Simon Property: 4.2% Yield, 25% Upside

There’s a false narrative going around that the Internet is going to put all “brick and mortar” stores out of business. And while this may be true for some stores, it’s certainly not true for all of them. For example, we believe big-dividend (4.2% yield) Simon Property Group (SPG) isn’t going out of business anytime soon (SPG owns and operates premium shopping malls). In fact, SPG is growing, its shares have inappropriately sold off, and it currently presents a very attractive buying opportunity for income-focused investors that would like to see some capital appreciation too (we believes the shares could easily trade 25% higher within the next year).

A Summary of the Business

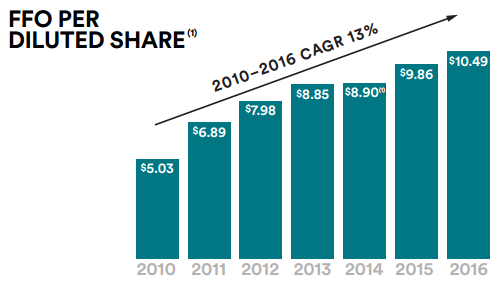

Despite the narrative that retail properties will be made obsolete by online shopping, Simon Property Group continues to grow. The company owns high quality retail properties and achieved record Funds from Operation (“FFO”) of $3.8 billion in 2016.

Stores represent 90% of the total retail sales pie of $4.5 trillion. And “brick and mortar” stores also generate 67% of the ecommerce sales pie.

SPG’s properties are diversified by asset type across US malls, Premium Outlets, “The Mills,” and international.

SPG announced a dividend increase in the first quarter of 2017, and repurchased 1.4 million shares in the forth quarter, both signs of financial strendth. SPG also has the highest investment grade ratings among US retial real estate companies, and remains one of only two US REITs with an “A” or “A2” stable outllok credit rating from S&P and Moody’s, respectively.

Valuation

At only 15.3 times Price/FFO, SPG currently trades near the lower end of it historical P/FFO range (excluding the distress of 2008—2009).

We believe SPG shares could easily trade back up to a more normal 18 times FFO. If the shares were to trade at 18 times the midpoint of management’s 2017 FFO guidance of $11.45 to $11.55, then a price of $207 per share is not unreasonable. And considering SPG’s current stock price, this gives the shares 25% upside if they were trade back to a conservative 18 times FFO, a price that is not unreasonable.

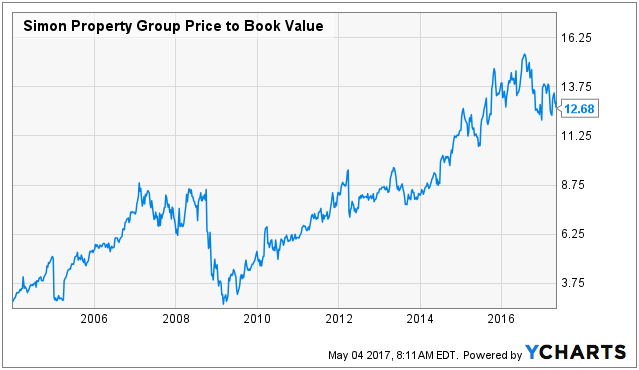

SPG’s Price to Book Value has climbed in recent years as the company grew, strengthened its financial wherewithal, and focused its business by spinning off risky properties into a separate REIT, Washington Prime Group (WPG), in 2014. Over the last year, the P/BV has pulled back significantly making for a more attractive entry point for investors.

SPG shares have traded lower over the last year for two main reasons. First, the narrative that all retail stores will be replaced by online merchants has stoked fear among investors. And second, dividend stocks in general have sold off as the “Trump Rally” focused on growth stocks and frightened investors about faster interest rate increases than previously expected (REITs rely on borrowing to finance growth).

Competition

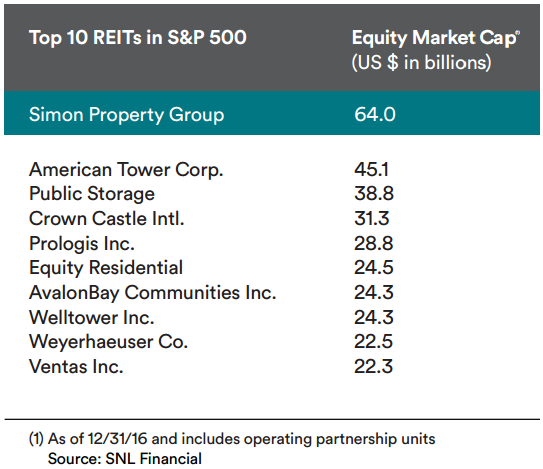

SPG is the largest retail REIT (2.5 times the size of its next largest competitor). SPG also has premium properties, and a higher credit rating than its peers.

As mentioned previously, the total retail market size is $4.5 trillion, and online sales make up 10% of this amount. Shoppers will likely continue to choose retail shopping (over online) for major purchases. Further, SPG own premium properties, and has already spun off its lower quality (riskier) properties in to a separate REIT. Relative to lower property-quality REITs, SPG will likely be less challenged going forward.

From an industry standpoint, SPG CEO David Simon explained in his year-end 2016 letter to shareholders, that SPG faces both cyclical and structural challenges. Cyclical challenges (such as low wage and GDP growth, lack of exciting fashion trends, the stronger dollar affecting tourism, and demographic shifts will pass. Structural changes are more challenging. Specifically, the internet is a force to deal with. Also, Simon believes, “we have too much retail per capita in the US. Some of it will become obsolete, and though we have little exposure to this, the industry will feel the pain and this feeds the narrative.”

Catalyst

REITs have recently underperformed the S&P 500 (especially retail REITs) over the last year, and they are relatively inexpensive from a valuation standpoint because investors have been favoring growth stocks. However, any volatility in the markets could fuel a “flight to quality” which would benefit steady “risk-off” big-dividend payers such as SPG. Additionally, improvements in retail real estate prices fueled by less aggressive interest rate hike expectations could both drive the share price higher.

Important also, as contrarian investors, it can be wise to make long-term investment decisions based on valuation and outlook, instead of waiting for a short-term catalyst. As Warren Buffett is often quoted as having said…

“…if you wait for the robins, spring will be over.” -Warren Buffett

Additional SPG securities

Worth noting, in addition to common stock, SPG also offers a variety of publicly traded bonds as well as shares of preferred stock. For example, the following table shows the outstanding SPG bonds.

Regarding preferred shares, the Series J Cumulative Preferred shares (SPG-J) currently trade at $70.65 and offer a 5.92% dividend yield. More specifically, SPG is on the hook for Chelsea Property Group, 8 3/8% Series A Cumulative Redeemable Preferred Stock, liquidation preference $50 per share, redeemable at the issuer's option on or after 10/15/2027 at $50 per share plus accrued and unpaid dividends, with no stated maturity, and with distributions of 8.375% ($4.1875) per annum paid quarterly on 3/31, 6/30, 9/30 & 12/31 to holders of record on the 15th day of the month in which the payment is due or on the day fixed by the board, not more than 30 days or less than 10 days prior to the payment date. Dividends paid by preferreds issued by REITs are NOT eligible for the preferential 15% to 20% tax rate on dividends and are also NOT eligible for the dividend received deduction for corporate holders. In regards to payment of dividends and upon liquidation, the preferred shares rank equally with other preferreds and senior to the common shares of the company.

We are not interested in owning the bonds or the preferreds at this time because given the recent price performance, we believe the common stock offers the most attractive return opportunity.

Recent Price Action

The common shares have trade down more than 25% since August 2016 while the S&P 500 is up 10% (the preferreds have also outperformed the common). The common shares have traded lower for two main reasons. First, the Trump Rally has favored growth stocks and put selling pressure on dividend stocks in general. Additionally the Fed has continued to raise interest rates thereby putting downward pressure on REITs which rely largely on debt to finance growth (we believe the market has overreacted considering SPG’s current valuation on both a price to FFO and price to book value basis.

Worth noting, short interest has been increasing for SPG (currently 3.72% of the shares outstanding) as the negative narrative for retail REITs continues.

Conclusion

Simon Property Group is a very profitable REIT that generates strong and growing funds from operations. It trades at very attractive valuation multiples relative to its historical range, and we believe REITs in general (and high-quality retail REITs, in particular) have significant upside potential because the market narrative is overly pessimistic, in our view. If you are an income-focused, contrarian investor that appreciates significant price appreciation potential, Simon Property Group is worth considering.