We currently own this 9.4% yield BlackRock Closed-End Fund (CEF) for its many attractive qualities. We last wrote about the compelling bond CEF opportunity in late March when the markets were falling apart due to covid fears (for example here and here), and as you can see in the following chart, shares have since rebounded strongly. However, we believe the price remains attractive, and in this article we review the compelling qualities and important risks (buying opportunities) to watch. Worth mentioning, despite volatility, it has never stopped paying (or even reduced) its big Monthly dividend payments to investors.

BlackRock Multi-Sector Income Trust (BIT), Yield: 9.4%

For starters, we are talking about the BlackRock Multi-Sector Income Trust. To give you a flavor, this particular CEF owns a variety of bond (fixed income) securities, as you can see in the following chart (it currently holds 1,422 securities).

And as we mentioned, it has never once stopped (or even reduced) its big monthly dividend payments to investors in its entire history (see chart below).

Important to note, the majority of the distribution payments throughout its history have been comprised of income paid by its underlying bond holdings, however it did recently return some investor capital in April - August to maintain the steady distribution to investors.

This is not uncommon for closed-end funds (because investors want and need the steady monthly income payments), and in BIT’s case, it was a relatively small amount, and the return of capital has ceased starting with this month. From an investors standpoint, the return of capital works to reduced you cost basis (so keep that in mind when you sell shares—i.e. capital gains calculations), but overall no harm, no foul. BIT did the right thing.

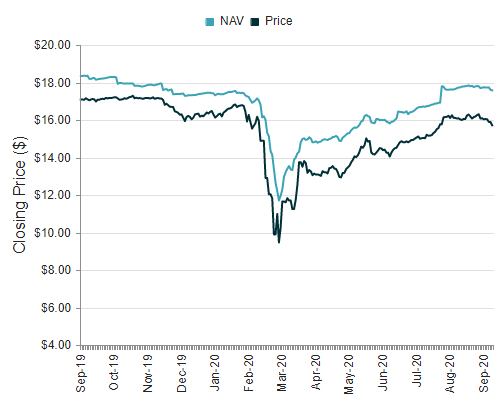

Attractive Discount to NAV

Another attractive quality of this CEF (BIT) is that it trades at an attractive discount to its net asset value, as you can see in the following chart.

On of the unique characteristics of closed-end funds (unlike exchange traded funds or mutual funds) is that they can trade at wide discounts to the actual value of the holdings (this can be a great opportunity for investors). For example, if you add up the value of all of the bonds BIT owns—that equals the NAV. However, the market price of BIT (as you can see in the chart above) is currently about 10.58% below the actual value of what it owns. This means investors in the fund get all the income payments of the underlying holdings at a discounted price (i.e. shares of the fund cost 10.58% less than they’re worth). This is because the price of a CEF is based entirely on supply and demand (buyers and sellers) and fearful sellers have pushed the price below the NAV. There is no guarantee that the price will ever rise back up to the NAV (it could even get wider), but investors are still getting the income payments on sale, something we like!

Also worth mentioning, the negative z-scores in the table above are an indication that the discount to NAV is currently wider than normal, and in this case we view that as quite attractive.

Credit Spreads

Another important consideration for this fund is the health of the fixed income markets, as measured by credits spreads. And as you can see in the following chart, spreads have narrowed significantly since the depths of the pandemic sell off earlier this year, but they still remain slightly elevated (the CCC option-adjusted spread is currently 11.69%).

This is important to understand because as the market panics, credit spreads widen, and individual bond prices fall (mathematically this increases bond yields because investors require a higher yield to compensate for perceived higher risk).

In our view, credit spreads are currently slightly elevated (as we move beyond the coronavirus market lows and head into a volatile election cycle), and this presents an attractive investment opportunity. Things could get worse (i.e. spreads could widen further), but this would likely just create an even more attractive buying opportunity considering the US Fed has taken a “whatever it takes” approach to support the bond markets.

For color, if you don’t know, the main reason bond markets sold off so hard earlier this year was NOT so much because of risk of default, but rather it was due to illiquidity—which created “forced sale” problems for highly levered investors. Since then, the US Fed has expanded its open market purchase activities to include an extraordinarily wide range of fixed income securities—including most of the ones held by BIT—and this dramatically increases the attractiveness of investing in BIT. For more information on this, check out the link in the opening paragraph of this report.

Other Important Considerations

Before investing in BIT (we own shares), there are additional things you should consider. For example, the fund uses borrowed money, currently 35% (i.e. for every $100, the fund invests in roughly $135 worth of bonds). This does increase risks, and it cost money to borrow, but the leverage is generally capped at around 40% (this is very reasonable and relatively very safe) and the borrowing costs are very low (interest rates are extraordinarily low right now, and BlackRock can borrow at a lower rate and with more efficiency than just about anyone else).

Management fees are another consideration, but the current management fee of 0.8% is very reasonable for a fund of this high quality (it’s actually lower than most of its competitors thanks to BlackRocks large scale and commitment to low fess. The total expense ratio (including management fees) rises to 2.89% when you include the cost of borrowing and other operational expenses (this is again very reasonable and actually quite low compared to other popular CEFs such as those managed by competitor PIMCO).

The Bottom Line

We like this fund because of the big steady monthly income payments, attractive price (i.e. discount to NAV and slightly elevated credit spreads) and solid management company (BlackRock has incredible resources, and is a leader in the industry). We also have confidence that the fixed income markets (i.e. this fund currently holds 1,422 bonds diversified across sectors, as shown in our earlier chart) are not going to blow up. Even though we are heading into what could be a volatile election cycle in the US, we have confidence that the companies and government entities issuing the underlying bonds in this fund will be able to support their debts. Furthermore, the “whatever it takes” approach of the US Fed to support the bond markets gives us further confidence still. There is no guarantee that the share price won’t be volatile in the months ahead (if it falls, buy more!), but the big dividend payments have been steady, we expect them to remain steady, and the current prices is considerably attractive too. At the very least, keep BIT on your watchlist. We currently own shares.