Investors are often lured in by high yields, only to later discover they've purchased a value trap. This report reviews why we believe one particularly popular high-yield equity is NOT worth the risk, and why we wouldn't touch it with a 10-foot pole. However, there is another point in the capital structure of this particular high-profile company that may be worth considering.

CBL & Asscociates Properties (CBL), Yield: 14.7%

CBL is a big-dividend shopping mall REIT that announced a dividend cut in November, and the share price fell so far (-30%) that the yield has already climbed up to 14.7%. However, before you go chasing after this yield, we suspect it's a value trap. Even though this company could miraculously turn itself around, we believe it's too risky and the shares will likely fall further (as we have described in our detailed report below). You can read all about our views on this REIT below, and you can also read all about of views on the debt (the bonds) in this report:

The bonds are still trading at an attractively discounted price, and they may be worth considering if you are an income-focused investor (see link above). However, the stock is likely a value trap, in our view. And in case you are feeling bold, and considering the stock, here is our latest write-up on the stock for you to consider...

We rate CBL & Associates a SELL

Summary:

- CBL & Associates Properties, Inc. is a B-class shopping mall owner and operator (organized as a REIT), and following last month’s announced dividend reduction, the shares are now down over 50% year-to-date. Equity shares fell nearly 30% following the dividend cut announcement, and CBL’s 2024 bonds fell to $90.00 from $96.50.

- Like most “brick and mortar” property owners, CBL has been challenged by the evolving retail industry including the growth of online shopping (thereby increasing competition) as well as less demand for B-class mall owners in particular (e.g. lower rent per square foot properties, like CBL’s) that has been resulting in tenant bankruptcies (e.g. Toys"R"Us, Perfumania and Vitamin World filed in Q3), and undesirable rent concessions being offered by CBL.

- Over the last four years, CBL management has been working to reposition (improve) the portfolio and increase liquidity via over 40 property transactions (many sales). However, CBL was recently forced to lower its already conservative guidance and reduce the dividend (the dividend cut will preserve an estimated $50 million in annual cash flow)

- FFO per diluted share, as adjusted, was $0.50 for the third quarter 2017, compared with $0.57 per share for the third quarter 2016. Third quarter 2017 was impacted by approximately $0.02 per share of dilution from asset sales.

A Summary of the business and the industry

CBL & Associates Properties (CBL) is a regional shopping mall REIT. The company owns and operates 119 properties located mainly in the Southeast and Midwest regions of the US.

CBL is a “B-class” mail REIT, an area that has faced challenges, and will likely continue to face challenges from struggling retailers. As consumer shopping habits continue to change (for example, online shopping such as Amazon), CBL is forced to deal with increasing bankruptcies from its tenants, as well as being left with no choice but to lower rents for tenants that simply cannot stay in business at current rental rates. In some cases, CBL has been selling properties to raise cash.

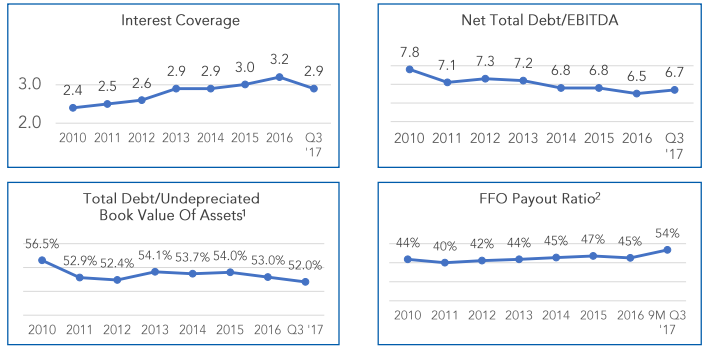

CBL has been making efforts to improve its portfolio as shown in the following graphic.

Management believes the portfolio is stronger as a result of the nearly 40 properties, including more than 20 malls, which they have sold or transacted on in the past 4 years.

Brief History of the Company and its founding

CBL is named after Charles B. Lebovitz. In 1961, Moses Lebovitz, Charles Lebovitz, and Jay Solomon founded Independent Enterprises; in 1970, the company merged with Arlen Realty & Development Corporation, which owned shopping centers on the East Coast of the United States; and in 1978, Charles Lebovitz and 5 associates formed CBL & Associates, Inc. In 1993, CBL & Associates Properties, Inc. was formed as a REIT and acquired all of the assets of CBL & Associates, Inc. The company became a public company via an initial public offering.

Valuation:

Relative to its own historical level, CBL’s EV/EBITA ratio has declined sharply as shown in the following chart.

The company has already been forced to reduce rents charged to tenants and deal with bankruptcies, and the market is assigning a low valuation multiple implying there may be more pain and challenges to come.

CBL’s funds from operations (“FFO”) per shares has already come down ($0.50 in the third quarter, versus $0.57 in the same quarter last year), and the company trades at an extremely low 2.7 times expected 2017 Adjusted FFO.

Also, the company’s public equity value (market cap) is $975 million, whereas the value of equity on its balance sheet is $1.1 billion. The low market value and CBL’s high debt load (debt is 75% of assets) suggests CBL may face more significant challenges ahead.

On November 6th, S&P Global Ratings lowered its corporate credit rating on CBL to 'BB+' from 'BBB-'. The outlook is stable.

According to a November 6th note from Debt Wire:

“We affirmed our 'BBB-' issue-level rating on subsidiary CBL & Associates Limited Partnership's senior unsecured notes and assigned a '2' recovery rating indicating our expectations for substantial (70-90%; rounded estimate: 80%) recovery in the event of a payment default. At the same time, we also lowered our issue-level rating on the company's preferred shares to 'B+' from 'BB'.

The downgrade reflects CBL's weaker-than-expected operating results in the third-quarter-ended Sept. 30, 2017, and lowered guidance for the rest of 2017. CBL reported a total portfolio same-center NOI decline of 2.6% for the three months, and a 1.6% decline for the nine months ended Sept 30, 2017. Based on the lowered earnings guidance for a same-center NOI decline of 2%-3%, we now expect NOI to drop 2.5% in fiscal 2017 (mid-point of guidance). Higher-than-expected tenant bankruptcies, rent concessions to boost occupancy, and lower rent from renewed leases all contributed to the revenue decline in the quarter. In fact, rents on renewed leases dropped a sharp 16.1% for the three months ended Sept. 30, 2017 (-7.9% year-to-date), and we expect continued pressure on rent growth over the near to intermediate term.

We based the stable outlook on our view that despite our expectations that same-store NOI will continue to decline over the next year as rent concessions help stem occupancy declines, debt leverage should remain in the high-7x area for the next one to two years. We think CBL's efforts to reposition and redevelop its portfolio of assets should help offset some of the pressure from declining rents.”

Competition:

CBL faces competition from changing consumer shopping habits. Specifically, online shopping and better located retail properties (more convenient and higher rents) will continue to pressure the stores to which CBL leases space, and ultimately CBL. As another form of completion, it can be argued there is simply an oversupply of class-B shopping malls, which will ultimately lead to more pressure on the industry, including CBL.

Management- (Capital Allocation):

CBL has been selling assets to free up capital, they reduced the dividend, and they’ve been paying down and modifying debt. For example, year-to-date, CBL has completed gross asset sales of $166.25 million including the sale of its remaining 25% interest in River Ridge Mall to its joint venture partner for $9.0 million. Also during the third quarter, CBL closed on the extension and modification of two unsecured term loans totaling $535 million and completed an offering of $225 million aggregate principal amount of its 5.950% Senior Notes Due 2026.

Catalyst-

A negative catalyst for CBL would be an economic slowdown, which would negatively impact CBL’s tenants, and accelerate CBL’s challenges. A positive catalyst would be the continued repositioning of CBL’s portfolio (i.e. continuing to dispose of undesirable properties, and adding more desirable locations).

Recent Price action:

CBL is NOT currently ranked in Jarvis. According to the Wall Street Journal, 25.5% of the shares outstanding were recently sold short.

Special /Unique:

CBL is not significantly different from other B-class mall owners. However, the company does maintain an investment grade credit rating, and it is working to reposition its portfolio towards more profitable assets.

The Last Downturn-

CBL’s share price still has not recovered to the level it achieved prior to the onset of the financial crisis in 2007, even after adjusting for dividends (the total return (dividend plus price appreciation) has been negative since the 2007 highs).

Quality-

CBL is a B-class mall owner and operator. The low rent/square foot (currently $32.83 base rent per square foot) is an indication of the less desirable property locations.

Insider Activity-

Capital Structure –

In addition to common shares, CBL has a variety of publicly traded debt and preferred shares outstanding. For example, the Series D preferred shares yield 8.1% and trade at $22.69, and the series E preferred shares yield 7.7% and trade at $21.60. Both the E- and D-series are currently redeemable at CBL’s discretion at $25 per share.

The following table shows CBL’s outstanding bonds. The bond prices decreased sharply following the November earnings release where the common share dividend cut was announced.

Risks –

The biggest risk for CBL is if more tenants continue to face financial hardships which would decrease property occupancy for CBL (due to bankruptcies) or decrease rents (due to CBL being forced to offer rent concessions to avoid bankruptcies). This scenario could occur as the industry continues to evolve towards more online sales (and less CBL “brick and mortar” properties), less B-class mall properties (like CBL’s), or simply if the economy turns downward. The challenges created by these negative environments could be magnified by CBL’s relatively high level of debt.

Conclusion:

It's tempting to buy shares of big-dividend REIT CBL & Associates (CBL), especially after its big price decline over the last month. It's also tempting to think the company can miraculously turn things around. Granted, the CBL is working hard to manage its shrinking cash flows, and transform its struggling shoppin mall portfolio into something more desirable in the marketplace, but the headwinds (from online shoppers and retailers with more attractive physical locations) leads us to believe CBL's equity shares are a value trap. However, it's bond may be worth considering: An Interesting Non-Equity Income Idea (CBL 2024 Bonds).

For reference, you can view all of our current holdings here.