This small cap industrial REIT is well positioned to keep benefiting from its high exposure to ecommerce logistics. The dividend is very well-covered, and management remains highly confident. However, its relatively high leverage and exposure to one big risk in particular is important to consider. In this article, we review the business, dividend safety, valuation, and conclude with our opinion on why the company’s biggest risk may actually provide an additional boost to the share price as the economy emerges from the most challenges stages of the global coronavirus pandemic.

Overview:

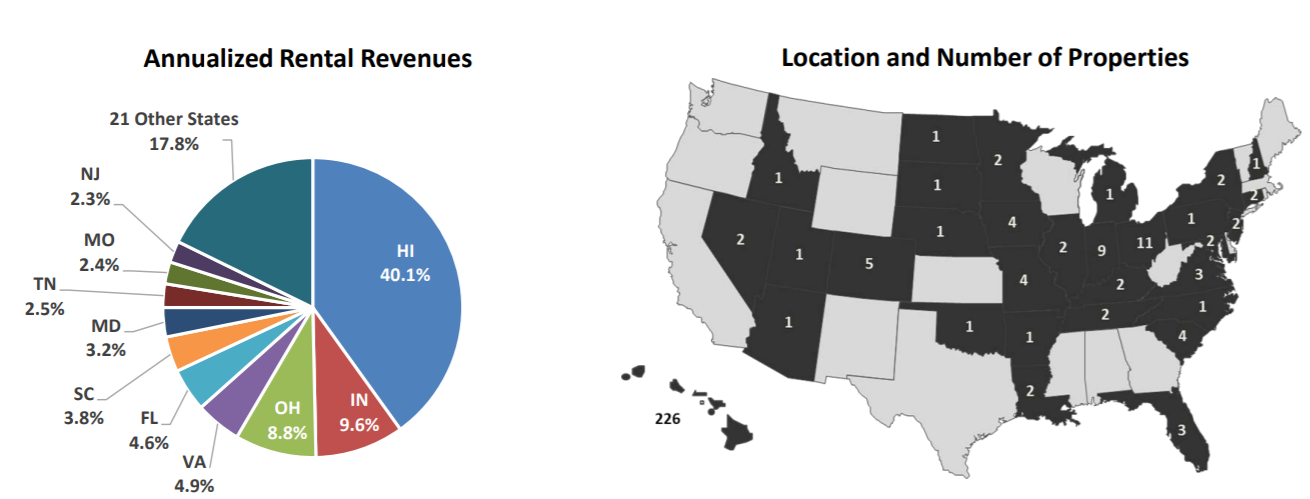

Industrial Logistics Properties Trust (ILPT) is an industrial REIT focusing primarily on logistics, including warehouses and distribution. It owns ~301 industrial and logistics properties with ~43.8 million sq. ft. of rentable area. Of these, ~226 properties are located in Hawaii and the remaining 75 properties are in the continental US. Despite the lower number of properties, the continental US has the larger area (~62% of the total square footage) and accounts for ~60% of total annualized revenue. Notably, a large portion of ILPT’s portfolio has ecommerce exposure with marquee clients such as Amazon—which is a positive as it will provide significant cushion against the ongoing coronavirus backdrop.

ILPT’s tenant base is highly diversified. It has approximately 266 tenants and ~75% of its total annual rent comes from investment-grade tenants. Additionally, 84% of its continental US revenue comes from properties which provide essential goods or services. We believe these defensive characteristics will help safeguard ILPT during the current crisis.

(source: Company Presentation)

As of March 31, 2020, the total portfolio occupancy rate was 98.9%, and the continental US portfolio occupancy was 99.8%. Amazon is the largest tenant accounting for ~16.1% of annualized rent. No other tenant contributes more than 3.7% of its annualized rental revenues. The weighted average remaining lease term is ~9.3 years with only 0.5% of annualized rent expiring over the next 12 months

(source: Company Presentation)

ILPT said that so far its rent has remained relatively unaffected by COVID-19. ILPT noted in its Q1 earnings call that April rent collections remained strong with 19 of top 20 tenants or 95% having paid rent as scheduled. For the one tenant, a rent deferment has been granted. As April 2020, ILPT has granted rent deferrals to 37 tenants, representing ~6.5% of annualized rent. The rent deferral requests are expected to continue throughout May but should subside in Q3 provided the economy continues to reopen this month.

The Hawaii portfolio (~40.1% of rent) is the most impacted by the pandemic given its exposure to tourism. Historical data shows that the Hawaii portfolio has been resilient through previous financial downturns, and ILPT expects the same this time around as well.

E-Commerce Driving Demand

The US retail industry is experiencing a major shift away from malls and shopping centers to e-commerce sales platforms. The trend for online shopping is a secular one and the novel coronavirus (COVID-19) outbreak is likely to boost it further as people are forced to quarantine and order from home. Specifically, there is a higher penetration of new products such as grocery and pantry goods in the e-commerce sector due to the pandemic which boost logistics real estate demand moving forward. E-commerce typically requires up to 3x more space than brick-and-mortar retail businesses require to store inventory. The pandemic is also forcing many companies to reevaluate their supply chain strategy including options to move manufacturing onshore. This will further increase demand for warehouses.

E-commerce sales still represent just a small fraction of total retail sales (~11% as of 2019), thereby providing a large runway for growth. This means high occupancy rates and high rents for the companies that develop and own these properties. ILPT is well positioned here given is exposure to the ecommerce sector.

(source: Company Presentation)

Attractive Growth Prospects

ILPT plans to grow its portfolio via accretive acquisitions. It has acquired over $1 billion of properties since its IPO in January 2018. For example, in February of this year, it acquired an 820,000-square-foot Class A e-commerce distribution facility located near Phoenix for $71.6 million and at a cap rate of 5.2%. The property is 100% leased to Amazon. Some of the earlier acquisitions during 2019 include: 1) An eight property portfolio located in the Indianapolis and Cincinnati markets; 2) A 20 property portfolio located in 12 mainland states and 3) Two multi-tenant properties located in Columbus.

ILPT management continues to look for more opportunistic M&A as evident from its Q1 earnings call.

“We continue to monitor the transaction market and have selectively submitted offers on certain properties during the past month but have not been selected as the buyer, which indicates to us that pricing has not yet changed significantly from pre-pandemic levels.

Even in its most recent 10k filing, it presents a case for growth through acquisitions.

“We intend to grow our business by investing primarily in industrial and logistics properties that serve the growing needs of e-commerce. We believe that e-commerce sales will continue to grow, in both dollar value and as a percentage of total retail sales, and that this will create strong demand for industrial and logistics properties and rental growth for the next several years. We are focused on acquiring industrial and logistics properties that are of strategic importance to our tenants’ businesses, such as build to suit properties, strategic distribution hubs or other properties in which tenants have invested a significant amount of capital.”

Dividend Safety:

Since becoming publicly listed in 2018, ILPT has paid regular quarterly dividends. At the current annualized dividend per share of $1.32, ILPT delivers a dividend yield of 6.4% which is fairly attractive. The payout ratio was ~72% in Q120 which is quite safe in our view. Looking at the quarterly growth figures, we see that normalized FFO per share has grown in mid double-digits over the last four quarters. Assuming similar growth, the payout ratio will improve further. This means even if ILPT experiences reduced payments from some tenants, it has extra cushion to keep paying the dividend.

Valuation:

On Price to Funds from Operations basis (“FFO”), ILPT is trading at ~11.2x 2020 estimates, which is a discount to its peer group average. The lower valuation is due to the market’s perception of higher risks (for example, higher leverage and the Hawaii tourism industry). This higher perceived risk is also reflected in the relatively higher dividend yield as compared to other industrial REITs. ILPT has delivered solid FFO per share growth over the last four quarters and management remains confident they can continue to execute (and the share price and FFO can continue to grow), largely by addressing leverage concerns. In our view, the shares could see a valuation re-rating (a higher share price) particularly as we emerge from the most challenges stages of the coronavirus.

(source: Blue Harbinger Research, Yahoo Finance, Company data)

ILPT Share Price:

Risks:

Tenant bankruptcy: ILPT is exposed to the risk of tenants not being able to meet their rental obligations. Barring exposure to Amazon, ILPT is well diversified with no significant tenant concentration. However, should one or more of these tenants face financial trouble it could lead to future cash flow interruption.

Interest rate risk: The Federal Reserve has cut interest rates to zero and even though we expect interest rates to remain relatively tame, dramatically rising rates could create challenges. As REITs are often seen as an alternative to bonds, higher interest rates could mean decreased demand for REITs, thereby causing a decline in the share price. Also, higher interest rates put downward pressure on earnings as interest costs rise.

Volatility risk: Industrial REITs in particular are more volatile and sensitive to the economy. As such, investors may choose to wait for an opportune time (maybe a big sell-off) to purchase shares (or consider selling out of the money put options to generate upfront premium income, and to give yourself a shot at owning shares at a lower price). Shares of ILPT have rebounded significantly since the big March sell-off, however they remain attractive for income-focused investors at their current price.

Conclusion:

In our view, ILPT’s biggest risk is its high exposure (and leverage) to Hawaii tourism, especially as the global pandemic has squashed demand for non-essential travel. However, ILPT still has very attractive exposure to the industrial logistics space, which is benefiting from the current pandemic (e.g. “stay at home” orders) and as the secular ecommerce trend continues to grow. Further, the dividend is well covered (the payout ratio was recently only 72%) and management remains confident (they also claim the legal structure of the Hawaii leases makes them significantly secure).

We believe the valuation is already low because a lot of risk is baked in, and if/when the world emerges from the pandemic (and into the “new normal”) exposure to Hawaii tourism could prove to be a highly valuable (share price boosting) characteristic. If you are an income-focused investor, we believe ILPT’s 6.4% dividend yield is worth considering.