This report is a continuation of our free report title “Top 10 Big Yields Worth Considering.” However this members-only version contains all the detail for the top 5 big yields worth considering. It includes equities, debt, a closed-end fund, and a very attractive preferred stock. All yielding between 6% and 12%, and all trading at very attractively discounted prices.

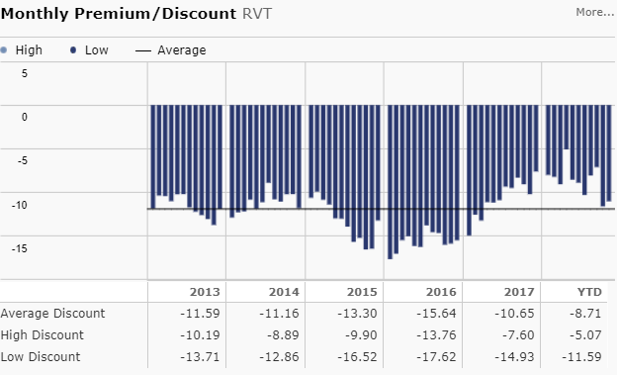

5. Royce Value Trust (RVT), Yield: 8.9%

This big-yield small cap closed-end fund (CEF) is an attractive contrarian bet on top of a contrarian bet due to its large discount to net asset value and because small cap stocks, as a style, are currently out of favor. Specifically, as an equity style, small caps are considered riskier, and not surprisingly they have sold off harder than large caps during this latest market wide sell off over the last three months, as shown in the following chart.

Further still, RVT’s discount versus its NAV has widened, another attractive phenomenon, in our view, as shown in this next chart.

This active fund has a strong management team, a relatively low management fee, and when the rebound eventually comes—this fund will rebound harder than the rest of the market. Plus it pays a big yield. You can read our recent RVT write-up, here…

4. FerrellGas 2020 Bonds, Yield: 11.0%

This is one of the higher risk ideas in this report, but it also has the potential for very attractive returns (we currently own the bonds). In a nutshell, the former management team of this propane company made a bad strategic decision a few years back that the company is still paying for today. And even though we have zero interest in owning this company’s equity, we do like the bonds because of the big yield and attractive price appreciation potential. You can read our full report on these attractive FGP bonds, here…

3. PIMCO Dynamic Credit & Mortgage Income Fund (PCI), Yield: 8.8%

This attractive fixed income closed-end fund is generally more sensitive to credit spreads than interest rates, and as risk and fear have recently gripped the market, credit spreads have widened, and this fund has sold off. Not only is the price more attractive, but it trades at a discount to its net asset value, a rarity for a PIMCO fund. You can read our recent write-up on PCI here…

2. Adams Natural Resources Fund (PEO), Yield: 7.2%

This attractive closed-end fund has been paying distributions for over 80 years! And now is an attractive time to buy. Not only have the shares sold-off as energy prices have, but it now trades at a dramatically wide discount to its net asset value—a very attractive quality, in our view.

This fund invests at least 80% of assets in companies engaged in petroleum or natural resources (or related industries), and at least 25% in the petroleum industry. Not surprisingly, as oil has sold-off, so too has this fund. PEO also has a low management fee, and a strong management team. And before you ask, please note this fund pays out 3 smaller quarterly distributions, and then a larger Q4 distribution. However, it is the large distributions plus large price appreciation potential that we like about PEO. You can read more about this fund at Morningstar, on the PEO webpage, or in our recent write-up here…

1. Teekay Offshore Partners Preferred Series B (TOO.PB), Yield: 12.1%

Teekay Offshore’s high-yield preferred shares have recently sold-off, thereby making them increasingly attractive, in our view. The business and industry are healthier than they were a few years ago, and the backing by Brookfield gives us added confidence. We also appreciate that the market may not be giving the company enough credit for its evolving shuttle tanker business. Further, cash flows have been steady, and are based on multi-year contracts. You can read our recent full write-up on these big-yield preferred shares here…

Conclusion:

At Blue Harbinger, we diversity our investments prudently across various styles. One such style is “big yield” investments, a class in which we like to invest in opportunistically, particularly when the market sells off, and opportunities trade at attractively discounted prices—which is increasingly the case right now. To view all of our current holdings, click here.