WP Carey recently announced quarterly earnings, whereby it beat expectations. However, the share price is down this year (despite gains for other top dividend REITs), thereby leaving investors wondering what is happening and if the shares are worth investing. In this report, we review the company and its strategy, and then review 10 good things about WPC, 5 big risks to consider, and finally share our one bottom line conclusion about investing,

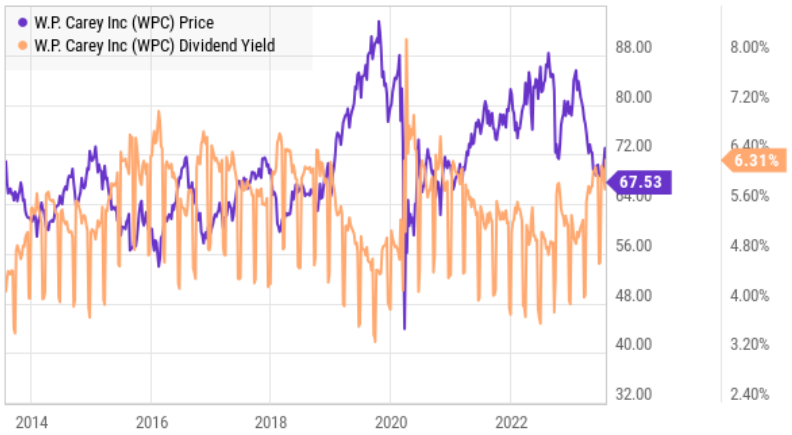

Overview: W.P. Carey (WPC), Yield 6.3%

W. P. Carey (WPC) is a REIT that specializes in investing in single-tenant net lease commercial real estate, primarily in the U.S. and Northern and Western Europe.

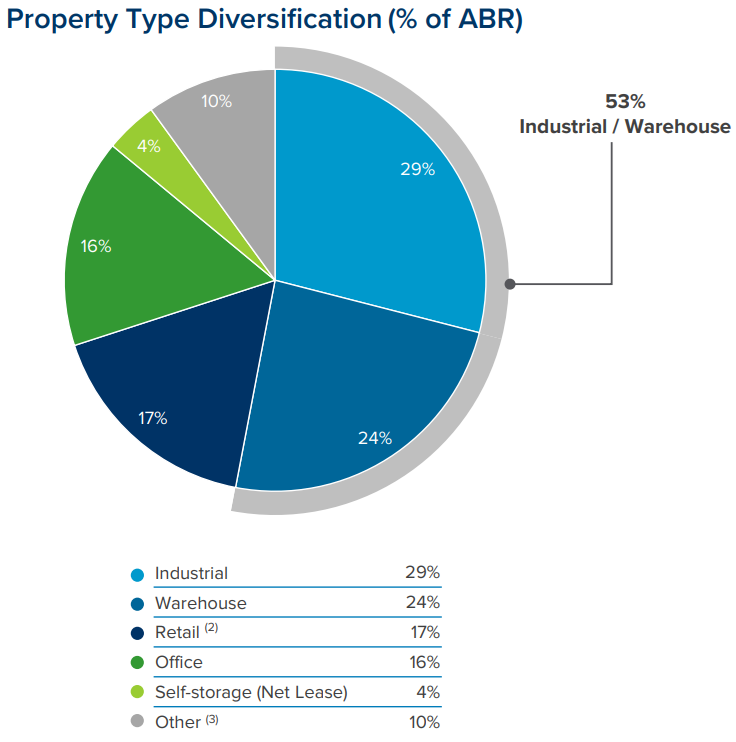

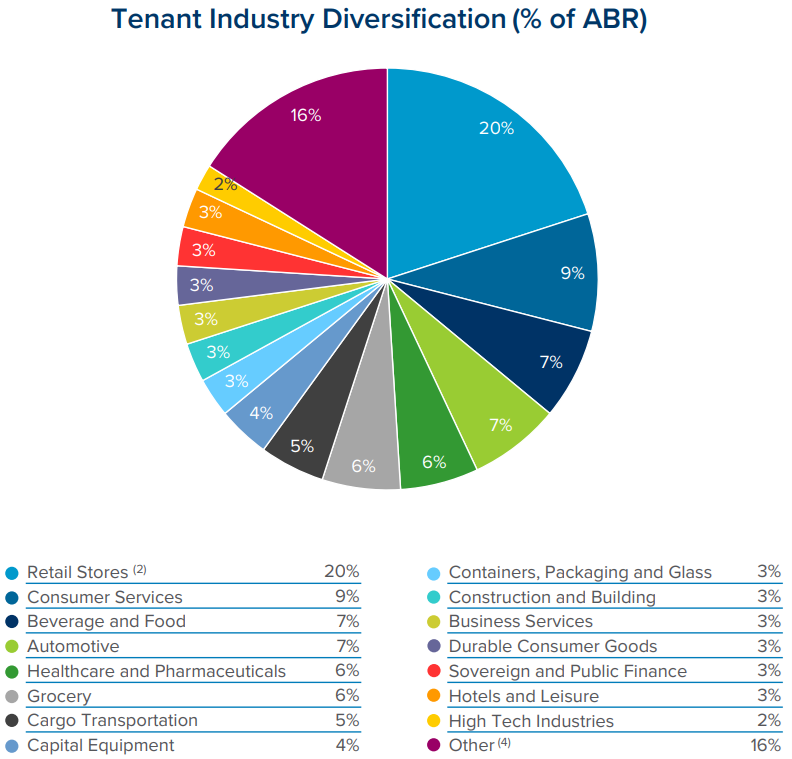

It is one of the largest owners of net lease real estate and among the top 20 REITs in the MSCI US REIT Index. WPC’s portfolio is highly diversified by geography, tenant, property type and tenant industry. And the company has a successful track record of investing and operating through multiple economic cycles since 1973—led by an experienced management team. WPC also has an investment grade balance sheet (with access to multiple forms of capita), as well as stable cash flows (derived from long-term leases that contain strong contractual rent bumps).

Investment Strategy:

The WPC investment strategy is to generate attractive risk-adjusted returns by investing in net lease commercial real estate, primarily in the U.S. and Northern and Western Europe. The company aims to protect against downside by combining credit and real estate underwriting with sophisticated structuring and direct origination.

WPC also works to acquire “mission-critical” assets essential to a tenant’s operations. And to create upside through rent escalations, credit improvements and real estate appreciation. WPC also works to capitalize on existing tenant relationships through accretive expansions, renovations and follow-on deals

The REIT believes the hallmarks of its investment approach include diversification by tenant, industry, property type and geography. As well as disciplined, opportunistic, proactive asset management and a conservative capital structure.

Q2 Earnings:

WPC recently announced second quarter earnings, whereby the company delivered AFFO (Adjusted Funds from Operations) of $1.36 (beating expectations by $0.07) and delivered revenue of $452.6M (beating estimates by $22.12M). Here is what CEO Jason Fox had to say:

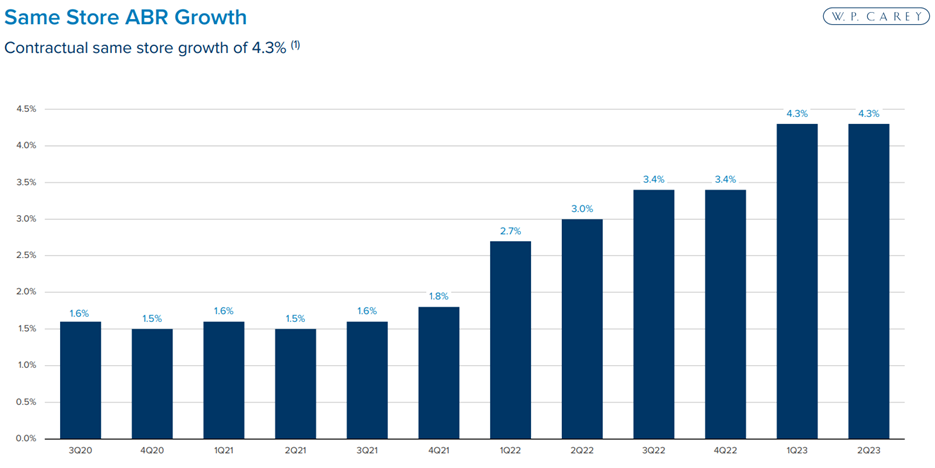

“Our performance over the first half of the year continued to be driven by the strength of our investment activity — completing close to $1 billion of investments — and contractual same-store rent growth that remained over 4%.” And “we expect further deal momentum over the second half of the year, given the competitiveness of sale-leasebacks as an alternative source of financing and the investment spreads we’re achieving. We're also confident in our ability to fund our investments and other capital needs without having to raise additional capital this year, something we view as a distinct competitive advantage in the current environment. Furthermore, we expect rent growth to remain elevated, reflecting the lagged impact of CPI on rents, as well as higher fixed increases.”

10 Things We Like About WP Carey:

1. Diverse Investment Portfolio: W.P. Carey's investment portfolio spans various sectors, providing diversification and risk mitigation. The company has been successful in capitalizing on opportunities in North America and Europe, finding attractive deals in warehouse and industrial sale leasebacks, among others. The ability to source captive deal flow from existing tenants and private equity sponsors adds further strength to WPC's investment strategy.

2. Solid Fundamentals and Rental Growth: W.P. Carey's recent investment activity has been fruitful, with a significant volume of accretive new investments during the second quarter. The company's contractual same-store rent growth remains robust, making it a standout performer in the net lease sector. The favorable environment for sale leasebacks enables WPC to apply upward pressure on capitalization rates, further enhancing the potential for value creation.

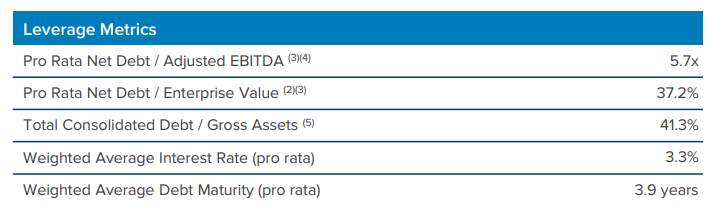

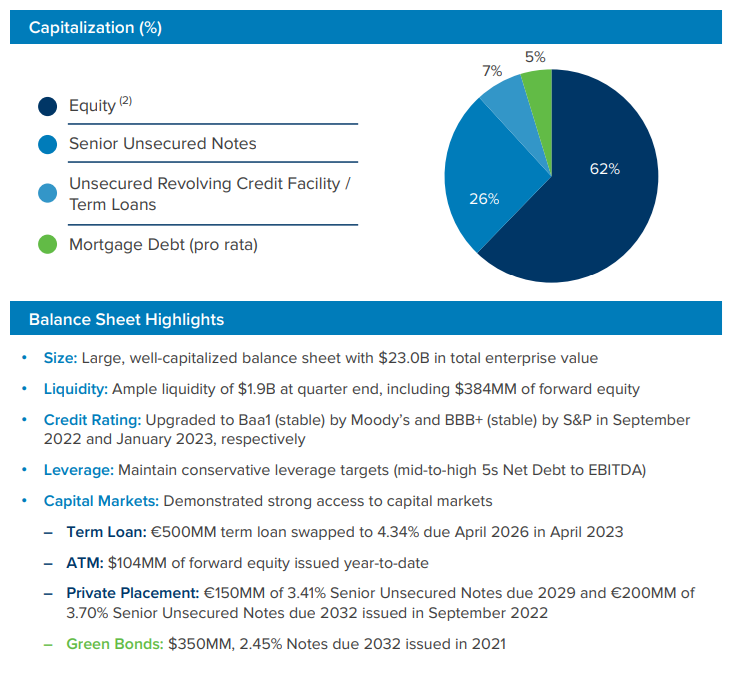

3. Capital Positioning and Flexibility: W.P. Carey's strong balance sheet positions the company well to manage its near-term debt maturities effectively. The company's prudent capital raising strategies and diverse sources of capital provide a competitive advantage in uncertain market conditions. With the ability to raise capital from various sources, including unused capacity on the revolving credit facility, unsettled equity forwards, and anticipated disposition proceeds, WPC can fund its investments without the need to raise additional capital in the near term.

4. Stable Sale-Leaseback Market: The sale-leaseback market has remained stable throughout the year, particularly in the U.S. This stability indicates a healthy market for W.P. Carey's core business model, providing sale-leaseback financing solutions for operators.

5. Larger Transactions: W.P. Carey has seen larger transactions this year, indicating growth in deal sizes, with some deals ranging around $75 million. This expansion suggests the company's ability to handle bigger transactions and potentially drive higher revenue.

6. Competition Thinning: The competition has thinned out for W.P. Carey, particularly among private equity real estate peers, due to increased costs and reduced availability of mortgage financing. This favorable competitive landscape may provide more opportunities for W.P. Carey to secure attractive deals.

7. Decreased Office Exposure: The company has been strategically reducing its exposure to the office sector, decreasing it significantly from over 30% to about 16% of its total portfolio. This shift reflects W.P. Carey's focus on other asset classes like industrial warehouses, which are currently more attractive.

8. Positive Rent Bumps: The company has experienced positive rent bumps, with contractual same-store increases at 4.3% in the first two quarters of the year. This growth trend is expected to continue into the future, with projected rent bumps at around 4% for the back half of the year and an average of 3% for 2024. Positive rent bumps contribute to the company's revenue growth and overall financial performance.

9. The Dividend: W.P. Carey has a robust history of dividend growth, having increased its dividend payout for 12 years in a row. This consistent track record of dividend growth reflects the company's stability and commitment to rewarding shareholders. For income-focused investors, a reliable and growing dividend stream is a crucial factor when evaluating potential investments. And WPC just raised its quarterly cash dividend to $1.069 per share, equivalent to an annualized dividend rate of $4.276 per share. This suggests that W.P. Carey is committed to returning value to its shareholders through dividends.

10. Valuation: The current P/FFO valuation ratio of 12.8 times is notably low compared to historical standards. This suggests that the stock may be undervalued (but also faces risks, as discussed in the next section), thereby presenting an opportunity for investors to acquire shares at a favorable price. An undervalued stock with a strong dividend yield can provide an attractive combination of income and potential for capital appreciation.

(note: data as of Thursday, July 27th)

5 Risks Investors Should Consider:

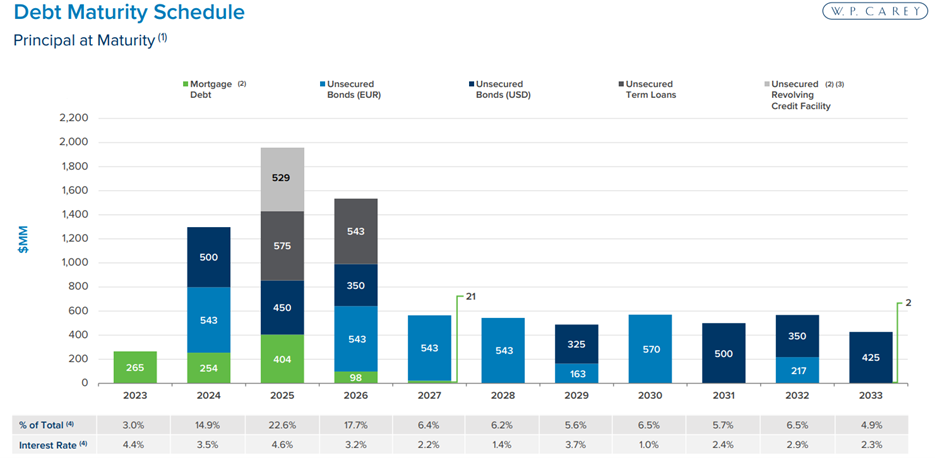

1. Interest Rate Volatility: Fluctuations in interest rates can impact the cost of borrowing for W.P. Carey, potentially affecting the profitability of its investments and financial performance (and its own valuation). For perspective, here is a look at the company’s upcoming debt maturity schedule (below). This matters because as interest rates have recently risen sharply (and remain dynamic) refinancing maturing debt will likely come at higher rates.

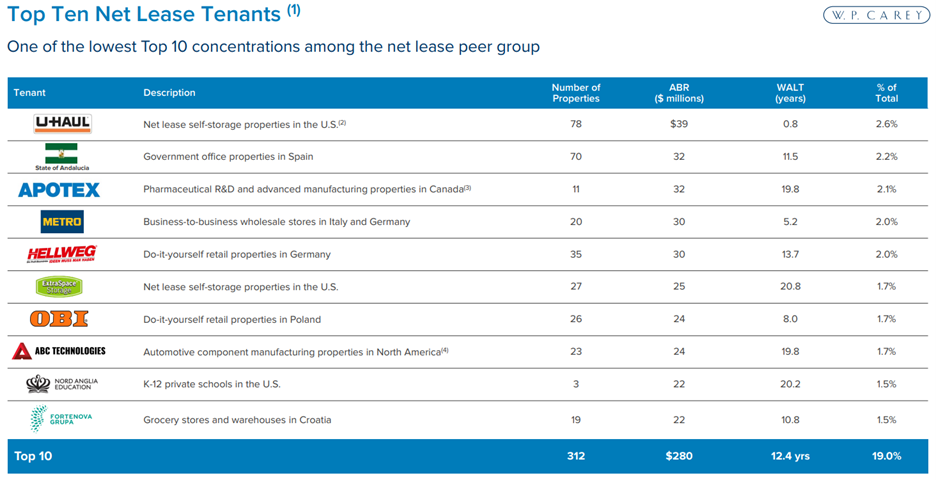

2. Tenant Credit Risk: W.P. Carey's revenue depends on the creditworthiness of its tenants. If major tenants face financial difficulties or default on lease payments, it could impact the company's cash flow and operations. Fortunately, as mentioned early (and as described in the graphic below), WPC is well diversified and has a relatively low tenant concentration. Nonetheless, the company’s reliance of major tenants, such as Apotex and ABC Technologies, could lead to significant revenue exposure if any of these tenants face financial difficulties or fail to meet their lease obligations.

3. Economic Downturn: A broader economic downturn or recession could lead to higher vacancies and reduced rental income as tenants may struggle to meet their lease obligations. And this scenario could potentially be exacerbated by higher interest rates, as described earlier.

4. Office Portfolio Exposure: While W.P. Carey has been reducing its exposure to office properties, a significant portion of its portfolio (~16%) remains invested in this sector. Demand for office space may be influenced by economic conditions, remote work trends, and changing business needs. In particular, office property performance has continued to deteriorate dramatically in recent years following the pandemic and increased work-from-home.

5. Market Conditions and Competition: W.P. Carey faces competition from other real estate investment firms in the sale-leaseback market. Increased competition may make it challenging to find attractive deals or lead to higher acquisition costs. For example, the net lease transaction market has experienced slowdowns over the past year, making it challenging to find attractive investment opportunities. If the market continues to slow down or experiences unfavorable conditions, it may impact W.P. Carey's ability to deploy capital and acquire new properties. Further still, real estate valuations can be subject to fluctuations due to changes in demand, economic conditions, and other factors. A downturn in the real estate market could adversely affect the value of W.P. Carey's properties, leading to potential losses or reduced income.

The Bottom Line:

Overall, we believe WPC’s growth has slowed (as evidenced by the slowing growth rate of its dividend increases), but it is still growing (thanks in large part to rent escalators), and it is well positioned to benefit going forward (considering its relatively strong financial position and very solid real estate portfolio). In fact, we believe the shares are attractively priced, despite the risks, because the market will recover (knock on wood) and WPC is in a better position than peers to benefit.

We do not currently own shares of WPC (we have owned it in the past), but it is high on our watchlist, especially as the share price is down this year and the current valuation is near the lower end of the historical range. If you are looking for a big-and-growing dividend, with the potential for share price appreciation, W.P. Carey is absolutely worth considering for a spot in your income-focused value portfolio.