One of the biggest deterrents to successful long-term growth investing is near-term fear. Whether its driven by the relentless media fearmongering, short-term Wall Street valuation methodologies, or the psychological notion that people react far more negatively to short-term down moves than to up, near-term fear prevents many people from participating in massive long-term gains. It’s challenging for some investors to recognize the amazing power of compound growth, but it’s often referred to as the 8th wonder of the world by those who understand it. In this report, we countdown our top 10 growth stocks with massive upside potential (despite near-term fear), starting with #10 and finishing with our #1 top idea.

Trust But Verify: Do Your Due Diligence

Before diving right in, it’s worth mentioning, when you come across an article about top growth stocks, you might be hesitant to trust it considering the continuing proliferation of “get-rich-quick” people on the internet, ranging from one-sided cryptocurrency cheerleaders to outrageous penny stock dreamers. However, we support our views with a detailed fundamental research report for each stock on our list. It’s always important to do your own due diligence. It’s also good to be skeptical as an investor, and we’ve provided our detailed reports to help you make up your own mind.

Also, briefly, regarding our earlier comments about media fearmongering, short-term Wall Street valuation methodologies, the psychology of down moves versus up moves, and the power of compound growth—here is some perspective, starting with an ugly example of media fearmongering:

The Absurdity of Fearmongering:

The above screen shot shows the #1 trending article on popular retail investor website, Seeking Alpha, from earlier this week. Absolutely no one knows where the market is going in the short-term (or if a “big crash is imminent”), and headlines like the above are not only unnecessary, but they are an example of the media fearmongering that causes many investors to miss out on powerful long-term gains. A far better approach is to select attractive individual businesses/stocks, and then to hang on for the long-term (despite any near-term volatility), so you can enjoy the powerful long-term compound growth. We provide specific examples of stocks that are attractive in this regard, later in this report.

Use Appropriate Valuation Methodologies:

Regarding inappropriate short-term Wall Street valuation methodologies, it’s almost as if their models are trying to put round pegs through square holes. Typical analysts like to value companies using price-to-earnings ratios and discounted cash flow models. However, these are the absolute wrong approaches to valuing disruptive long-term growth stocks benefiting from massive secular industry changes—such as the ongoing digital transformation and migration to the cloud. The companies benefiting from these changes (many of them on our list later in this report) are often focused on capturing as much of the industry sales growth as possible now (to stay ahead of peers, gain first-mover advantages, economies of scale, and maintain their leadership positions within these massive market opportunity spaces), that their earnings are negative (actually a good thing for early-mover massive growth opportunity companies) and their cash flows seem insufficient (they’re spending massive cash on expansion so operating margins are often small or even negative, and this cash spending can also often include cash raises through secondary offerings—again—not necessarily a bad thing for this type of company).

Valuing top growth stocks is an art and a science. Specifically, appropriate valuation metrics are important (often including price (or enterprise value) to FORWARD sales estimates, for example), but so too is having the vision to recognize the intangibles of leadership in capturing scale in emerging and dynamic marketplaces that are not yet easily quantifiable. Analysts that do this, have far better results in capturing the most attractive long-term growth.

Behavioral Finance:

Next, regarding investors much stronger emotional reactions to down moves in the market (i.e. fear) versus up moves, here is a relevant quote from the Corporate Finance Institute on Loss Aversion:

“Loss aversion is a tendency in behavioral finance where investors are so fearful of losses that they focus on trying to avoid a loss more so than on making gains. The more one experiences losses, the more likely they are to become prone to loss aversion.

Research on loss aversion shows that investors feel the pain of a loss more than twice as strongly as they feel the enjoyment of making a profit.”

It’s important to keep your psychological bearings as an investor. Disciplined, goal-focused, long-term investing is a winning strategy.

The Power of Compound Growth:

And with regard to the amazing power of compound growth, here is a look at the stark difference in the value of your nest egg over time if it grows at 3% versus 6% and versus 12%, per year. You may be familiar with the rule of 72 (i.e. how long it takes to double your money at certain growth rates), but it’s not the first double that matters, so much as the 4th, 5th, 6th and beyond! And hanging on to your winning long-term businesses, despite relentless naysayers and fear mongers, is a big part of the challenge. And despite any short-term volatility, it’s the long-term compound growth that matters.

In reality, the lines won’t be so smooth (there will be volatility), but in the long run that won’t matter. Compound growth works despite short-term volatility. And for those of you with an even longer-term horizon, here is a look at the same chart over a longer time period. The benefits of long-term compound growth is truly impressive.

And to add a little more color to the power of compound growth, here is a look at two more outstanding charts on compound growth with regards to revenue growth and price-to-sales (important metrics to consider for the names on our top 10 list), and revenue growth versus price-to-2021-gross profit (also important, especially gross profits, for the names on our top 10 list).

source: Luca Capital

source: Richard Chu

A Note on Volatility:

It is worth mentioning again that short-term volatility is often the price you pay for the most attractive long-term growth. Once small companies like Amazon, Facebook and Google have all experienced dramatic share price drawdowns in their history, but they all marched dramatically higher over the long-term. They are great examples of the power of long-term compound growth (if you have the fortitude to hang on through short-term volatility and fearmongering) because they are all now massive companies, and investors that hung on to their shares over the years made a lot of money! A lot. Top growth stocks don’t go up every day, every week or even every quarter. But they do go up a lot—and experience amazing compound growth—over the long term.

Growth Stocks Just Sold Off Hard

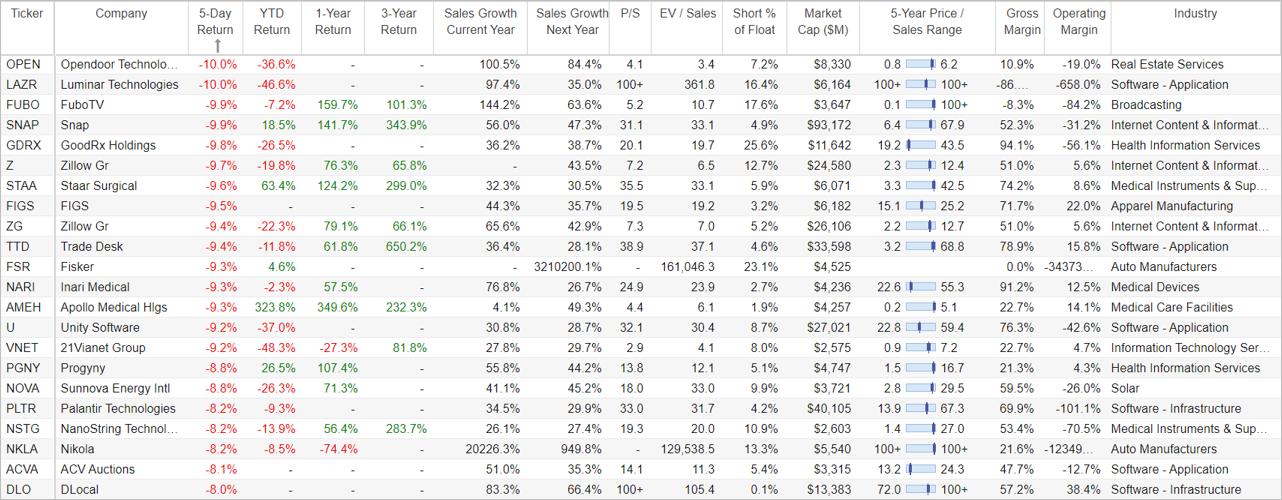

Finally (before we get into the Top 10 Growth Stocks), it’s also worth noting that many top growth stocks (those with the highest expected sales growth rates for this year and next) just sold off hard over the last week, as you can see in the following table (for perspective, the S&P 500 (SPY) was down about 1% last week, and the Nasdaq (QQQ) was down about 0.9%). And despite here-today-gone-tomorrow narratives about inflation and this being the start of the next “big crash”, we view this sell off as mainly short-term “noise,” especially for the top long-term growth stock names on the list.

source: Stock Rover, data as of 7/16/21

Top 10 Growth Stocks:

With that backdrop in mind, let’s transition into our top 10 growth stocks, starting first with an “honorable mention,” and then getting into #10, #9, #8 and all the way down to our #1 top idea.

*Honorable Mention: Accolade (ACCD)

Accolade is a rapidly growing healthcare company with a $3 billion market cap. Specifically, the company provides technology-enabled solutions that help people understand, navigate, and utilize the healthcare system and their workplace benefits. The company has a very large and growing total addressable market opportunity (currently ~$24 billion), and here is a look at the company’s current high revenue growth trajectory.

ACCD Revenue Growth, source: Seeking Alpha

Accolade has a proven business model, that simplifies the complex consumer health benefits journey, and delivers cost savings. The shares sold off earlier this month as it announced EPS short of expectation (even though revenue growth was ahead of expectations).

We’re including Accolade as only an honorable mention because its operating margins are still very negative (even though it’s spending heavily on growth—a very good thing), and even though its attractive recurring revenue model is consistently delivering margin improvement. We’re keeping Accolade high on our watchlist for now, and you can read our previous full report on Accolade here:

10. NIO Inc (NIO)

Electric vehicles are a big deal in the US because people care about reducing carbon emissions, they want to spend less on gas, and because Elon Musk made them cool. And considering China has a bad reputation when it comes to the environment, you’d think electric vehicles would be a big deal there too. And it turns out—they are.

pictured: NIO eT7, source: NIO.com

NIO is a Chinese automobile company that designs and manufactures electric vehicles primarily targeting premium markets. NIO went public in 2018, and it has been enjoying rapid sales growth. And even more important, NIO has a massive total addressable market opportunity (so it can keep growing rapidly) and it has the backing of the Chinese government.

NIO Revenue Growth, source: Seeking Alpha

We also like NIO’s unique strategy to reduce cost and facilitate EV adoption (Battery as a Service (BaaS)), plus the valuation is more compelling after the recent price dip.

image source: YCharts

The NIO fearmongers are in no short supply, suggesting the valuation is too high, the competition is too great and China is too big of a risk factor. We disagree, and you can read our previous full report about why NIO is an attractive long-term investment, here:

9. StoneCo (STNE)

StoneCo is a Brazil-based fintech company that provides retail merchants with electronic payment and short-term financing related solutions to manage their businesses across in-store as well as online channels. Its target customers primarily include micro, small, and medium-sized businesses across several industry verticals in Brazil. The company also provides services to nearly 260 integrated partners including global payment service providers, independent software vendors, and digital marketplaces, who embed StoneCo’s payment solutions into their own offerings to enhance the user experience.

We like StoneCo’s business, especially because it enjoys a very high growth rate and a massive total addressable market opportunity to keep growing over the long term.

StoneCo revenue growth, source: Seeking Alpha

We also like that StoneCo is consistently gaining market share in a highly competitive industry, and that it is broadening its ecosystem which will lead to an increasingly sticky customer base. The company has also experienced an impressive expansion in margins and has a very healthy balance sheet.

Fearmongers and naysayers will point to this company’s valuation being too rich and its volatility being too high to handle. However, we disagree.

image source: YCharts

Near-term volatility is the price you often pay for attractive long-term growth, and the recent price pullback has made the valuation more attractive. You can read our recent detailed full report on StoneCo here:

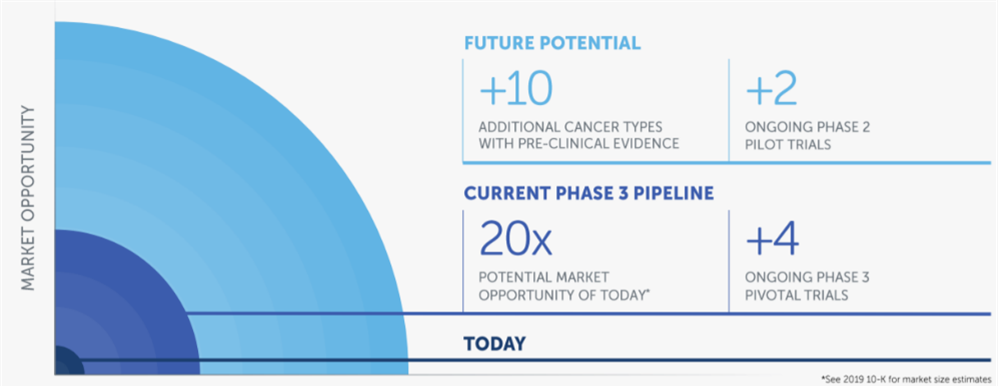

8. NovoCure (NVCR)

NovoCure is a global cancer treatment company possessing patented Tumor Treating Fields (“TTF”) technology (for treating some of the most aggressive forms of cancer). The company has put itself on a path for continuing revenue growth, and it has a large total addressable market opportunity.

NovoCure revenue growth, source: Seeking Alpha

Source: Company’s Corporate Presentation

We went into great detail in our previous full report on NovoCure earlier this year, and the shares have been volatile lately, most recently experiencing a sell off after the company released the results of its liver cancer study earlier this month.

source: YCharts

Despite the market sell off, we actually viewed the results as positive, and we view the sell off as a more positive entry point for long-term investors. And if you are one of those investors that is overly fearful of near-term volatility, then you might consider a strategy similar to the bullish vertical put spread we describe in the following link—however sometimes it’s better to just buy the shares and hang on (despite volatility) for the long-term.

7. Palantir (PLTR)

Palantir is a software company that is growing rapidly and has a massive total addressable market (to keep growing for a long time). It provides big data analytics solutions (ranging from data mining to visual analytics), on a single consolidated platform, thereby enabling informed decision-making. The company is having great success landing and expanding government agency contracts, but is also recently attempting to diversify into enterprise-grade commercial organizations too.

The share price has pulled back from all-time highs in recent months, but the long-term growth story remains intact and the valuation is now more reasonable.

Palatir revenue growth, source: Seeking Alpha

And in addition to the attractive business, we also particularly like Palantir’s subscription model, its high gross margins, and its customizable solutions (which lead to a very sticky customer base).

If you are looking for more detailed information and analysis on Palantir (including it business model, its market opportunity, financials, valuation and risks) you can check out our latest detailed report on Palantir here:

*Honorable Mention: Oak Street Health (OSH)

Oak Street Health is getting an honorable mention on this list for its high growth rate and large total addressable market opportunity. It operates a network of primary care centers to deliver value-based care exclusively to Medicare eligible patients in medically-underserved communities. Here is a look at the revenue growth trajectory.

Oak Street Health revenue growth, source: Seeking Alpha

Oak Street Health has been at the forefront of implementing a highly differentiated technology enabled value-based primary care model that aligns the incentives of all the stakeholders in the provider ecosystem to capture the market opportunities that are being generated from the poor health outcomes, which are primarily a result of flaws in the US healthcare system

The company went public in August 2020, and the shares have continued to trade a tight range with an upward trajectory.

We do not own shares of OSH, but we have been sharing some interesting trading opportunities with our members, and you can read one such example here:

6. Futu Holdings (FUTU)

If you are looking for a very-high long-term growth stock, you may want to consider this Hong Kong based online brokerage and wealth management firm. Revenues are expected to grow at over 100% this year. And the company’s impressive integrated platform (e.g. stock trading, margin financing, wealth management, market data and interactive social features) is expanding thanks to its high R&D budget and important relationship with Tencent (the preeminent Chinese internet juggernaut).

Futu revenue growth, source: Seeking Alpha

Both the share price and forward price-to-sales ratio have fallen, thereby creating a more attractive entry point, in our view.

One of the biggest risks for Futu is simply the Chinese government. However, the valuation already over-compensates for that risk (if this were a US company it would trade at much higher valuation multiple).

There is a lot to like about Futu. And for all the details, you can read our previous full report on the company, here:

*Honorable Mention: Salesforce (CRM):

We’re including Salesforce as on honorable mention in this report because it is a powerful long-term blue-chip growth stock. It’s profitibale and it has room to keep growing, but it’s already quite large and its expected growth rate is lower than other names on this list.

Salesforce revenue growth, source: Seeking Alpha

We currently own shares of Salesforce, and you can view our full report on the company (and why it is so attractive) here:

5a. Square (SQ)

We’re adding two names at number five (part a and b), and we are starting with financial-services / digital-payments company, Square (SQ). Square provides tools to merchants (or sellers) to help them to manage and grow their business, and provides tools to consumers (or buyers) to help them send, receive and manage their money. And importantly, Square has a very high growth trajectory and a very large total addressable market opportunity (fintech is huge!).

Square (SQ) revenue growth, source: Seeking Alpha

Square’s business has faced challenges during the pandemic (particularly on the sellers side), but has also made gains (on the consumer side), and is positioned well to keep growing rapidly, especially as vaccine rollouts continue.

We currently have a significant position in Square, and you can view our full detailed report on the company here:

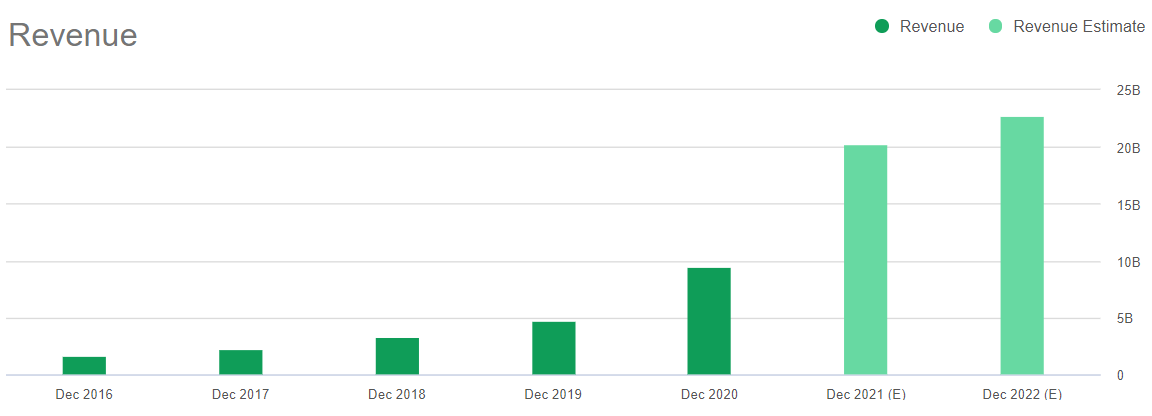

5b. The Trade Desk (TTD)

The Trade Desk (TTD) is growing rapidly. The company’s self-service software platform (that enables ad agencies and brands to make data-driven ad placements across a variety of mediums) is benefiting dramatically from secular growth in digital ads and Connected TVs, in particular. Here is a look at recent and expected revenue growth.

The Trade Desk revenue growth, source: Seeking Alpha

More specifically, The Trade Desk offers a real-time bidding, cloud-based platform to advertising agencies and brands to make their ad placements fair and personalized across the open internet. Open internet refers to multiple formats and devices including targeted display video, Connected TVs (CTVs), online news platforms, social ads, and audio content, to name a few.

The shares trade at a rich valuation, but they are well worth it—considering the high growth and massive market opportunity.

We continue to have a significant position in The Trade Desk shares, and we are comfortable that the long-term upside potential outweighs the near-term volatility and competitive risks. You can read our detailed full report on The Trade Desk, here:

4. Teladoc (TDOC)

Sentiment is driving shares of this telehealth leader lower in the near term. However, the long-term story is still very much intact as the growth rate and growth opportunity remain high and large, respectively.

The shares have sold off in recent months as the market continues to overreact to the “pandemic trade” narrative, without realizing TDOC is not a flash in the pan, but rather a tremendous long-term growth opportunity. Further, some investors are turned off in the near-term by the company’s signal of little membership growth for 2021, as well as the loss of a Fortune 500 company contract. However, the company remains on track to deliver 30%-40% revenue growth in the medium-term. We also like the recent collaboration with Microsoft.

TDOC revenue growth, source: Seeking Alpha

In our view, the market’s negativity is dramatically overblown, and an attractive buying opportunity exists. We currently have a significant position in shares of TDOC, and you can view our recent full report reviewing the health of the business, growth opportunities, valuation, risks, and more—in this report:

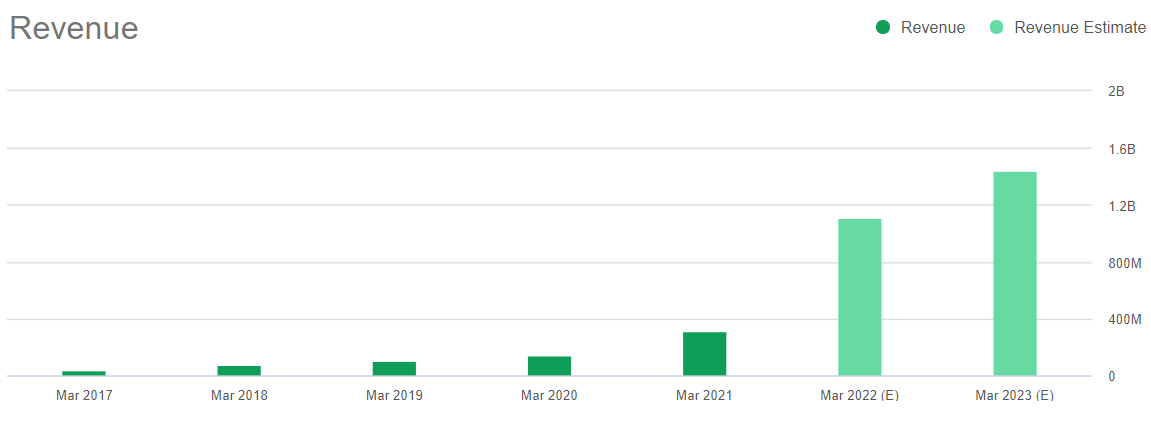

3. Digital Turbine (APPS)

Digital Turbine Inc. (APPS) is an on-device media platform which works with wireless carriers and device OEMs to pre-install apps on new devices. The business model is attractive, the market opportunity is very large, and revenues continue on an attractive trajectory higher.

Digital Turbine revenue growth, source: Seeking Alpha

Further, the share price has recently pulled back on noise, thereby creating a more attractive entry point for long-term investors (more on this in our detailed report, linked below).

You can view our new report on Digital Turbine here:

2. Enphase (ENPH)

Enphase Energy is a leading provider of microinverters and batteries used for solar energy generation and storage.

And the shares offer an impressive combination of high growth, high margins and attractive valuation.

Enphase revenue growth, source: Seeking Alpha

We currently own a significant amount of Enphase shares, and you can access our full report on the company, here:

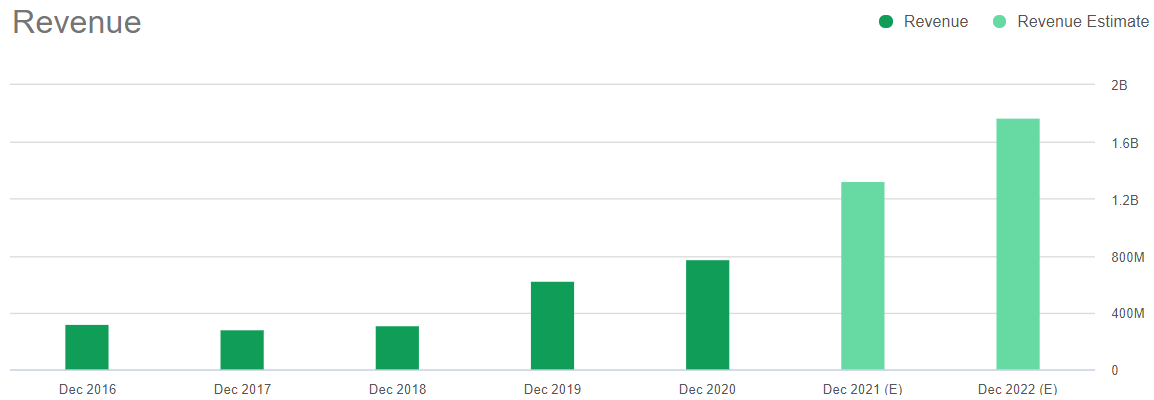

1. Roku (ROKU)

There’s a lot to like about Roku (the largest TV-based on-demand streaming platform in the US), starting with its dramatic business growth thanks to the global shift from linear TV to over-the-top (“OTT”) streaming services.

ROKU revenue growth, source: Seeking Alpha

The company is consistently delivering powerful top and bottom-line growth, driven by an increasing number of users and higher advertising revenues. It’s also taking initiative to expand into international geographies (to fuel more growth), and it enjoys a very large and expanding total addressable market opportunity.

We currently have a large position in shares of Roku, and you can view our full report here:

The Bottom Line:

If you are going to invest in long-term growth stocks—be prepared to suffer the slings and arrows of both volatility and relentless fearmongering from others—mainly the media. However, if you have the fortitude to buy great businesses and then hang on for the long-term—your results can be truly amazing. We have attempted to share a variety of top growth stocks in this report—many of them we currently own.

We are having great long-term success with our long-term Disciplined Growth portfolio, and you can view all our current holdings here: