The common shares of this once beloved mortgage REIT suffered significant equity erosion earlier this year (and it was forced to cut its dividend by 90%) as it was hit with margin calls and forced to liquidate assets at depressed prices during the market-wide Covid-19 sell-off. Since then, the company has been limping its way back towards better health, albeit with a significantly less valuable book of business. Furthermore, the company’s three series of preferred shares still trade at attractively discounted prices and offer compelling high yields (they are also insulated, from some risks, by the company’s common shares). In this article, we review the business, the shares (common and preferred), and then conclude with our opinion on investing.

(Purple Line: NRZ Price, Orange Line: NRZ price-to-book, source: yCharts)

Overview: New Residential (NRZ)

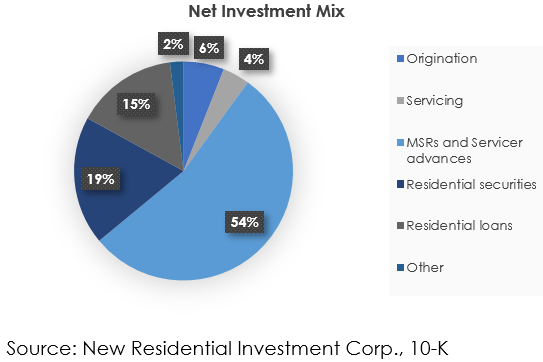

Incorporated in 2013, as a spin-off from Drive Shack, Inc., New residential Investment Corp. is a REIT that primarily invests in residential mortgages and mortgage related assets. The company is externally managed by Softbank-owned, Fortress Investment Group, and has asset under management of $18.5 billion as of second quarter FY-20. NRZ’s business model involves sourcing credit at lower interest rates and investing in mortgage related assets that generate higher yields, thereby earning a positive spread. NRZ’s investment portfolio is divided into the following investment strategies:

Origination: Through this business, NRZ provides loan refinance facilities to its existing servicing customers and it also purchases loans from mortgage brokers or other originators through retail or wholesale channels. These loans are then sold off to GSEs or other institutions and NRZ earns gains as an intermediary in the transactions. Also, NRZ retains the mortgage servicing rights of these loans and earns servicing fees during the entire tenure of the loan. Prior to COVID-19, NRZ was primarily involved in originating non-qualified loans i.e. residential mortgage loans which are not backed by govt. agencies, however, post pandemic, the mortgage markets saw significant loss of investor appetite for Non-QM loans. As a result, NRZ has now shifted its business model to focus on origination of more liquid agency loans which can be sold to GSEs. Origination assets comprise 6% of the total net equity investments of the company.

Servicing: Through this business, NRZ conducts servicing of performing and delinquent loans on behalf of the owners of underlying mortgages. These services include collecting loan installments, returning principal and interest to investors, payment of taxes and insurance, administering loan modifications, overlooking foreclosures, etc. Servicing assets make up 4% of the total net equity investments of NRZ.

MSRs and Servicer advances: This is the largest investment segment of the company and accounts for 54% of the total net equity investments. Mortgage Servicing Rights ("MSR") provides a mortgage servicer with the right to service a pool of mortgage loans in exchange for a fee. The MSR holder’s responsibility is the same as in the servicing business segment. An MSR is comprised of 2 components: Base Fee and Excess MSRs. Base fee is the amount charged for performing mortgage servicing duties whereas excess MSR is the amount over and above the basic fee. Excess MSRs can be carved out as a separate asset and can be sold to other institutions. For the excess MSRs which NRZ owns, it collects monthly cash flows from the MSR, but does not assume any servicing duties, advance obligations, or liabilities associated with the portfolios underlying the investment unlike the case in full MSRs. NRZ is required to service the principal and interest payments to mortgage lenders even if the borrower defaults or forbears mortgage payments. These payments are called servicer advances. The liquidity requirements have been significantly amplified in the current economic scenario as borrowers are allowed to request mortgage payments forbearance for a period of 180 days or more because of COVID related hardships. NRZ is entitled to receive proceeds from the liquidation of the underlying portfolio once a default does happen, however that can take time, and meanwhile it is supposed to transfer payments on underlying mortgages to investors. Also, the value of MSR investments is directly related to interest rates. MSR values are currently at their lowest levels because of ultra-low interest rates as low interest rates have led to increased loan pre-payments and advancements in the period for which NRZ is entitled to hold the servicing rights.

Residential securities: In this segment, NRZ holds non-agency residential mortgage backed securities. These investments account for 19% of the total net equity portfolio of the company.

Residential loans: In this segment, NRZ directly invests in performing or non-performing mortgage backed loans. These investments account for 15% of the total net equity investments.

Massive Portfolio Erosion Due to Late March Sell-Off

The Covid-19 pandemic led to a significant dislocation in capital markets including the residential mortgage markets. A sharp sell-off was observed in all asset classes as unemployment rates reached historical highs when stay-at-home orders came into effect in late March. Residential mortgage markets were not spared from this panic selling as spreads skyrocketed to levels last observed during the 2008-09 global financial crisis. NRZ’s Non-Agency RMBS investments and residential mortgage loan investments lost a substantial amount of value during this massive sell-off. As these investments were financed primarily through short-term repurchase agreements (with the assets owned serving as collateral), a sharp decline in underlying values led to an increase in margin calls on these credit agreements. In an attempt to reduce the credit risk from these securities and avoid margin call risk, NRZ liquidated a major portion of its RMBS and residential loans portfolio at considerably low valuations resulting in high realized and unrealized losses at the end of Q1 FY 20. NRZ’s total investment in loans, call rights, and MBS which amounted to over $26 billion at the end of last year, trimmed by more than 50% to just over $12 billion by Q2 2020. On a percentage basis, the share of MBS and residential loans in the total net equity investments declined from 46% to 34%.

Additionally, as discussed, over 50% of the company’s investments consist of mortgage servicing rights (MSRs). With the CARES Act coming into force, NRZ will be required to remit principal and interest on mortgages backed by Government sponsored enterprises (GSEs) even if it is unable to collect the installments from the borrower because of forbearance period. Due to this increased need for liquidity in the near term, the company has been forced to maintain a high cash position. Consequently, NRZ sharply cut its common dividends by 90% from $0.50 per share to $0.05 per share.

Normalcy returns to business environment post Fed intervention

The financial markets (including the residential mortgage markets) have greatly recovered since March as the federal reserve has infused substantial liquidity in the markets to support its smooth functioning. Between mid-March and mid-August, The federal reserve has injected $892 billion of liquidity by purchasing agency MBS and announced that they will continue to purchase assets to maintain market stability. Accompanied with that is the reduction in the Fed Funds Rate—which has driven mortgage rates to historically low levels.

After a spike in the initial weeks of Q2 2020 when the CARES Act was announced, forbearance rates have also fallen to their lowest levels in last 5 months. The percentage of borrowers granted forbearance has dropped to 7.8% from a peak of 8.4%. Additionally, mortgage servicers have received support from the government in the form of the Ginnie Mae PTAP program and FHFA capping servicer obligations to 4 months of P&L during the forbearance period. NRZ has secured excess capacity of $2.2 billion to meet any servicer advance needs due to forbearances. Given the strong improvement in business environment post Q1, NRZ increased its quarterly common dividends by 100% to $0.10 per share in June and again by 50% to $0.15 per share in September.

NRZ’s accelerating shift to an operations-focused business

As mortgage rates hit lows, NRZ is experiencing strong growth in its loan origination business because of the increase in volume of both new mortgages as well as refinancing. Investors must note that NRZ was already in the process of moving towards operating activities in recent years (i.e. it is moving towards the origination and servicing business to generate stable and reliable fees as a source of revenue).

To establish itself as an operating company, in 2017, NRZ acquired Shellpoint Partners which is a GSE-approved vertically-integrated mortgage platform with strong origination and servicing capabilities for $190 million. Later in 2019, NRZ acquired MSRs as well as the servicing and origination business of Ditech Holdings for $1.2 billion. NRZ’s efforts to re-model its business appears to be paying off as its operating business, especially the origination business, was the primary driver of improved earnings by the company in Q2 2020. Specifically, it generated record pretax income of $181 million in Q2 from originations which represents a QoQ increase of 201%. This jump was primarily a function of a significant increase in new mortgage originations and loan refinancing as well as the increase in gain on sale margins. One of the important drivers for the increase in sales margins is expansion of high profit generating direct to customer (DTC) channel of loan origination.

With social distancing norms still in place, NRZ leveraged its technology platform and marketing skills to reach out to increased number of customers. The advantage of DTC channel is that it helps NRZ deliver improved services to its customers, has higher conversion rates, and generates higher gains on sales margins. Additionally, it improves recapture rates through better service relationships. Through higher recapturing and customer retention NRZ can achieve increased market share and minimize MSR amortizations even in a falling interest rate environment.

“Our origination and servicing business continue to be a primary focus. The return on equity in that business has been very, very good. As we sit in this robust housing market, robust refinancing market, we want to make sure that we continue to perform extremely well there. And you saw the results in the first quarter.” - Michael Nierenberg, CEO in Q2 2020 earnings call

Source: NRZ, Supplementary Information

With Fed expected to continue its loose monetary policy in the near to medium-term, the macro environment is supportive of NRZ’s origination business as the demand for new residential loans will continue to remain strong. The company is estimates $50 billion of loan originations this financial year and pre-tax income of $750 to $800 million from origination and servicing businesses for the full year.

Natural hedges in the business will provide long-term income stability

Investors must note that NRZ’s origination business and MSR portfolio are driven by opposite forces. As interest rates fall, the company’s origination business delivers strong performance while its MSR investments lag due to increased amortization rates resulting from faster prepayment of underlying borrowings. As interest rates rise sometime in the future, the origination business will see some loss of momentum, however, gains in the MSR investments will offset the reduction in earnings from origination. The combination of the two businesses means some cushion to earnings and lower volatility going forward.

Improved financial leverage and enough liquidity to meet any urgent servicer advance requirements

NRZ’s liquidation of large parts of its investment portfolio during the March market sell-off helped it substantially delever its balance sheet and maintain a high level of liquidity. Its borrowing to asset ratio declined from 85% at the end of 2019 to 71% by Q2 2020. It ended the quarter with a cash balance of over $1 billion which is significantly higher than its historical average of just $400 million. With forbearance rates and unemployment levels at their lowest levels since the peak of coronavirus pandemic in April and significant excess capacity of $2.2 billion available to finance servicer advances whenever they arise, the company now believes that it will only need $350 million - $ 600 million from current cash balances to fund service advances. This provides NRZ with enough cushion to go on the offensive and make opportunistic purchases of assets which are currently mispriced. Also, NRZ recently announced the refinancing of $550 million of senior secured term loan which it raised in March at a substantially high interest rate of 11%. The refinanced term loan carries an interest rate of 6.25% and will result in approximately $30 million of annualized savings and higher core earnings.

Source: NRZ, Supplementary Information

For further perspective, here is a look at the current (and historical) discounted price-to-book valuation for New Residential.

Despite the lower price-to-book on the common shares, there are some questions as to whether to company’s business can achieve the previously high returns on its assets, considering the business has evolved, and the potential return on investments may not be as high as it was (i.e. can residential loans really earn the same level of returns as MSRs?). However, the preferred shares provide another option to consider.

Preferred shares are a lower risk option to play the continuing recovery and tap solid income

One of the best ways to invest in NRZ is through its preference shares. The company has 3 sets of preferred stock outstanding. All of the preferred shares are perpetual and cumulative. And as a result of the broader market sell-off in March 2020, dividend yields on the preferred stocks reached very high levels of over 11%. Since then, the preferreds have shown significant recovery, however, they are still trading at a dividend yield of between 8-9%, which is considerably higher compared to the improved business. At these discounted valuations, we believe that the risk-reward is attractive for long term income-focused investors. Out of the 3, Series C offers the best return potential as it trades at the steepest discount relative to series A and B while offering similar yields.

The company’s quarterly preferred dividend liability amounts to just $14.5 million and the core earnings to preferred dividend coverage ratio stands at 10.7x which is expected to rise further post refinancing of the company’s high cost debt. Also, with the available liquidity of over $1 billion, adds strength to the preferreds. Further, the company has increased the quarterly dividend for its common shareholders recently (twice) which signals additional confidence by the firm and suggest more safetfy for the preferreds as they hold a senior position in the capital structure.

Learn more about the preferred shares here (QuantumOnline).

Risks

Liquidity challenges: Although NRZ has sourced considerable financing to meet servicer advance requirements, a substantial increase in forbearances and delinquencies in the near term may lead to liquidity challenges for the company in the future. Recent trends however point towards some stabilization in forbearances related disruption.

Widening spreads: Although the company has trimmed its Non-Agency MBS and residential mortgage loan investments in the last couple of quarters, they still together constitute 34% of the company’s total net equity investment portfolio. If the spreads widen materially due to market uncertainties, it will result in realized and unrealized losses for the company, which may eventually impact share prices and dividends. Having said that, the Fed has proven very likely to step in anytime the market need liquidity support.

Evolving business: As NRZ’s business continues to evolve over time (i.e. the residential loan business is growing and agency loans are becoming a relatively larger portion versus non-agency), there are some questions as to whether the historically high returns (and dividend yield) can be achieved and sustained. However, considering the dramatically discounted book value (and the fact that the company is surviving the extreme Covid-19 sell-off/liquidity challenge), we believe the business will continue to evolve, grow and kick off high income.

Conclusion

The massive market-wide sell-off in late March (and subsequent liquidation of parts of NRZ’s portfolio at depressed valuations) led to significant equity erosion. However, since then the company has built a substantially improved leverage and balance sheet position. And although some uncertainties remain (around the company’s servicer advance obligations, prepayment rates, and liquidity needs), the preferred shares (trading at a nearly 8.5% dividend yield) offer investors an attractive way to generate income and play the continuing recovery in the mortgage markets. If you cannot get comfortable with the higher risk and volatility of the common shares, New Residential’s preferred shares are worth considering (the series B and C have similar high yields and trade at more widely discounted prices—i.e. more price appreciation potential).

Note: We currently have a small position in NRZ common shares, and may initiate a position in the preferred shares soon.