If you care most about receiving big steady dividends and income from your investments, then you may care less about impending market volatility. However, if you are consistently selling shares to generate spending cash—then a massive market decline (even if it’s only temporary) can spell disaster. In this report, we review current market valuation metrics (suggesting big danger on the horizon), we then explain why your anxiety level may be a symptom of something else (that needs to be addressed), we delve into the important question “how much cash should you hold?” and then highlight three specific “high income protection stocks,” before finally concluding with a very important takeaway.

Frothy Market Valuation

Were you selling stocks in early 2020 during the depths of the initial pandemic sell off? Whether you did so out of panic or because you needed the cash to cover expenses—you missed out on a truly massive market rebound.

And now, there is a growing chorus of investors suggesting the market is overheating. For starters, here is a look at the incredible dip then rebound of the S&P 500 following the 2020 pandemic lows (green line). Notice also the high unemployment rate, increasing inflation (CPI) and the very high S&P 500 price to earnings ratio.

And even if you are a pure stock picker (i.e. you don’t invest passively in the S&P 500) you know that big declines in the market drag just about every single stock lower.

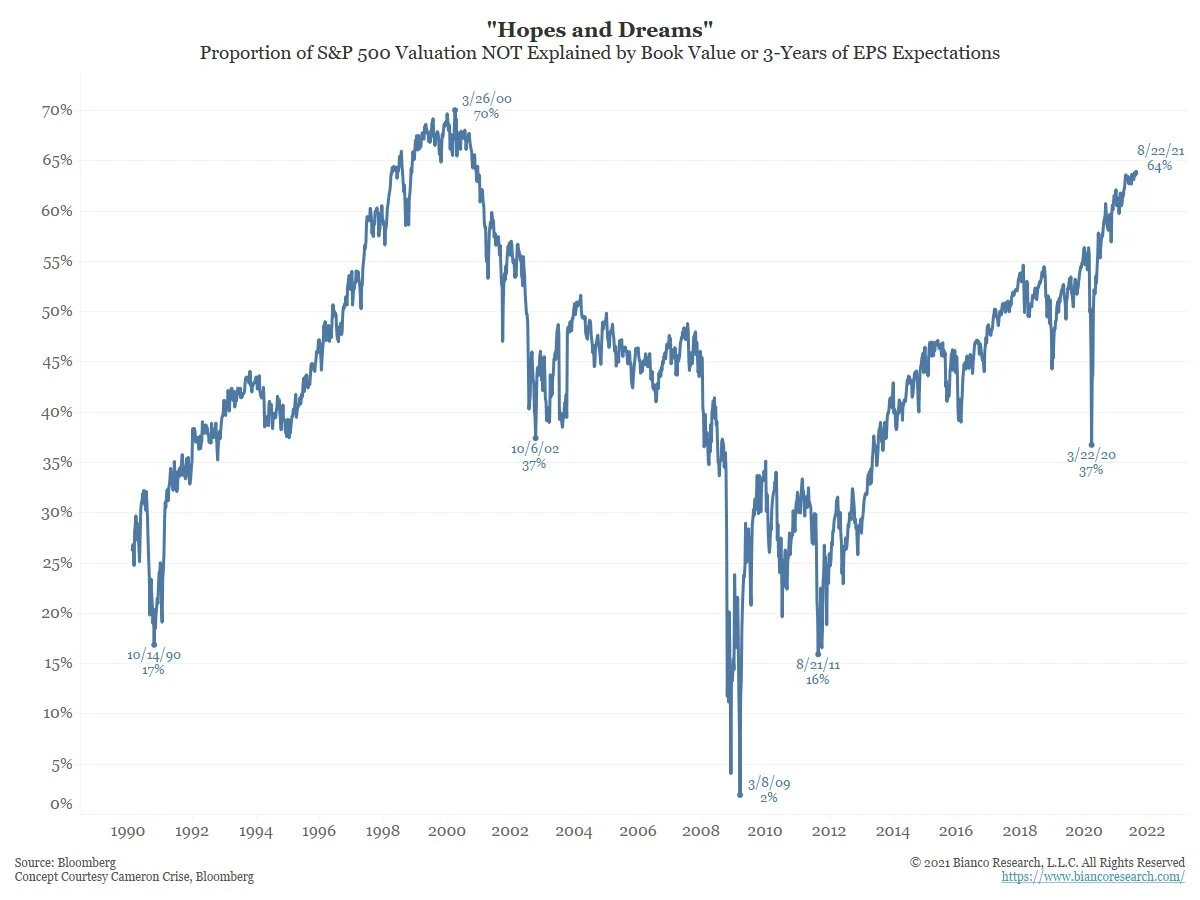

Next, here is a look at some analysis from Bianco Research that suggest the S&P 500 is dangerously expensive based on the sum of its 3 parts: the current value of assets (book value), the net present value of expected future earnings (i.e. the median S&P 500 earnings forecast by Wall Street analysts over the next 3 years), and a residual component (in this case referred to the “Hopes and Dreams” level).

And as you can see in the chart above, the “hopes and dreams” portion of the current S&P 500 valuation is dangerously high on a historical basis.

Moreover, this next chart shows “hopes and dreams” make up the largest portion since the tech bubble peak in 2000.

If you are particularly sensitive to near-term market volatility, this valuation data is concerning.

A Big Red Flag (Not What You Think)

To be clear, no one can predict the exact day and time of the next market sell off. For example, even Warren Buffett says:

“I don’t know, and perhaps with a bias, I don’t believe anybody knows what the market is going to do tomorrow, next week, next month, next year”).

However, if current market valuation metrics are causing you to lose sleep at night—it could be an indication of a different kind of problem. Specifically, it could be an indication that you are invested in the wrong types of investments for your own personal situation.

If you are in the early accumulation innings of your investments career (i.e. you don’t yet need your investments to generate spending cash) then you can tolerate another huge market sell off. After every historical market crash (e.g. the financial crisis, the tech bubble, etc.) the market has eventually rebounded, and as long as you held on to your investments (without selling) you’re better off for it.

However, if you need your investments to generate cash, then you may be invested in the wrong types of investments. For example, if 100% of your nest egg is in zero-dividend, high-growth, tech stocks—it may be time to reassess your strategy. For one thing, you might want to consider holding a few more dividend stocks (it can psychologically and financially feel great to keep getting paid big healthy income—even when the market is selling off), and it might also be time to hold a little more cash in your portfolio. Meeting your specific needs and sleeping well at night are both important considerations.

How Much Cash Should You Hold?

It seems there are as many different opinions about how much cash to hold as there are investors. However, the differing opinions are often not about determining the single right or wrong answer, but rather determining a prudent solution for your own individual situation.

For starters, you should hold at least as much cash as you need to meet your short-term obligations because few things can be more financially painful then watching the stock market crash (and the value of your investments crash) right before you need to pay for a very large expense. If you have an immediate cash need—that money should not be invested in stocks because they’re simply to volatile in the short term (i.e. remember the Warren Buffett quote from above).

How to Raise Cash

If you have short-term cash obligations, don’t wait to raise cash. Trying to eek out a few extra days, weeks or even months of stock market gains can spell disaster (again, no one knows where the market will be next week or next month, and a big crash is always a possibility—especially with many current valuation metrics arguably so very high).

Sell the things that aren’t consistent with your strategy, and don’t delay. For example, if you have just enough of a nest egg to support a comfortable lifestyle, you probably shouldn’t have 10% of your assets in Bitcoin. Bitcoin is highly volatile and unlike stocks there is no good way to value Bitcoin (it’s not a business that produces revenues, income or dividends). It’s fine to speculate a little if its consistent with your strategy and situation, but don’t go betting the farm on Bitcoin.

Using Cash: Income-Generating Options Trades

Many brokerage accounts offer money market sweeps so the cash in your account earns at least some interest (albeit, not a lot in today’s environment). Another strategy for your cash that we write about often (for our members) is selling income-generating put options. Perhaps more exotic, but this strategy is still consistent with our disciplined, long-term, investment philosophy.

Specifically, we often write about selling cash-secured, out-of-the-money, income-generating put options on stocks we’d like to own at a lower price. For example, we just shared a new trade with our members this week on Energy Transfer (ET) (an attractive high-yield equity investment in its own right). The trade put very attractive upfront premium income in our pocket (that we get to keep no matter what). And it also gives us a shot at picking up shares of this attractive business at an even lower price (if the shares fall below our strike price before the contract expires in about 3 weeks). This is a repeatable strategy that some investors (with cash balances in their accounts) like to implement on a regular basis.

3 High Income Protection Stocks

Next, if you are concerned about a market crash (which is always very possible—especially with current valuation metrics so high), you might instead want to considering investing in more “high income protection stocks.” Specifically, you might want to consider owning big-dividend stocks with the financial wherewithal to keep paying you healthy income even during big market selloffs. This can help you meet your financial obligations without being forced to sell anything at the bottom, and it can also help you sleep better at night. Here are 3 examples that we like.

1. Merck (MRK), Yield: 3.4%

A 3.4% dividend yield may not sound all that “high” to you, but it’s more than double the current yield on the S&P 500, the dividend has been increased for more than 10 years in a row, and it’s paid by a very healthy company that is currently a bit of an attractive contrarian play, in our view (especially as the share price has been weak this year). These are very attractive qualities if you are concerned about a market selloff.

And despite this year’s weak share price performance, Merck’s earnings-per-share is expected to grow at a healthy clip (12.8%) over the next 5 years and it trades at a reasonable forward price-to-earnings ratio (see table below).

The above table is from a recent members-only report, and Merck was one of thee names from the list that we found particularly attractive. Specifically, we believe Merck is on track for a strong post-pandemic recovery considering it was harder hit because it has a higher percentage of hospital administered drugs (people have been avoiding hospitals). We also like Merck’s divestment of Organon in June (leaving strong patent protection for the remainder of the portfolio).

Overall, we view Merck as a healthy contrarian play, especially if you’re looking for steady income and stability during a potential market sell off.

2. W.P. Carey (WPC), Yield: 5.5%

We recently shared a detailed W.P. Carey report, and it is worth revisiting here because it fits in well for those seeking steady income during potential market volatility.

For starters, WPC is a diversified REIT that had dramatically stronger rent collections during the pandemic than many of its peers. This is a tribute to the mission-critical nature of the properties and a tribute to WPC’s strength.

We also like that this business has been strategically shifting to more attractive industrial properties—a segment positioned well for the post-pandemic world (especially considering retail property demand was already in decline, and office property demand is fundamentally changing).

WPC has also paid a dividend for more than 10 consecutive years, and we view it as a good one to own during a sell off (we are currently long WPC).

3. Omega Healthcare (OHI), Yield: 8.2%

Omega is a healthcare REIT (focused on skilled nursing and assisted living) and it’s another attractive dividend stock, especially if you are concerned about the market overheating. Specifically, Omega has a 17+ year history of dividend increases, and it also has the added support of government funding to its tenants (though Medicare and Medicaid), which proved particularly helpful during the pandemic selloff in 2020.

Omega also has demographic tailwinds on its side (an aging population) and the share price recently sold off a bit (making for a more attractive entry point, in our view). For your reference, we wrote about Omega in more detail in our recent report: Top 10 Dividend-Growth Stocks.

Conclusion:

There are growing indications that the market is overheating and we may be due for a significant correction. No one knows the exact date and time, but current conditions should be particularly concerning if you are relying on market gains to generate income for living expenses.

To help you alleviate anxiety, make sure you own the right types of investments for your situation. We highlighted 3 attractive big-dividend payers in this report (that should keep paying steady income despite market volatility), and we share a variety of additional ideas in this report: 75 Big Dividend REITs, BDCs and CEFs (including three specific dividend stocks that are particularly compelling).

At the end of they day, the most important thing is to select investments that are right for you. Don’t go chasing after Bitcoin and zero-dividend growth stocks if your goal is steady high income. Disciplined, goal-focused, long-term investing is a winning strategy.