If it’s simply big steady income payments you seek, this report reviews two fixed-income closed-end-funds (CEFs) that offer attractive yields of 10.5% and 9.1%, respectively. They both pay monthly, and we currently own both. This report shares the important details for you to consider.

The two CEFs we are referring to are:

BlackRock Multi-Sector Income Trust (BIT), Yield: 9.1%

PIMCO Dynamic Credit and Mortgage (PCI), Yield: 10.5%

We last reviewed these two funds together during the depths of the coronavirus crisis in late March, when we described them both by writing Buy! Buy! Buy! We took a lot of flak for taking such a strong view, however the share price of both rebounded dramatically since then as we predicted it would.

We still believe both offer very attractive long-term investment opportunities, and we continue to own both of them. For your review, here are the things you are going to want to consider if you are going to buy (or continue to own) these two high-income CEFs.

What Do They Own?

For the most part, both of these CEF invest in fixed-income (bond) investments. According to BlackRock’s website:

BlackRock Multi-Sector Income Trust’s (BIT) (the 'Trust') primary investment objective is to seek high current income, with a secondary objective of capital appreciation. The Trust seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its assets in loan and debt instruments and other investments with similar economic characteristics.

And according to the PIMCO PCI webpage:

The fund utilizes a dynamic allocation strategy across multiple fixed income sectors, with an emphasis on opportunities in developed and emerging global credit markets, to pursue current income as a primary objective and capital appreciation as a secondary objective.

We encourage you to click on the links provided above to lern more about these funds as the website information is organized helpfully. For example, both funds are well-diversified within their fixed-income markets, and the investments they hold have well laddered maturities, as you can see if you scroll down on the links we provided above. This is important because it helps reduce the risks associated with any one holding within a fund “blowing up” because each position is relatively very small (BIT owns over 1,400 securities and PCI owns a similarly large number of positions).

Market Prices vs Net Asset Values

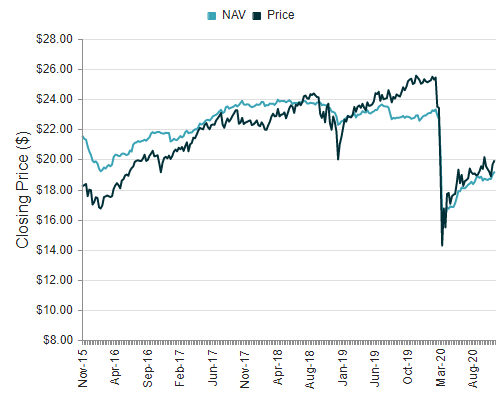

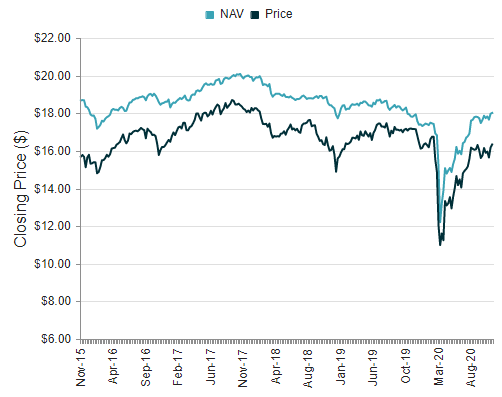

One of the most interesting and important things to consider when investing in a closed-end fund is the current market price versus the fund’s net asset value (NAV is the aggregate value of all the individual underlying holdings). Unlike a mutual fund or an exchange-traded fund, the market price of a closed-end fund can vary significantly from its NAV (because the market price is based on supply and demand, and there is no immediate mechanism to bring the two into alignment as there is with mutual funds and ETFs). Here is a look at the current and historical market prices of BIT and PCI:

PCI NAV vs Price:

BIT NAV vs Price:

We generally prefer to buy and own CEFs that are currently trading at a discount to NAV (as is currently the case for BIT and not PCI) because it means we are getting a chance to buy the assets “on sale,” and because it means we get to buy the income stream they produce (in this case quite high) at a discounted price.

However, there is more to it than simply premium versus discount. For starters, there is no guarantee that discounted price CEFs will ever rise back up to their NAV price (the discount could get bigger), and there is no guarantee that premiums will ever revert either. In fact, in the case of PCI, it trades at a premium (for a variety of reasons we’ll get into in a moment), but the premium is currently a smaller than recent history (and a lot of PIMCO CEFs tend to trade at much higher premiums—which could bode well for PCI).

Another thing worth considering is the price of the underlying holdings versus their par values. Specifically, bonds generally mature at a par value of $100, but BIT’s holdings current have an average price of only around $98 and PCI’s around $88. This can bode well for future price appreciation of the underlying holdings (assuming most of them will mature at their $100 par value, which they almost always do).

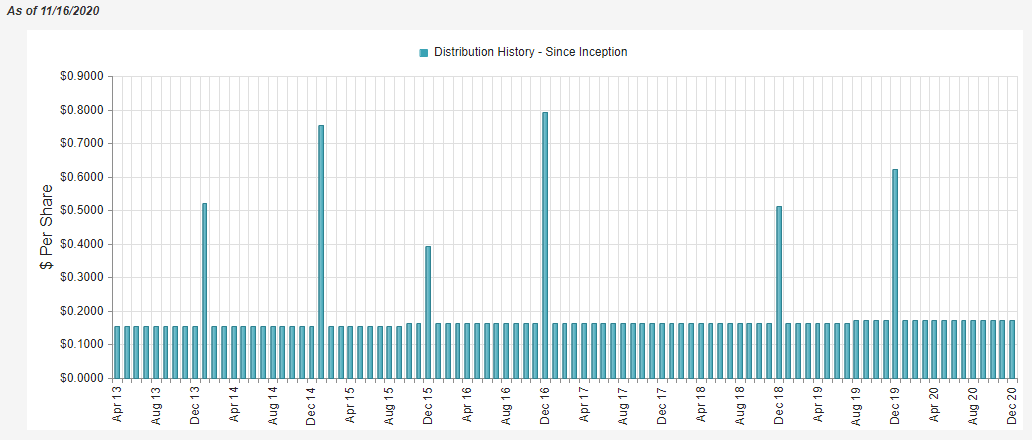

Distribution History: They Both Pay Monthly

If it is steady income payments you seek, you might be happy to know both of these CEFs pay income to investors monthly. And as you can see in the following charts, this income has been steady (even slightly rising):

BIT Monthly Distribution History:

PCI Monthly Distribution History:

You might also not these CEFs do occasionally pay special “extra” dividends, depending on the performance of the underlying asset valuations.

Important to note, both funds aim to pay income based on the income produced by the underlying holdings. But in rare cases they can generate some of those big steady income payments with capital gains and/or a return of your own capital. While many investor prefer to see distributions come from 100% income of the underlying holdings, it is acceptable in our view for some distribution payments to be generated from other sources as described above so long as it is minimal and the overall distribution strategy is sustainable—which we believe it is for both PCI and BIT. Note also that there are slight tax differences in income payments (ordinary income rate) versus long-term short-term capital gains and return of capital (return of capital reduces your cost basis, which can result in more capital gains taxes when you do eventually sell). We are comfortable with the distribution composition for both PCI and BIT.

Leverage (Borrowed Money):

Many CEFs use borrowed money as part of their normal operations. While this can increase risk and volatility, we approve of the leverage in PCI and BIT because they do so prudently, they adhere to regulatory limits, they do so at a lower cost (and with more discipline) that you or I could do, and the leverage helps increase the monthly income payments and total long-term returns. Leverage is concerning to some, but it’s not unlike the leverage corporations use on their balance sheets, homeowners use when they get a mortgage, or the borrowing Warren Buffett does at Berkshire Hathaway. Furthermore, the types of bonds these fund invest in tend to have somewhat lower volatility in the first place, so the leverage is less concerning (and totally normal). As you can see on the webpage links we provided earlier, PCI’s current leverage ratio is around 43% and BIT’s is approximately 35%. For your reference, CEF Connect is another very good resource for CEF information.

Fees and Expenses:

Fees and fund expenses are another important consideration when investing in closed-end-funds. And in the case of fixed income funds that use leverage (such as BIT and PCI), the cost of borrowing money is important to be aware of so you don’t misjudge the fee. For example, PCI charge a management fee of around 2.12% which is normal for PIMCO but on the high side for most CEFs. And when you add in PCI’s 2.0% cost of borrowing, the aggregate expense ration rises to ~4.18%. That is significant, but in the case of PIMCO acceptable considering the strong management team and company resources, plus the firm’s long track record of success. For comparison, BIT’s management fee is less (1.25%) and it’s cost of leverage is also less (only 1.54%—largely because it borrows less). BlackRock is another highly reputable firm with strong resources and a track record of high success. Keep in mind also that the management fees are higher on fixed income funds because it is arguable more “involved” to pick and manage fixed income portfolios than say publicly-traded stock portfolios. Overall, we believe the fees on these two funds are significant but acceptable if you are looking for strong management teams to deliver steady monthly income payments in markets (fixed income) that are much harder for you as an individual (or even professional) to invest in.

Conclusion:

We like both of these funds, and we currently own both of them. And while we believe there is not as much immediate price appreciation potential as there was in late March (the shares have climbed significantly since then as coronavirus fears and fixed income market liquidity risks have reduced), we do believe the big income payments are healthy and will continue.

We also believe these investment are “contrarian” in the sense that BIT trades at an attractive discount to its NAV (you’re buying high income on sale) and PCI’s underlying holdings trade at an attractive discount to their par value (~88 cents on the dollar). If you are a long-term income-focused investor, PCI and BIT are both worth considering for a spot in your portfolio. We own them in ours.