While other business development companies (“BDCs”) were cutting their dividends as a result of the pandemic, Oaktree Specialty Lending Corp (OCSL) not only maintained theirs, but has also significantly increased it in each of the past five quarters. Moreover, the shares are trading at an attractive price relative to net asset value (“NAV”). In this report, we review the health of the business, the highly-experienced management team, its balance sheet, liquidity, dividend safety, valuation and risks. We conclude with our opinion on investing.

Overview

Oaktree Specialty Lending Corporation (OCSL) is an externally managed BDC focusing its investments primarily on US-based middle market companies through senior secured debt, asset backed loans, unsecured/mezzanine loans, bonds, and to a lesser extent in preferred and/or common equity—usually in conjunction with a concurrent debt investment. It also opportunistically invests in areas that have less competition and potential for greater investment returns, such as stressed sectors and rescue lending, sponsor-led acquisitions and management and/or leveraged buyouts.

Worth noting, Oaktree Capital Management merged OCSL with its sister BDC Oaktree Strategic Income Corporation (OCSI) in early 2021. The merger drives shareholder value by leveraging the benefits of larger scale, diversity and financial flexibility, while also streamlining management operations at Oaktree. OCSL has remained the operating entity after the merger. As a note, we previously owned OCSI, and now own OCSL following the merger.

Well Diversified, Senior Secured Debt Focused Portfolio

With the OCSI merger, OCSL is a more scaled BDC that has a portfolio worth $2.3 billion at fair value (including $504 million from the OCSI portfolio), up from $1.7 billion in the prior quarter. The portfolio consists of well diversified investments in 137 middle market companies operating in 41 industries, a large majority of which are non-cyclical and defensive, such as software, IT services and healthcare. It has also diversified its portfolio by investment size, as its top 25 investments account for just about 41% of its total portfolio, thus limiting the risk exposure to any specific individual investment.

Source: 3QFY21 Investor Presentation

As we can in the chart above, OCSL also has a noteworthy chunk of its investments in joint ventures. Specifically, OCSL co-invests in senior secured loans of middle-market companies and other corporate debt securities through joint ventures with Kemper Corp. and with GF Equity Funding (Glick JV), in which OCSL became a party as a result of the consummation of merger with OCSI. OCSL has 87.5% equity ownership in each of the two joint ventures, and as of March 31, 2021, the value of its investments in the Kemper JV and Glick JV were $130 million and $55 million, representing 5.6% and 2.3% of its portfolio, respectively. OCSL considers the joint ventures as income-enhancing vehicles that add to its earnings power.

Source: 3QFY21 Investor Presentation

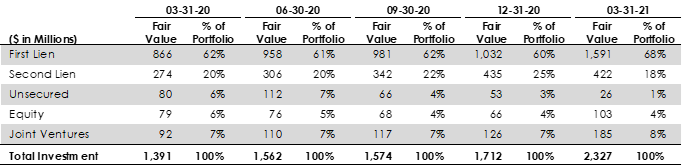

Further, OCSL has ~86% of its investments in senior secured loans, consisting of 68% in first lien loans and 18% in second lien loans. While investing in middle market companies typically carries some default risk, having a substantial portion of the investments in senior secured loans, and more specifically in first lien loans, adds a higher level of safety as the probability of incurring a loss on these loans is generally very low. In fact, the percentage of OCSL’s investments in first lien loans, which hovered around the 60%-62% range until the first quarter of fiscal 2021, shot up during 2QFY21 with the acquisition of OCSI, which had a higher focus on first lien loans.

Source: OCSL Presentations

Also noteworthy, the OCSL’s new investment commitments over the past few quarters have increasingly been in first lien loans. In fact, the first lien loans have accounted for about 74% of all of its new investment commitments in the past one year, including ~80% of the $318 million new investment commitments during 2QFY21.

New Investment Commitments

Source: OCSL Presentations

Strong External Manager and Seasoned Investment Team Driving Portfolio Performance

OCSL and OCSI were originally part of Fifth Street Asset Management (were called Fifth Street Finance Corp. and Fifth Street Senior Floating Rate Corp., respectively), until Oaktree assumed their management in late 2017. Founded in 1995 by the legendary investor Howard Marks, Oaktree is a leading global investment management firm that is focused on credit investments. As of 30 June 2021, it managed $156 billion in contrarian, value-oriented, risk-controlled investment strategies across a variety of asset classes. OCSL’s management team consists of experienced executives from Oaktree, also including Armen Panossian, who serves as its CEO and CIO. The team is supported by a dedicated strategic credit team of 28 investment professionals, consisting of 14 senior level professionals (6 Managing Directors, 4 Senior Vice Presidents and 4 Vice Presidents) with average investment experience of 15 years.

The investment portfolio of OCSL (as well as OCSI, pre-merger) has undergone a major revamp since Oaktree assumed management in 2017. Oaktree shifted OCSL’s investment focus from smaller private borrowers to larger borrowers (as seen in the change in median debt portfolio company EBITDA from $50 million in 2017 to $103 million in 2QFY21 in the table below), and has been repositioning the portfolio to more liquid, higher quality and defensive investment bets (termed as core investments). This has resulted in improved portfolio performance and an excellent credit profile with investment grade credit ratings and no non-accruals in the debt portfolio as of 31 March 2021.

Source: 3QFY21 Investor Presentation

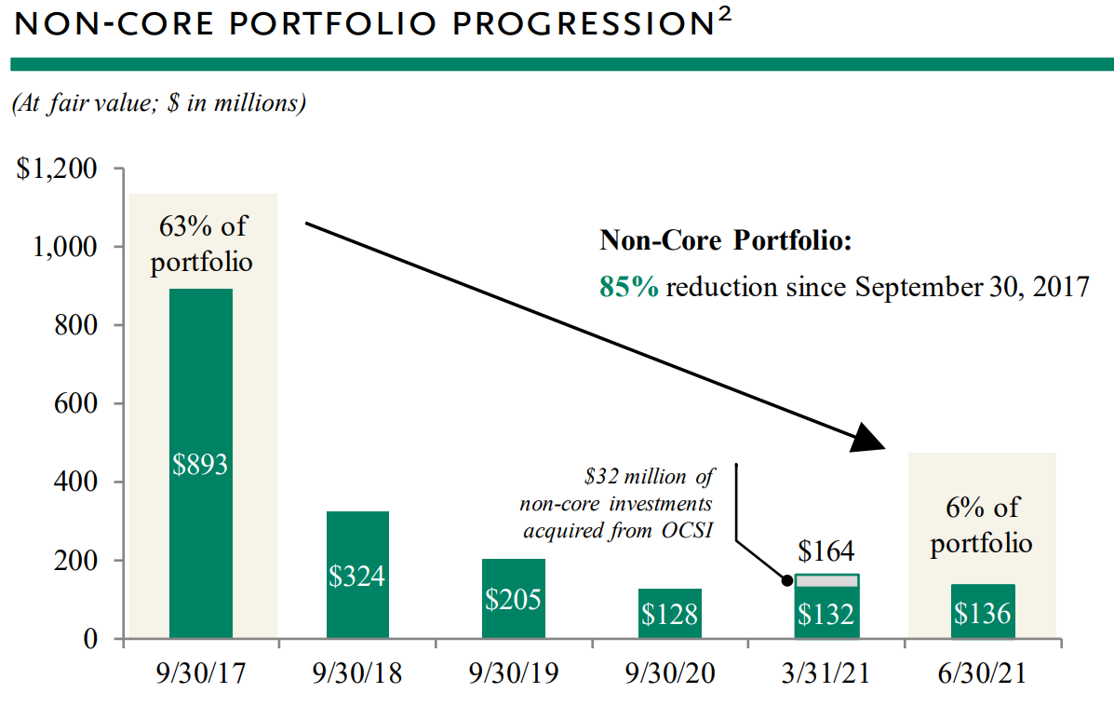

We note that the defensive repositioning of OCSL’s portfolio is mostly complete, and the noncore investments represent only about $132 million (including $32 million from OCSI), or 6% of OCSL’s portfolio at fair value, consisting of $77 million of debt investments in 4 companies, $51 million of equity investments in 16 companies and limited partnership interests in one third-party managed fund, and $8 million in one aircraft.

Source: 3QFY21 Investor Presentation

As a result of the strategy shift, OCSL has been able to deliver compelling performance, generating an annualized return on equity (ROE) of 12.0% since 2018. The BDC has seen consistent growth in its net asset value (NAV) after the COVID induced dip during the first quarter of 2020. In fact, its most recently reported NAV of $7.22 per share is the highest under Oaktree’s management and is supported by consistent growth in net investment income, and the appreciation in the value of its portfolio resulting from the repositioning into higher quality investments.

source: Q3 investor presentation

Worth noting, Brookfield Asset Management (BAM) has a majority stake in Oaktree, and the two asset managers together have one of the largest and most comprehensive alternative investment platforms with over $600 billion in AUM. OCSL immensely benefits from this large platform as it gets access to extensive resources, management expertise and industry relationships for sourcing, due diligence and credit selection, while also getting frequent first looks at quality investment opportunities.

Conservative Balance Sheet, Strong Liquidity

OCSL maintains a conservative balance sheet that is levered just about 0.79x on a net debt to equity basis, as on 30 June 2021, which is just below its target leverage range of 0.85 to 1.0x.

OCSL’s liquidity position remained strong with $85 million of cash and $636 million of undrawn capacity on its credit facilities at the end of 3QFY21, which was sufficient to fund its unfunded commitments of $239 million, including $166 million eligible to be drawn immediately (the remaining amount is subject to certain milestones that must be met by portfolio companies).

Source: 3QFY21 Investor Presentation

Growing Dividend, Well Covered by NII

OCSL maintained a steady dividend payment even at the peak of the pandemic, when many other BDCs reduced their dividend to preserve liquidity; and from September 2020 onwards, it has increased its dividend every quarter. It declared a dividend of $0.13 per share for the June quarter, which represents ~37% growth over the dividend paid in the previous June quarter. While the dividend growth has been impressive, what is more impressive is the fact that it has remained well covered by net investment income (NII), as we can see from the chart below.

data source: OSCL

Going forward, we believe OCSL is well positioned to not only maintain, but also further grow the dividend. We expect the dividend growth to be well supported by NII, which will benefit from a number of factors, including:

Rotation of the portfolio into higher yielding investments: OCSL has a continued focus on improving the yield on its investments by rotating out of lower-yielding investments and into higher-yielding proprietary loans. During 3QFY21, it exited $39 million of lower yielding investments, and at the quarter end it had just about $142 million (including $102 million acquired from OCSI) of lower priced investments (priced at or below LIBOR+4.5%) remaining in the portfolio. We believe OCSL can easily swap these investments into higher yielding ones to increase its income. Further, most of its new investment commitments have higher yields (the $178 million new investment commitments during 3QFY21 were at an average yield of 9.2%), implying there is continued upside to the NII to be realized over time.

Synergies from OCSI merger: The merger with OCSI will bring operational synergies resulting from the elimination of duplicative expenses that will lead to near-term G&A savings, in addition to interest expense savings from a more streamlined capital structure. Also, in conjunction with the merger, Oaktree has agreed to waive off base management fees totaling $6 million, which will result in an additional accretion of $0.75 million per quarter to NII for the next two years.

Accretion from joint ventures: ~$79 million of investments in the Kemper and Glick JVs are lower priced investments (at or below LIBOR+375). OCSL can increase the underlying portfolio yields of these JVs by rotating them into higher spread investments. Additionally, given the Kemper JV’s strong earnings power, OCSL is now receiving dividend income from the JV starting last quarter, which will further add to its investment income.

Targeted increase in leverage: As mentioned, OCSL is operating just below the low end of its long-term targeted leverage of 0.85x to 1.0x, presenting it the opportunity to deploy higher leverage to make incremental investments and enhance its returns. Near term though, the BDC expects the leverage levels to remain at the low end of the target range.

“I would expect, given our tone of cautious optimism, we'll be probably closer to the low end of our target range, barring any sort of surprises to the upside in terms of non-sponsor deal flow that we may be able to find that we think has mispriced risk. So we're always looking for those types of idiosyncratic opportunities. They could present themselves even when the markets are pretty strong and some of the harder to understand or harder to underwrite businesses. We do still see a lot of deal flow in our life sciences area and some of the other areas that are outside of the LBO sponsor activity area. So if we did see some surprises to the upside on our origination on the non-sponsor side, I could see us trending towards the middle part of our range. I don't think that we'll be on the high end of our range in the next couple of months.” - Armen Panossian, CEO & CIO on 2QFY21 earnings call

Valuation

Like most BDCs, OCSL shares have seen a strong rebound since the pandemic induced lows in March 2020. Its price has appreciated by over 60% in the past one year and this year so far it has returned ~37% to shareholders in the form of dividends and price appreciation. Despite the significant price appreciation, the stock continues to trades at NAV, unlike some of the other top BDCs that are commanding a significant premium to their NAVs, as we can see from the following table.

source: StockRover, data as of 10/13/21

We believe that the quality of OCSL’s portfolio is as good as some of the other top BDC’s and believe it has the potential to outperform some of the top BDCs in the longer-term, especially given its larger scale now with the merger with OCSI, and the access it has to the extensive resources and management expertise of Oaktree and Brookfield. Accordingly, we believe that by investing in the shares at current prices, investors can grow their capital, in addition to pocketing an attractive 8.0% dividend yield. Moreover, OCSL has been growing its dividend over the past five quarters and investors tend to pay more for a BDC with a rising dividend, thus making the case for price appreciation even stronger. Furthermore, based on the NII dividend coverage ratio, we expect additional dividend increases in the quarters ahead.

Risks

Investment Underwriting Risks: Similar to other BDCs, OCSL primarily invests in privately held middle-market companies which generally tend to carry higher risks. It also tends to opportunistically invest in distressed assets. While OCSL’s manager Oaktree has strong credentials as one of the best evaluators of distressed assets, any poor underwriting on its part can possibly lead to investment losses.

Conflicts of Interest with Manager: Being externally managed, OCSL is inherently exposed to conflicts of interest with its manager, which will have certain obligations towards its own stakeholders that might not be in the best interests of OCSL’s shareholders.

Interest Rate Risk: OCSL generates most of its interest income based on floating rates, implying that its investment yields are tied to market interest rates such as LIBOR. While the majority of its liabilities are also on floating rates, it does have a $300 million unsecured debt maturing in 2025 that has fixed interest rate and has recently priced at $350 million debt at fixed interest rate. This means that in a declining interest rate scenario, the decline in investment yields will not be offset by a commensurate decline in interest costs, and this can negatively impact its NII.

Conclusion

OCSL is a well-managed BDC that has a solid, diverse portfolio which generates strong returns across market cycles. It maintains a conservative balance sheet with limited leverage, no near-term debt maturities, solid liquidity and investment grade credit rating, which allows it to raise funds at low costs and offers ample flexibility to maintain its liquidity to fund its investment commitments, as well as to support continued growth in investments. Moreover, it has access to extensive resources and management expertise of global asset managers Oaktree and Brookfield. Accordingly, we believe it has the potential to outperform some of the top BDCs in the longer-term. With growing dividends, an attractive 8.0% dividend yield and the shares trading at NAV, we believe OCSL is an attractive investment within the BDC space for longer-term income focused investors.

We are currently long shares of OCSL. And if you are looking for additional attractive high-income investment opportunities, consider other top ideas (that we currently own) in our latest members-only “Top 8” report below.