REITs, BDCs, CEFs and MLPs may seem like dramatically different types of investments (and they are), but if you are an income-focused investor, it can make sense to consider all of them for a spot in your prudently-diversified portfolio. In this report, we share data on 25+ big-dividend investment opportunities from each category, and then dive deeper into four specific attractive opportunities (including one REIT, one BDC, one CEF and one MLP). We then conclude with a few important takeaways for income-focused investors to keep in mind.

25+ Big-Dividend REITs

Real Estate Investments Trusts, or REITs, are often an income-investor favorite because they can pay big steady dividends and because they give many investors a sense of long-term stability that helps them sleep well at night. REITs are also a lot easier to invest in than going out and buying actual real estate properties on your own (plus they’re a lot more liquid too).

To give you a sense of recent performance and dividend yields, the following table contains 25+ big-dividend REITs (sorted by industry).

You may notice a few of your favorite REITs on the list above. And you’ll also notice that year-to-date REIT performance has been a mixed bad (especially by industry) and businesses continue to recover and adjust to the pandemic. We’ll dive into the details of one particularly attractive REIT from the list, later in this report.

25+ Big-Dividend BDCs

Business Development Companies, or BDCs, basically provide financing (usually loans) to middle-market-sized companies. These are often the types of companies that are too small or too risky for traditional big banks to deal with (especially as big bank regulations have become increasingly stringent in recent market cycles). However, by bringing unique skill sets, and by constructing a diversified portfolio of investments, BDCs can reduce a lot of the risks and thereby provide select compelling big-dividend investment opportunities.

To give you a sense of recent performance and dividend yields, the following table contains 25+ big-dividend BDCs (sorted alphabetically).

You may notice a few of your favorite BDCs on this list. And you’ll also notice that year-to-date performance has been particularly strong for most BDCs as compared to the S&P 500. The above table also provides a variety of additional metrics (including price-to-book ranges and market caps), and we’ll dive deeper into one particularly attractive BDC from the list, later in this report.

25+ Big-Dividend CEFs

Closed-End Funds, or CEFs, are another income-investor favorite because they can also offer very high yields and highly interesting price premiums and discounts versus the value of their underlying holdings (i.e. net asset value, “NAV”). Like mutual funds and exchange traded funds (“ETFs”), CEFs are pooled vehicles that hold many underlying investments (such as stocks and/or bonds, depending on the particular CEF strategy). However, unlike mutual funds and ETFs, there is no immediate mechanism in place to ensure CEF market price stay close to their NAVs, and as such—CEFs can trade at wide premiums and discounts (thereby creating unique risks and opportunities).

To give you a sense of dividend yields and recent performance, the following table contains 25+ big-dividend CEFs (sorted by strategy).

There are likely a handful of investor favorites on this list that you have hear of (or may even already be invested in). We’ll dive deeper into one CEF from this list that is particularly attractive, later in this report.

25+ Big-Distribution MLPs

Master Limited Partnerships, or MLPs, provide another vehicle through which investors can capture high yields. However, MLPs offer their own unique sets of risks and benefits.

For starters, MLPs are basically publicly traded limited partnerships, that offer the tax benefits of of a private partnership, but also the liquidity benefits of a publicly traded company. And MLPs are effectively limited to the natural resources (and real estate) sectors.

However, investors should also keep in mind that MLPs generally come with the additional burden of annual K-1 tax filings, and they can create tax liabilities when held within supposedly tax deferred retirement accounts.

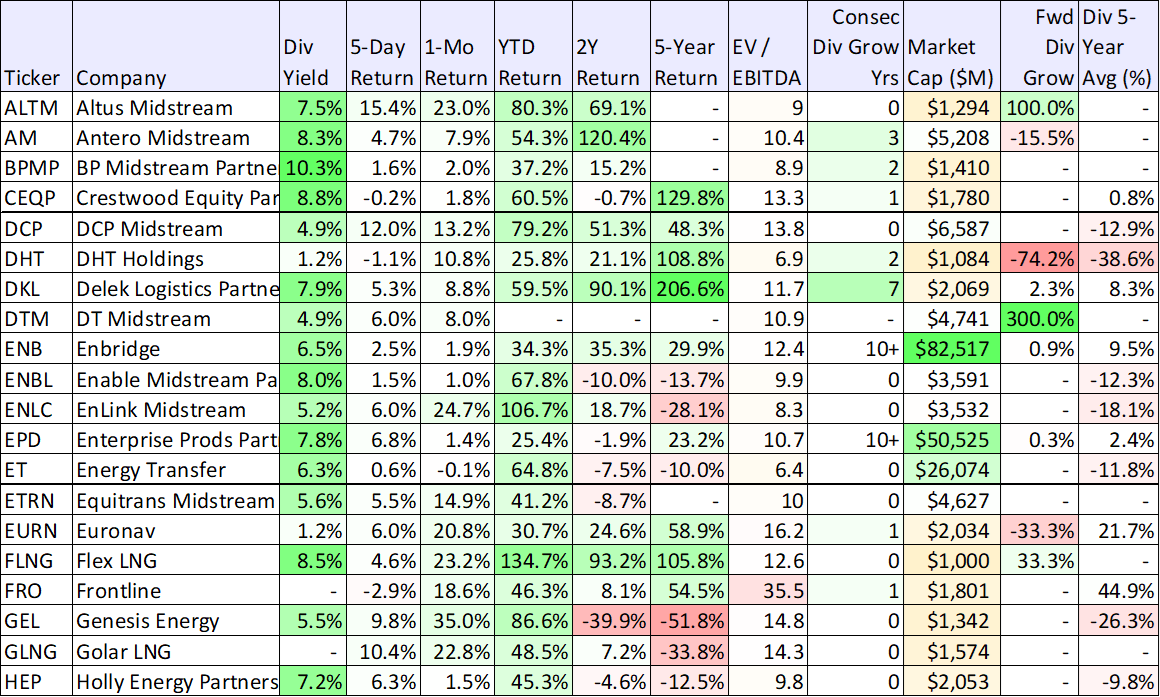

To give you a sense of recent performance and yields, the following table contains 25+ big-distribution MLPs, sorted alphabetically. You will also notice that the table includes several midstream companies that technically are not MLPs, but still offer large yields that are worth considering. Midstream activities include the processing, storing, transporting and marketing of oil, natural gas, and natural gas liquids.

Many popular MLPs are included in the above list, and the table also includes data on valuation and dividend history. We’ll highlight one particularly attractive MLP from the above list, later in this report.

4 Big-Dividends Worth Considering:

With that data backdrop in mind, here are four particularly attractive big-dividend opportunities from the list that are worth considering if you are a disciplined, long-term, income-focused investor.

Arbor Realty Trust (ABR), Yield: 7.4%

Arbor Realty Trust (ABR) is an attractive mortgage REIT, offering a 7.4% yield, a growing dividend and a compelling price. Specifically, ABR is a nationwide REIT and direct lender that provides loan origination and servicing for multifamily, seniors housing, healthcare and other diverse commercial real estate assets. And as you can see in our earlier table, it continued raising its dividend throughout the pandemic (while others were cutting) and the dividend continues to be well covered. We recently wrote up a very detailed report on ABR for our members back on September 7th, and the bottom line takeaway was (and still is) this:

Mortgage REITs can be an attractive source of steady high income, but they come with risks. As we saw during the depths of the 2020 covid sell off, years of gains can be wiped out quickly as dividends were slashed and share prices plummeted. ABR faired much better than peers because of the relatively conservative and diversified nature of its balance sheet and its business. In particular, ABR was able to continue increasing its dividend when others were cutting, and ABR’s share price continues to be a long-term top performer. In our view, ABR is well positioned for share price strength and dividend growth in the years ahead, and if you don’t own shares they are worth considering—particularly if you are an income-focused investor.

Oaktree Specialty Lending (OCSL), Yield 8.1%

Oaktree Specialty Lending (OCSL) is an attractive 8.1% yield BDC that was included in our earlier BDC list, and we like it for a variety of reasons. For starters, Oaktree was founded by legendary investor Howard Marks, known for his patient, deep-value approach to investing. And that is exactly what these funds do, considering they keep the balance sheet relatively conservative until market conditions start presenting attractive “deep value” opportunities like they did during the pandemic. OCSL (and OCSI, which was recently rolled up into OCSL) stayed conservative and then got aggressive when markets sold off during the pandemic. The rewards of this strategy were great, and it is an attractive, disciplined long-term strategy that can be repeated. In fact, Oaktree was one of the few BDC that was able to increase its dividend consistently during the pandemic while it share price and balance sheet both continued to improve. We wrote this one up in great detail for our members back on June 30th, and here is how we concluded that report:

OCSL is a well-managed BDC that has a solid, diverse portfolio which generates strong returns across market cycles. It maintains a conservative balance sheet with limited leverage, no near-term debt maturities, solid liquidity and investment grade credit rating, which allows it to raise funds at low costs and offers ample flexibility to maintain its liquidity to fund its investment commitments, as well as to support continued growth in investments. Moreover, it has access to extensive resources and management expertise of global asset managers Oaktree and Brookfield. Accordingly, we believe it has the potential to outperform some of the top BDCs in the longer-term. With growing dividends, an attractive 7.73% dividend yield and the shares trading at meaningful discount to NAV, we think OCSL is an attractive investment bet within the BDC space for longer-term income focused investors. We are currently long shares of OCSL.

Oaktree currently trades at a price-to-book value of around 1.0x, which believe remains attractive and the shares are worth considering if you are disciplined, long-term, income-focused investor.

PIMCO Dynamic Income (PDI), Yield: 9.8%

PIMCO Dynamic Income (PDI) is a very attractive 9.8% yield CEF that invests in a variety of income-producing bonds. The strategy’s primary objective is high income (which it has consistently delivered) and its secondary objective is price appreciation (which it has steadily maintained). We recently wrote in great detail about the upcoming merger of PDI with two other PIMCO Funds (PCI) and (PKO). And considering PDI continues to trade close to NAV (rare for a PIMCO fund—they usually trade at big premiums) we believe the shares are attractive. There could be some near-term bumpiness to the share price as a dividend adjustment might be part of the upcoming merger, but the underlying investments and the fund remain very attractive. Here is how we concluded our recent full report on PDI:

We know what PDI is worth because we can see the NAV every day. However, investors are rightfully concerned about the outcome of the merger (will there be a big distribution cut?), as well as concerned about the high payout ratio, high leverage and discounted price versus par for the underlying holdings. As a result, the once big premium versus NAV has fallen significantly. However, this is still PIMCO (essentially the best large fixed income investor in the world), and the upcoming merger gives them a chance to correct the growing stresses and risks (created by the high leverage and high payout ratio versus the underlying holdings). And once the dust settles, the underlying holdings will keep paying high income, PIMCO will still be a great manager, and eventually—the once big premium versus NAV for PDI—will be back!

Overall, if you are a long-term, income-focused investor, PDI is worth considering for investment.

Energy Transfer (ET), Yield: 6.3%

Energy Transfer (ET) is an attractive 6.3% yield MLP that owns and operates a diversified portfolio of midstream energy assets (including crude oil, natural gas and natural gas liquids (NGL) pipeline services and storage, for example). Energy Transfer has been working diligently (and successfully) to deleverage its balance sheet, and we expect that distribution increases will resume in the relatively near future. Yet despite the improving conditions, this one still trades at only 6.4x EV/EBITA, as the market continues to look backwards instead of forward. We wrote this one up in great detail for our members a couple months back, and we concluded it like this:

If you are looking for an attractive distribution yield, Energy Transfer is worth considering. As the company deleverages its balance sheet, distribution increases will likely follow. Further, the current valuation is low and suggests there is more price appreciation potential ahead—especially considering the improving fundamentals of the business.

Further, if you are into income-generating options trades, Energy Transfer is often a good one for selling out-of-the-money, income-generating, put options (we shared one such trade on ET with our members a little over a month ago) because the share price is low (thereby requiring less cash to secure the trade), volatility is often higher (which increases the premium income available), and it’s a great company to own for the long-term (if the shares/units get put to you).

Conclusion:

If you are an income-focused investor, it can make sense to consider opportunities from a variety of categories, such as those we reviewed in this report. Not only will this help diversify away some of your risks, but it can also help you keep you investment income high. Moreover, the four specific opportunities we have highlighted in this report are particularly attractive, in our view. Because when markets get volatile, it can be highly reassuring to have those big steady long-term dividend payments flowing into your account.

For reference, we currently own BDC OCSL and CEF PCI (which will roll into PDI soon), and the other names in this report are included high on our current watchlist. Furthermore, if you are looking for additional attractive opportunities from these four categories, consider our newly-released members-only report: Top 8 Big-Dividend REITs, BDCs, CEFs and MLPs. We currently own 7 of the 8 names on this list within our prudently-diversified, 38-stock, Income Equity Portfolio. All of the holdings in this portfolio are available to members, and we are currently offering a 10% Off discount for all new members.

However, at the end of the day, it is critically important for investors to stay focused on their investment goals, and stick to strategies that meet their own personal needs. Disciplined, goal-focused, long-term investing is a winning strategy.