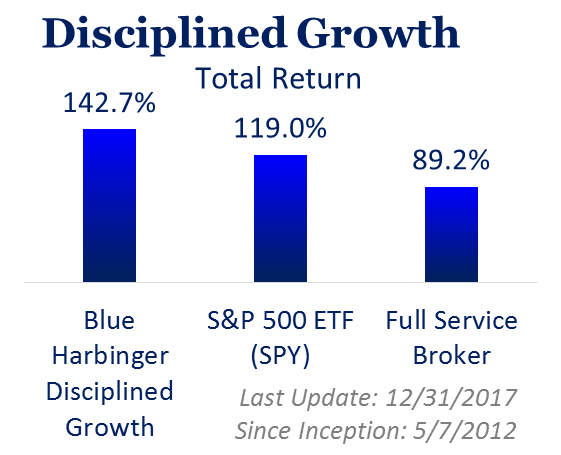

You can access our current holdings and performance here.

Here is a brief update on each of our current holdings...

- Accenture (ACN): Accenture beat earnings estimates and raised guidance in December, thereby posting a healthy total return of 3.4% for the month. We continue to believe in the business model and workforce, and believe this technology consulting and outsourcing company will benefit as the economy continues to grow, and it deserves a higher/premium valuation.

- ADP (ADP): After some bickering back and forth with activist investor, Bill Ackman, ADP appears to be refocusing on its business. Ackman did have a point, mainly there are ways to grow earnings and earn a higher earnings multiple from the market. ADP returned 2.9% in December, and we believe it has continued healthy upside, especially as the global economy remain strong.

- Adams Diversified Equity Fund (ADX): Hopefully you owned this one for the big outsized dividend in December (it was larger than expected). We continue to like the management team, holdings, and discount to NAV for this high-yield closed end fund. If you are an income-focused investor, ADX is worth considering.

- American Express (AXP): Unlike payment processing companies like Visa and MasterCard, American Express is actually a bank, and rising interest rates will continue to boost the returns for this strong-brand-name blue chip. New Tax reform should also decrease American Express’ tax bill in a meaningful way (i.e. more upside to the stock price).

- Disney (DIS): This stock is starting to perk up, gaining 3.4% in December. Negative narratives about cable cord cutting and struggling ESPN are finally giving way to positive news like potential for streaming market share and intellectual property to grow with the acquisition of Fox. Plus many of the storied Disney franchises are timeless.

- EastGroup Properties (EGP): This industrial property REIT sold off in December (down 5.4%) and we believe that has created a very attractive opportunity to buy shares of this healthy prime-location 3.0% yield REIT.

- Emerson Electric (EMR) has been on fire gaining 7.5% in December, and already adding another 4% in 2018. The market liked that EMR dropped its bid to acquire Rockwell Automation, as this St Louis based industrial manufacturer will benefit from the Tax Cuts and Jobs Act.

- First American Financial (FAF) put up a solid 1.5% total return in December as the commercial and residential real estate market continued to strengthen (FAF provides title insurance and related services). This stock put up outstanding numbers in 2017, gaining roughly 50%, and the 2.6% dividend yield is nice too.

- Facebook (FB): We own Facebook in our Blue Harbinger Disciplined Growth portfolio, and it countinues to benefit from two things. One, the strong rally is aggressive growth large cap technology stocks. And two, Facebook continues to expand and grow its advertising revenues on an incredibly scale. Yet there is still more room to run as the total addressable market is enormous, and the company’s expansion into virtual reality only adds to the size of the pie.

- General Electric (GE): This is a very attractive value stock. The market hates this company after cutting the dividend. But the old management team is gone, new management is righting the ship, and this company is being assigned far too low of a valuation by the market. GE generates enormous revenues, and as new management improves operations, this stock price is going up.

- International Business Machines (IBM): Yes, IBM is a dinosaur, but it legacy business will continue to provide huge revenues for years to come as its strategic initiatives grow. We believe IBM is an attractive large cap value stock, the shares are already up 6% in 2018, and the 3.7% dividend is safe and attractive.

- Large Cap Value ETF (IWD): we wrote about “risk creep” a few weeks ago, whereby investors should be careful not to chase after all the stocks that have been performing best lately (e.g. Amazon, Netflix, Google). Value stocks tend to outperform growth stocks over market cycles, and this low cost ETF provides efficient low-cost exposure to contrarian large cap value stocks, which are particularly attractive right now from a contrarian standpoint.

- Small Cap Value ETF (IWN): Similar to our large cap value ETF, this small cap value ETF is a contrarian investment that produces powerful returns over market cycles. We believe small cap value stocks are due for a rebound, and when it happens it will likely be swift and powerful.

- International EFT (IXUS): If the US economy keeps booming, the US dollar will likely strengthen, and that could make international products less expensive and more attractive thereby kicking off a rally in non-US stocks. Regardless, we like to have some international exposure for diversification purposes, and this is an attractive low-cost way to play it.

- Johnson & Johnson (JNJ): This is a blue chip among blue chips. It has (and we believe it will continue) to put up steady, healthy returns for many years. The dividend is attractive at 2.4%, and it’s a basic staple in many healthy, long-term, income-focused investment portfolios.

- New Residential (NRZ): With a yield of over 11%, NRZ grabs the attention of many investors. We believe management continues to do an outstanding job of evolving with the residential mortgage industry (e.g. their recent acquisition allows them to do some mortgage servicing which alleviates some risks and increases growth opportunities for NRZ). And as long as the company keeps staying ahead of the curve, this dividend is safe and the shares are attractive.

- Omega Healthcare (OHI): The shares sold off after another tenant reported liquidity challenges. Specifically, the company was already facing some challenges with tenants Genesis and Signature Healthcare, but more recently Omega announced challenges with Orianna Health Systems (Orianna has been put on a cash basis). Importantly, these operators continue to make payments, and the best time to buy is often when the market is fearful and shares have sold off.

- Paylocity: We continue to like this growth story. This cloud-based payroll processing and human resource company continues to put up impressive growth numbers, and there is more room to run considering it offers extremely competitive lower cost services for small and mid-sized companies. Plus, a strong economy and rising interest rates benefit Paylocity as well, as business grows and the company earns incrementally more on the carry for the external company payrolls it administers. Eventually, Paylocity will stop speding so heavily on growth, and it will turn into an impressive cash cow because one companies have set up their payroll, they do not like to change it (i.e. Paylocity’s business has very low turnover). Paylocity does NOT pay a dividend, but the shares were up around 60% in 2017, and there is more room to run.

- Procter & Gamble (PG): This is a relatively low-risk, healthy-dividend, blue chip company, with plenty of growth opportunities in emerging markets. This is also a staple within many long-term, low-risk, income-focused portfolios.

- Phillips 66 (PSX): These shares have been very strong in recent months, but have more room to run as the market still values the steady long-term income contracts incorrectly. Specifically, the market thinks of PSX as a refiner (and assigns a lower valuation multiple consistent with other refiners) however PSX has expanded into the steady healthy long-term midstream business which not only creates a lot of income but also deserves a higher valuation multiple.

- Royce Value Trust (RVT) and Royce Micro Cap Trust (RMT): If you like small cap value stocks like we do, and you are an income-focused investor, RMT and RVT are attractive. Not only do they offer attractive exposure to small cap value stocks (which tend to outperform over long-term market cycle and are due for a healthy contrarian rebound), but we like the low cost, seasoned management team and discounted prices (versus NAV) for these two closed-end funds. The yields are both well over 7%.

- Triangle Capital (TCAP): This stock had all the signs of a quality investment, but it turned out to be a disaster in 2017. With zero warning, management slashed the dividend and lowered guidance and the shares lost a significant amount of value. We believe business development companies (such as this one) should be able to find healthy opportunities in the current market environment, but TCAP has struggled to transition as legacy investments have rolled off their books. Despite management mistakes, we believe the shares have sold off too far, and we continue own TCAP, which currently offers a 12.7% dividend yield.

- Tekla Health Care Closed End Funds (THQ) and (THW): If you believe in the healthcare sector, and you like large distribution payments, these two closed end funds are an attractive option to consider. Not only do they provide attractively actively managed exposure to the health care sector, but they pay big distribution yields and they trade at discounted prices relative to their net asset values (“NAVs”).

- Tsakos Energy Navigation (TNP): We believe this big-dividend (5.0%) seaborne transportation company is trading at an attractive price because the market is too backward looking. Specifically, the market cycle is turning, and Tsakos is well-positioned as the competition has been reduced and has not been able to operate as efficiently as Tsakos. We’ve written in detail about Tsakos recently, and it also offers attractive high-yield preferred shares that investors may want to consider too.

- Union Pacific (UNP): This is a bet on the strength of the US economy as rail transportation remains an efficient form of transportation for a variety of products. UNP’ strategic access to west coast ports allows it to access enormous business from imports and exports to the East (e.g. China). Shares were very strong in December as the economy grows and UNP benefits from tax reform. More room to run.

- US Bank (USB): We like this very large regional bank because it avoided much of the distress assets that plagued the bigger bulge bracket banks. USB is well run and will benefit from increasing net interest margins as interest rates rise and the economy continues to strengthen. This is a far more efficient bank that it used to be just years ago. The company is handing out raising following recent tax reform, and there is a lot more room for this 2.2% dividend yield company to grow.

- Williams Partners (WPZ) delivered a 5.7% total return in Decemeber and the yield is 5.8%. This natural gas infrastructure company continues to benefit from lucrative long-term low-risk relationships with natural gas companies, as well as support from Williams Companies (WMB). If you’re looking for a steady high-yield, WPZ is wo

- Westar Energy (WR): This Topeka Kansas based electric utility company has been unusually volatile as the market digest the regulatory back-and-forth and ultimate approval of tis merger with Great Palins Energy. We believe the final decision lifts the uncertainty and clears the way for more upside for this electric utility company operating in a healthy market.

Honorable Mentions...

WP Carey REIT (WPC): Buy low, as the saying goes. Shares of WPC pulled back 1.8% in December while much of the market gained, thereby providing an attractive entry point for buyers. As we’ve written about recently, WP Carey is a strong well-diversified REIT with a big safe yield of 6.0%.

- AmeriGas (APU): AmeriGas gained 3.0% in December, but it’s added another 4% to that already in January as the cold weather is expected to increase propane sales. This cold weather is what we’ve been waiting for, and it’s the reason why APU is attractive (besides the big distribution yield of 8.0%).

- Enbridge Energy Parners (EEP) was down 5.5% in December, but is already up 8.1% in 2018, as the market adjusts to energy market volatility and tax reform. EEP is hated after significantly cutting its distribution in 2017, however we believe this 9.4% yielder still trades at a discount.

Conclusion:

All too often investors chase after hot flashy stocks, and they end up getting burned. Slow and steady long-term investing is a proven strategy for success. And as a quick, but important, reminder, here are our...

And as a final reminder, don't get cute and try to chase hot stocks... the tortoise always beats the hare.