If you don’t know, The Trade Desk (TTD) is growing rapidly. The company’s self-service software platform (that enables ad agencies and brands to make data-driven ad placements across a variety of mediums) is benefiting dramatically from secular growth in digital ads and Connected TVs. Further, the company’s recent launch of a more secure and effective Unified 2.0 solution (an alternative to cookies) has added to the growth momentum. But is the company’s valuation simply too high? In this report, we review The Trade Desk’s business model, its market opportunity, financials, valuation and risks, and then conclude with our opinion on whether the shares offer an attractive balance between risks and rewards.

Overview

Trade Desk is a leading Demand Side Platform (DSP) provider that offers a real-time bidding, cloud-based platform to advertising agencies and brands to make their ad placements fair and personalized across the open internet. Open internet refers to multiple formats and devices including targeted display video, Connected TVs (CTVs), online news platforms, social ads, and audio content, to name a few. The company’s software platform enables ad agencies and brands to leverage data-driven advertisement capabilities, real-time optimization and monitoring of their ads, internal and external data integration capabilities, enterprise APIs to customize the user interface, and various other features. This makes its platform more than just a digital ad exchange as it not only allows fair pricing for ad inventory through competitive bidding but also helps advertisers find better spots for ad placement. Large number of ad-buyers on the company’s platform have led to an increase in ads and data inventory suppliers as well. The company has a total of 82 directly integrated ad exchanges and supply-side platforms and 237 third-party data vendors on its platform as of FY 2020.

The Trade Desk earns revenue by charging a platform fee. This is a percentage of total gross spend by clients on advertising, data management, and other features on company’s platform. This fee has averaged almost 20% of total gross spend over the last 6 years. The company recorded a total of 875 clients as of FY 2020, of which Omnicom Group Inc. and Publicis Media Inc., global advertising and PR companies accounted for over 10% of total gross billings each. Geographically, the US accounted for almost 84% of total gross billings. The company is well diversified across all major business verticals as shown below.

Source: Company’s Investors Presentation

Fueling growth through programmatic digital advertising

With millions of websites, and numerous other digital applications available, the need for building an effective platform with ad publishers and buyers on a single platform has become increasingly important. Digital ad exchanges solve this problem by enabling ad-space buyers to place their advertisements on the desired medium in real-time through competitive bidding. Programmatic advertisement offers automated ad trade through AI and machine learning algorithms with minimal human intervention. Along with being a DSP provider, Trade Desk’s programmatic advertising enables its customers to trade ads in real-time and monitor and optimize them. Further, the company offers an all-in-one self-service platform that helps ad-buyers streamline costs as shown below.

Source: Investors Presentation

As per eMarketer, US programmatic digital display ad spending as a % of total digital display ad spend is expected to increase by 200 bps from 84.5% in FY 2020 to 86.5% in FY 2021. The upward trajectory is expected to continue in FY 2022 with further improvement of 170bps YoY. Growth is expected to resume post pandemic with mobile, video and programmatic digital display ad spending on Connected TVs (CTVs) leading the way.

Source: eMarketer

Large and growing Total Addressable Market (TAM)

The Trade Desk is leveraging two important secular growth trends. These are acceleration in global digital ad-spend and surge in programmatic advertising. While the latter has already been discussed, the former is also expected to remain an important factor in the company’s growth going forward. As per eMarketer, digital ad spending as a % of total ad spending is estimated to increase by almost 960 bps from 58.2% in FY 2020 to 67.8% in FY 2024. This growth will largely be driven by display ads that include mobile and online video ads. The fact that the company has already partnered with over 38 premium mobile partners including TikTok, rubicon, etc., and over 56 premium online video partners such as Vevo, Teads, and many others provide it with ample ad inventory to attract a large volume of ad-buyers on its platform.

Source: eMarketer, Investors Presentation

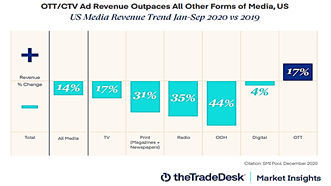

Pandemic was a catalyst for Connected TVs (CTVs)

“CTV advertising has been building over the past few years, but 2020 was a step change with myriad streaming platforms vying for consumer attention and increased opportunities for marketers to make conscious connections.” – Sean Muzzy, President, North America, Matterkind

While FY 2020 remained depressed in terms of revenue earned through ads across all media, CTV/OTT saw a 17% surge as per business intelligence company SMI. The Trade Desk expects this trend to continue making CTV/OTT based advertisements a driving force for future growth. Anticipating the rise in cord-cutting, the company has consistently struck breakthrough partnerships with media and entertainment companies. Its recent partnership with NBC Universal will bring interactive e-commerce to streaming TV through NBC’s ad-tech stack, One Platform. NBCU will also provide other ad inventory through The Trade Desk including CNBC International and Sports to allow ad agencies and brands to reach global audiences. Additionally, the company has been focusing on international geographies. It partnered with Chinese media companies such as Tencent and Baidu Exchange Services opening a gateway for western agencies to buy ads in China and tapping a market with almost a billion internet users.

Source: Trade Desk

Unified 2.0 gathering momentum

Another momentum gainer for the company is the recent launch of its ‘post cookie’ solution, Unified 2.0. Cookies are redundant on Connected TVs and mobile applications allowing Unified ID 2.0 technology to flourish in fast growing ad segments. UID 2.0 works in the same way as third-party cookies however, it provides complete anonymity by creating a unique ID of strings and numbers that cannot be reverse engineered to get real identity of users. Moreover, it gives full control to users for their data by allowing them to visualize how their data is used. Besides, it offers better ad-targeting than traditional cookies. In fact, the solution has found support from a variety of ad-tech players including LiveRamp, Nielsen, Criteo, and many others.

However, Unified 2.0 requires consent from users for using their data by making them enter their email ids. This might be an easy task for big publishers however, small to medium scale ad-publishers may find it difficult. In fact, as a part of Apple’s recent ATT update, a mere 4% of users in the US opted to be tracked by apps thus pointing to a possibly discouraging trend for Unified 2.0 going forward. Another challenge for UID 2.0 comes from Google’s privacy sandbox Federated Learning of Cohorts (FLoC) announcement last year which is still in the early stages of development. FLoC is expected to provide aggregate set of data to advertising agencies rather than individual data thus making it harder to identify individual users leading to better privacy control. It is important to note that the “Walled Gardens” that include Google, Facebook, and Amazon hold over 70% of the US digital ad market share. They also have the capabilities to develop their own post cookies solutions such as FLoC from Google. This presents a potential threat for Trade Desk over the mid to long term and something investors need to track for any further developments.

Consistent growth in the top-line and adjusted EBITDA

The Trade Desk reported $219.8M in total revenue in Q1 2021. This represents a YoY growth of almost 37% from $160.7M in Q1 2020. The top-line growth is primarily attributable to improvement in gross spend from both advertising agencies and brands. Connected TV (CTV) again was a key growth driver. It is important to note that the company’s top line has grown at a 5-year CAGR of almost 49%. During the quarter, The Trade Desk expanded its partnership with Walmart to launch a new DSP that will provide advertisers access to Walmart’s shoppers and sales measurement data. And the customer retention rate remained over 95% during the quarter. It expects $260.5M in total revenue for Q2 2021 which will represent a YoY growth of almost 87% at mid-point.

Source: Company’s Press Releases

The Trade Desk reported adjusted EBITDA of $70.5M in Q1 2021 representing almost 32% of total revenue as compared to an adjusted EBITDA margin of 24% same quarter last year. The improvement was largely driven by company’s strong top-line growth. The company’s adjusted EBITDA has grown at a 5-year CAGR of almost 80%. It is expecting $84M in adjusted EBITDA in Q2 2021 which will represent an adj. EBITDA margin of 32%.

Profitable since 2013 leading to a robust balance sheet

The Trade Desk has been GAAP Net Income positive since 2013. It reported $23M of GAAP Net Income for Q1 2021 representing almost 10% of total revenue as compared to Net Income margin of 15% in Q1 2020. For Q1 2021, it reported almost $76M in CFO and $13M in capital expenditure, implying Free Cash Flow (FCF) of $62M.

The Trade Desk had almost $681M in liquidity which includes $472M in cash and cash equivalents and $209M of short-term investments with no debt as of March 2021. More recently, the company announced a 10:1 stock split in order to make the company’s stock more accessible to retail investors as well as its employees (the shares currently trade at around $77.50).

Premium Valuation on Premium Growth

The Trade Desk may appear to trade at a steep premium as compared to its peers, however investors should not underestimate the power of long-term compound revenue growth. For example, if TTD grows revenue at 30% for each of the next 5 years, then its price-to-sales ratio falls below 10, which is a much more palatable level for some investors. Specifically, TTD’s incrementally higher growth rate (relative to peers) makes a big difference over the mid- to long-term as revenue growth compounds (i.e. compound growth is often said to be the “8th wonder of the world”). Here is a look at The Trade Desk’s valuation and growth as compared to other high-growth companies operating in the Interactive Media and Services industry such as Facebook, Amazon, and Pinterest.

Further, we expect The Trade Desk’s unique business model to continue to fuel high growth for years into the future considering the very large total addressable market opportunity in digital advertising and specifically the programmatic advertising space.

Risks

Intensely competitive landscape: Trade Desk faces intense competition from “walled gardens” comprising of companies such as Amazon, Google, and Facebook. These large players have an enormous amount of data which positions them well to leverage data-driven ad placement capabilities. Besides, these companies operate their own platforms with ample users enabling them to earn gross billing amounts from advertisement agencies and brands. In fact, as per digital commerce 360, out of total ad spend on Amazon DSP in Q4 2019, almost 69% was accounted by Amazon’s owned and operated websites such as Kindle, Fire TV, etc. While Trade Desk’s focus on just the demand side has enabled it to remain out of controversies that these walled gardens face, large amount of data with significant data management and analysis capabilities may threaten Trade Desk’s position in the long-run.

In Connected TV (CTV) market, possible consolidation of DSP platforms and CTV manufacturers and service providers also poses a threat going forward for Trade Desk. Despite significant breakthrough innovations including UID 2.0 by Trade Desk, intense competition from big players may limit upside potential over the long term.

Google’s elimination of third-party cookies: Google is actively working on reducing privacy concerns through elimination of third-party cookies. A significant step that the company took was investing in Federated Learning of Cohorts (FLoC). While a concrete solution is yet to be launch-ready, we believe that Google is taking the initiative seriously. Despite Trade Desk’s open-source Unified ID 2.0 solution for third-party cookies elimination, a similar solution from Google can hurt company’s competitive positioning considering latter’s superior data base and strong positioning in the market.

Conclusion

Trade Desk has grown to become one of the largest and fastest-growing independent DSP providers. Revenue and adjusted EBITDA growth has remained impressive in the last few years. However, the company faces formidable competition in the form of Google, Amazon, and Facebook that leverage in-house DSPs.

On the valuation front, The Trade Desk appears to trade at a steep premium, but when you factor in the tremendous growth potential, the premium is reasonable. We acknowledge that the share price will likely continue to be volatile (especially as investor expectations around interest rates change), however we believe the long-term growth potential outweighs the near-term volatility risks.

We continue to have a significant position in The Trade Desk shares, and we are comfortable that the long-term upside potential outweighs the near-term volatility risks. In our estimation, these shares are likely eventually going much higher.