As the market selloff intensifies, one strategy that helps many investors cope is dividend-growth investing. By owning stocks that pay steady growing dividends, it becomes psychologically easier for some investors to avoid the panicked selling that ends up hurting them so badly in the long term. Afterall, long-term compound growth is where the real money is made when it comes to investing. Nonetheless, steady growing dividends can help investors cope with high volatility (like right now), so we have included 10 top dividend-growth ideas below. They all pay growing dividends and trade at attractively discounted prices if you are a disciplined long-term investor.

“More people have lost money waiting for corrections and anticipating corrections than in the actual corrections." -Peter Lynch

“The big money is not in the buying or the selling, but in the waiting.” -Charlie Munger

50 Dividend-Growth Stocks, Down Big

Before getting into our top 10 countdown, let’s start with some data. The following three tables include top dividend-growth stocks, separated into blue chip stocks, REITs and BDCs. And as you can see, they all have a history of growing their dividend payments to investors each year.

Blue Chip Stocks: Let’s start with the blue chips stocks. These stocks were selected from the S&P 100 for having powerful dividend growth histories (at least 9 consecutive years of dividend growth). You can also see they have some impressive 10-year total returns (even though they are mostly down a lot this year). The 10-year “yield on cost” metric is also compelling (it’s calculated as the forward annual dividend payment per share divided by the share price 10 years ago, and it’s a metric that long-term investors may want to consider). The table is sorted by market cap.

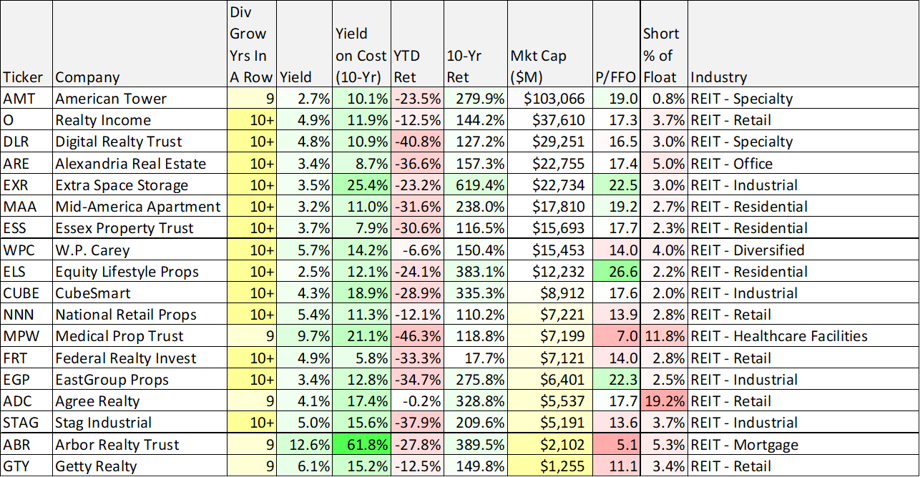

Real Estate Investment Trusts: REITs are also fertile ground for dividend growth opportunities. As you can see in this next table, the current dividend yields on REITs tend to be a little higher than the blue chips in our previous table, but the yields on cost are more similar. However, many of these REITs are down more this year, thereby creating some attractive long-term opportunities for income-focused investors (particularly those that like growing income). The short interest column is also interesting to consider.

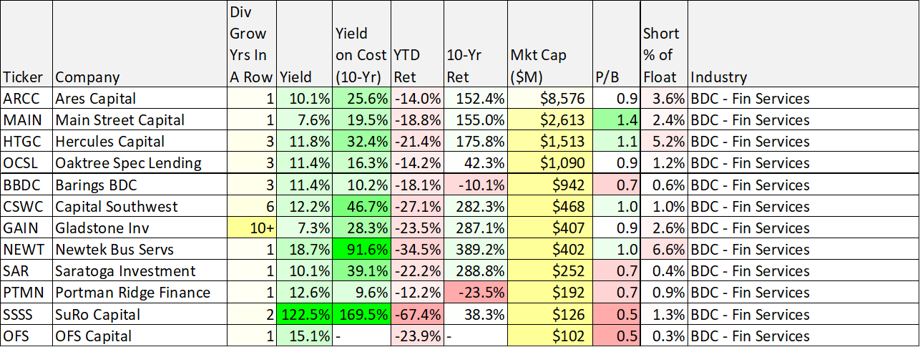

Business Development Companies: BDCs generally offer much bigger current dividend yields, and they can offer some very impressive 10-year “yield on cost” too. However, there aren’t too many BDCs that have been able to consistently raise their dividend payment each year, and the 10-year total return column is also worth considering.

So with that backdrop in mind, let’s get into the 10 top ideas. The list includes a variety of attractive blue chips stocks, three very compelling REITs and one big-dividend BDC that is particularly attractive now. Let’s get into it.

10. Intel (INTC), Yield: 5.5%

Intel is the leader in PC and server chips. And even though it has failed to match the growth rates of high-flyers like Nvidia and AMD in recent years, it still delivers very high margins and very health profits. Further, it will be helped by the recent Chips for America Act. It has paid a dividend for 28 years straight and it has increased its dividend for the last 7 years in a row. And considering this year’s steep share price selloff (shares are down 46% this year), the shares are currently downright attractive from a contrarian value investing standpoint. You can read our previous full report on Intel here (don’t be misled by the title).

9. Verizon (VZ), Yield: 6.7%

Verizon’s share price sits near its 52-week low, and its dividend yield (currently 6.5%) sits near a decade-long high. What’s more, its valuation is compelling if you can get comfortable with the near-term price risks. Overall, we view Verizon as an extremely attractive investment opportunity if you are an income-focused investor. We believe the shares will recover (following the recent strong declines) as the market acclimates to the new interest rate environment and as the valuation multiple adjusts back closer to less panicked levels. You can read more about Verizon is our recent detailed report here.

8. Apple (AAPL), Yield: 0.6%

A lot investors think of Apple as a growth stock, but we view it as an attractive value stock considering it trades at such low valuation multiples relative to its powerful earnings, cash flow generation and growth. Not to mention it has now raised its dividend payment for the last nine years in a row. Specifically, growing revenues at a double digit rate, with a 25% net profit margin, and trading below 25 times forward earnings (not to mention an attractive “yield on cost,” Apple is a Buy.

7. Realty Income (O), Yield: 4.9%

Realty Income (known as the monthly dividend company) has recently become very attractive as the shares have sold off hard and the dividend yield has mathematically rises. Specifically, Realty Income remains attractive for a variety of reasons, including its very strong financial position, its prudent acquisition-focused business strategy, its incredible dividend-growth (and safety) and its attractive current valuation. Not to mention, the outlook for its real estate business remains attractive because of the prime location properties that are largely not vulnerable to the online shopping trend that other types or REITs face (for example shopping malls). And despite the risk factors (such as rising rates and conservative rent escalators), we continue to believe Realty Income presents a very attractive investment opportunity for steady income-growth (and price appreciation) investors. You can read our previous full report on Realty Income here.

6. Hercules (HTGC), Yield: 11.8%

Somewhat of an odd ball on our list, Hercules is an internally-managed business development company that offers a double-digit yield and has now increased its dividend for 3 years in a row (a rarity in the BDC space).

Focused on providing financing for high-growth ventures, Hercules can get income investors access to market sectors they don’t normally invest in (prudent diversification can be a very good thing). Further, growth and venture have sold off this year (including Hercules) thereby making for a lower entry point to purchase shares. Further still, if rates keep rising—Hercules is in good shape (double good if the market recovers) because of its high exposure to floating rate investments and low fixed rate debt. Further, the valuation (price-to-book) has even come down (currently only a small premium to NAV).

Overall, we like the business, and if you are a long-term income-focused investor, we believe Hercules is absolutely worth considering for a spot in your prudently-diversified portfolio. You can read our full report on Hercules here.

The Top 5

Our top five dividend-growth stocks are reserved for members only, and can be accessed here. The top five includes two REITs and three more attractive blue chips stocks. We currently own four of the five in our top-performing 35-stock Income Equity Portfolio. If you are a long-term income-focused investor that likes the security of current income, combined with the potential for attractive price appreciation, you’ll likely find the list to be very compelling.

The Bottom Line

Even though share prices can fluctuate widely in the short-term, stocks represent ownership in businesses, and businesses are long-term investments. The recent volatility has made for increasingly attractive entry prices for long-term investors. And if the short-term price volatility stresses you out too much, stocks with steady growing dividends (such as the ones in this report) can help calm your nerves. We currently own most of the stock ideas in this report in our Income Equity Portfolio. In particular, we currently own four REITs, three BDCs and a variety of very attractive blue chip stocks. You can view all of our current holdings here.