Core Civic (CXW) offers an attractive investment opportunity specially after the recent decline in its share price amid rising political rhetoric against private prisons. CXW’s 10.8% dividend yield is highly compelling for investors seeking steady income. The stock saw a similar sell-off during the 2016 elections, only to bounce back sharply thereafter. And importantly, it has paid big healthy dividends (with little volatility) throughout. We see the stock as deeply undervalued. In the article, we analyze the worst-case scenario (a complete ban on private prisons) and even in that situation CXW stands to benefit. CXW currently offers a compelling entry point, combined with dividend payments that are big, healthy and attractive.

Overview: CoreCivic (CXW)

CoreCivic Inc. is a REIT. It owns and operates private prisons and immigration detention facilities. The company runs 105 facilities totaling over 17 million sq. ft. of real estate including 51 correctional and detention facilities and 27 residential re-entry facilities. Earlier this month, CXW announced the acquisition of a portfolio of 28 properties totaling 445k sq. ft. It operates via the following three segments:

Safety: is the largest segment representing nearly 85% of net operating income (NOI). It comprises 51 correctional and detention facilities with a total design capacity of ~73,000 beds.

Community: this segment accounts for ~10% of NOI. It owns and operates 27 residential re-entry centers with a total capacity of 5,000 beds.

Properties: this segment accounts for ~5% of CXW’s NOI. It consists of 27 properties totaling 2.3 million sq. ft. owned by CXW but leased to third-parties and used by government agencies.

CXW is highly exposed to the political climate and as such the stock price often shows high volatility near elections (importantly, it has continually paid big dividends throughout).

Stock pricing in worst case scenario…

Over the past six months, CXW shares have fallen approximately 30%. This decline has essentially nothing to do with the fundamentals of the business, which remain strong. Rather, investors are fearful of the possibility of a new US government administration (it is an election year) that could take an adverse stance on “private prisons". CXW shares experienced similar volatility during the 2016 election cycle (see chart below). However following the election, the share price sprung back (it rallied almost 80% within three months). This time again discussions on immigration and use of private detention centers are contentious issues in presidential debates (among challengers to the incumbent president). For example, the majority of Democrat candidates have stated their “wish” to outlaw private detention centers and private prisons altogether.

(source: gurufocus.com)

However, CXW Will Benefit Regardless

Even in the worst case scenario, if new contracts with private prisons are banned (or if private prisons are simply banned altogether), existing multi-year contracts do not change, and the actual need for capacity doesn’t just go away. Further still, there isn’t just excess capacity available beyond CXW (there are other providers, such as GEO Group, but there isn’t excess capacity).

As quoted below, CXW CEO Damon Hininger recently noted that even in the worst-case scenario (i.e. private prisons are completely banned), CXW will still gain because there is no alternative excess capacity, and the cost of building from scratch is very high. In which case, government agencies would be forced to either buy (or lease) CXW’s facilities. For example, he gave a brief calculation in the latest Q3 earnings call of what the company’s properties are worth in such a scenario.

“So as you know, we've got about 73,000 beds of capacity in our safety segment; of that about 65,000 is beds that we own outright. So if you take that 65,000 and consider some recent building that the federal or states have done here in the last, let's say probably 4 years or 5 years, at the Federal level, we've seen cost per beds in a range of $200,000 to $400,000 per bed and at the state level, we've seen some building projects in the range of $100,000 to $200,000 a bed.

So look at it this way, if you think about half our business with Federal, half our business with the states, $200,000 per bed probably a good average per bed, if you look at recent building projects within our industry. So you take that $200,000 per bed. It gives the 65,000 beds that we own that gives you an evaluation about $13 billion for our real estate.”

Even in the worst case scenario (i.e. if “private prisons” were banned) CXW still stands to benefit greatly based on need and demand.

Demand from Government Partners Remains Strong

Despite rhetoric-driven volatility in the sector, federal, state and local governments continue to see value in outsourcing to CoreCivic, and have been using CXW solutions at increasing ratec(and there is a strong pipeline of federal and state opportunities). For example, over the last 24 months, CXW has taken in significant new populations in Ohio, Kentucky, Nevada, South Carolina, Vermont, and Wyoming, pursuant to attractive new management contracts. CXW also continues to see demand from US Marshals Service (USMS) and ICE, two agencies that rely on the private sector for a substantial portion of their real estate needs because they do not have their own detention capacity. In 2019, CXW signed two large contracts with US Marshals Service and three large contracts with ICE.

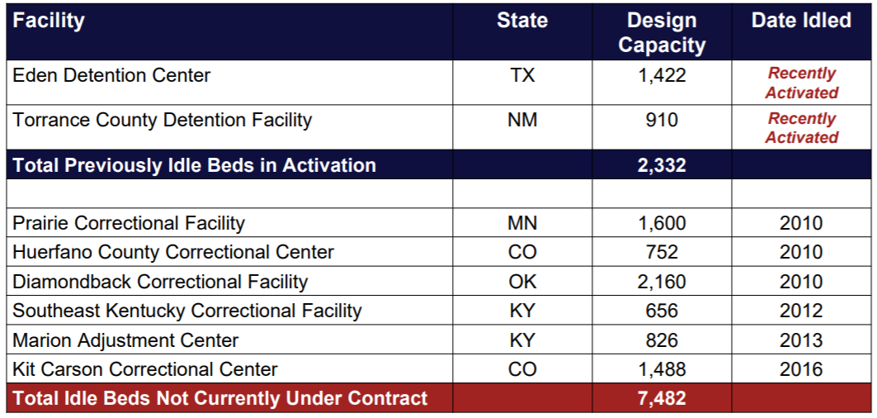

And worth noting, CXW has enough idle capacity available to meet the strong demand with little or no capital deployment required. Specifically, as of Q3, CXW had 6 idle prison and detention facilities including 7,482 beds. CXW noted that utilizing these idle beds will generate up to $0.90 in additional EPS and adjusted AFFO per share.

CXW has the capacity to meet demand:

(Source: Company Presentation)

Mission-Critical Nature and Lack of Alternatives

The mission-critical nature of CXW’s real estate along with a lack of viable alternative infrastructure supports steady demand for CXW. At the state level, CXW estimates that ~$15-$20 billion of infrastructure investments are needed to fix the criminal justice infrastructure. At the federal level, this is even higher as both USMS and ICE outsource nearly 80% and 95% of their requirements to private prisons. The company estimates that the construction of equivalent new government capacity would require Congressional approval and budget of $25+ billion. As such, many states such as California, Alabama, Wisconsin, Vermont, Idaho, Wyoming, Kentucky are exploring private sector solutions to address their criminal justice infrastructure needs. For example, CXW is nearing completion of the Lansing Correctional Facility construction project for Kansas. This 2,432 -bed facility will be operated by the State of Kansas under a 20-year lease agreement and will generate first year rent of ~$15 million. The state of Alabama is following a similar path after having failed for the last 3 years to approve a $1 billion plan to construct new correctional facilities. Now, it is actively pursuing a $900 million, 10,000+ bed procurement with private sector financing from CXW.

Dividend well Covered and Safe

In our view, the strong business fundamentals (as described above) will continue to drive strong cash flow and support the dividend and continued growth. For perspective, in Q3 adjusted FFO (AFFO) per share grew 30% YOY beating CXW’s own expectations. As such, CXW raised its full year FY19 AFFO per share guidance to between $2.59 to $2.63, up from its prior guidance range of $2.53 cents to $2.57. At the midpoint of its 2019 guidance, CXW expects to generate over $300 million of AFFO (AFFO is a proxy for cash flow after maintenance capex, but before dividends). At the current quarterly dividend rate of $0.44 per share, the dividend is annualized to just over $200 million leaving $100 million of residual cash flow. The dividend is well covered with an AFFO payout ratio of 67% meaningfully lower than its guided dividend policy of 80%.

Access to Capital a Key Parameter to Monitor; Sufficient Liquidity Near-Term

Several major banks have announced that they plan to stop lending and providing financial services to the private prison industry. This includes JPMorgan Chase & Co., Bank of America and SunTrust Bank all of which have existing debt obligations with CXW. These lenders plan to follow through on existing debt but will then no longer provide access to capital. This is potentiaoly a significant challenge for CXW given that REITs are reliant on capital to fund growth. As of the near-term, CXW has plenty of liquidity (~$633 million) to help pay off $344 million of debt maturing in 2020. And as seen in the debt schedule below, the majority of debt maturities are due after 2022.

CXW has assured that it will replace exiting lenders with others and is already developing new banking relationships. This is evident from the $250 million debt raise in December 2019 with the help from new partner, Japanese firm Nomura Holdings after Bank of America and other banks refused to participate.

(source: Company Presentation)

Valuation:

Core Civic shares have declined more than 30% since the recent bout of negative political rhetoric against the private prison industry began in roughly June 2019. This is a repeat of the previous election cycle which saw a similar share price decline, only to recover sharply after the election results. We cannot predict the outcome of the upcoming elections in the US; however even in the extremely unlikely worst case scenario (private prisons are immediately banned by the federal government and those prison populations are allowed to flood the streets), CXW is still in good shape because its facilities are so valuable (they’d likely be sold or leased at very high rates to the government in the unlikely situation whereby private prisons were to be immediately banned).

For perspective, Core Civics main publicly-traded peer (The Geo Group (GEO)) currently trade at a price in-line with CXW. Specifically, CXW trades at P/AFFO multiple of 6.3x (factors in political risk), compared to a recent historical multiple of ~10x (i.e. that’s where it has recently traded in recent years) demonstrating a significantly discounted price).

(source: Thomson Reuters)

Further, CXW is experiencing significant growth at the state and federal levels, which should boost earnings going forward. Near-term political headwinds are creating a highly compelling opportunity to buy a healthy 10.8% dividend yield at a deeply discounted price.

Risks:

Political risk: The company’s operations are dependent on government contracts as their primary customer. And with many vocal opponents to private prisons in this years presidential election, the company risks losing business. However, even if the new administration outlaws private prisons, existing multi-year government contracts cannot be canceled. Further, if private prisons are banned, CXW’s properties would still be in high demand as the government would need to buy or lease them at high rates to house the existing population s. We also note, that a during the last election cycle, the shares sold off hard based on fear, only to recover rapidly following the election.

Funding risk: There has been increasing reluctance from major banks to lend money or do any kind of business with companies involved in operating private prisons. For example, major banks including JP Morgan, Bank of America and SunTrust have officially stated that they will no longer provide any funding to CXW. However, given the steady cash flow nature of these businesses, other sources of capital (such as private equity) will quickly flow into place largely eliminating the challenge.

Conclusion:

Political rhetoric has created an attractive buying opportunity as the shares of this big-dividend-paying, steady (and growing) business, have sold off. Even in the worst case scenario, Core Civic’s properties and capabilities will remain in high demand. And in the meantime, the dividend yield is very high, strong and well supported. The discounted share price presents and extremely attractive buying opportunity in this 10.8% dividend yield REIT.