Many investors continue to seek attractive high-yield investment opportunities with relatively low risk. This article consolidates and reviews a handful of attractive opportunities for you to consider. These ideas are mainly preferred stocks and a high-yield bond. Without further ado, here are the ideas.

Stag Industrial, Series-C Preferred Stock (STAG-C), Yield: 5.3%

Stag (STAG) is a popular industrial REIT, and if you like the yield on its common stock (currently 5.1%), but you’re not comfortable with the volatility (it’s been a bit of a roller-coaster over the last two years) then you may want to consider Stag’s Series-C preferred shares. They trade at a slightly lower price than the common shares, they offer a slightly higher yield (5.3% versus 5.1%), and the share price is significantly less volatile and much safer.

You can read our full write-up on Stag’s preferred shares (from earlier this week) in this members-only article:

Additionally, you can read our last write-up on Stag’s common shares (from last fall) in this report:

Worth noting, the price on the common shares has risen considerably since that article, but the preferred shares remain attractively priced, in our view.

Sabra Healthcare Series-A Preferred (SBRA-P), Yield: 6.8%

Sabra Health Care REIT (SBRA) owns and invests in healthcare real estate, and we believe the company's preferred shares are attractive. Last month Sabra announced an all stock deal to merge with CCP. The transaction is expected to close in Q3, and it will have multiple diversification benefits. The combined entity will have reduced concentration risks, and it will make the preferred shares even safer in our view. You can read our write-up on the preferred shares from earlier this week here:

PowerShares Variable Rate Preferred Portfolio (VRP), Yield: 4.8%

If you like the higher-yields and lower-volatility of preferred stocks, but your not comfortable with individual stock-specific risks, and you’re afraid that rising interest rates may depress the value of your preferred stock holdings, then you may want to consider the PowerShares Variable Rate Preferred Portfolio (VRP).

This particular ETF solves the stock-specific risk by giving you a diversified portfolio of preferred stocks. Specifically, it holds 111 different securities. Important to note, the majority of the preferred stocks in this portfolio are in the Financial Sector. This creates some sector specific risk for investors, but it still diversified away most of the stock-specific risks. Also, the Financials sector is strong and healthy. For example, all of the big banks just passed the latest round of the Federal Reserve’s stringent stress tests, and all of the big banks had their capital distribution plans (dividend increases and share buyback plans) approved by the Fed as well. Banks use dramatically less leverage than before the financial crisis, and they are dramatically safer than they were before the financial crisis. Plus, the overall economy is strong, and interest rates are expected to rise which will help banks be more profitable (i.e. the net interest margin will increase).

This portfolio also greatly reduces the risks associate with rising interest rates. For example, if you own fixed rate securities, and interest rates rise, then the value of your holdings will fall to mathematically increase the yield to market rates. This is the risk of owning bonds right now, and it poses a risk for preferred stocks too. However, this particular portfolio of preferred stocks have variable interest rates that rise when interest rates rise, and (to a very large extent) this solves the fear of the rising interest rate problem.

Other things to consider about this fund is that it has a decent market value (there is $658 million of investments in the fund) which helps it achieve economies of scale and makes it safely viable. Also, the management fee on the fund is 0.50%. This is a reasonable fee for such a fund, but keep in mind you don’t pay any fee when you own individual preferred shares outright (instead of in a fund). Overall, if you’re looking for big, safe, diversified (across financials) yield that will rise when interest rates rise, this PowerShares Preferred Share ETF is worth considering.

Navios Maritime High-Yield Preferred Shares (NM-G) (NM-H)

Navios Martime High-Yield 2019 Bonds Yield: 14.5%

Navios Maritime Holdings (NM) is a seaborne shipping and logistics company, and it's been dealing with extremely challenging conditions over the last few years. Specifically, the seaborne shipping industry has been dealing with extreme oversupply and low prices. The distress has caused many shipping companies to eliminate their dividends to preserve liquidity (Navios did this), and it has caused many shipping companies to file for bankruptcy (this is not the case for Navios)

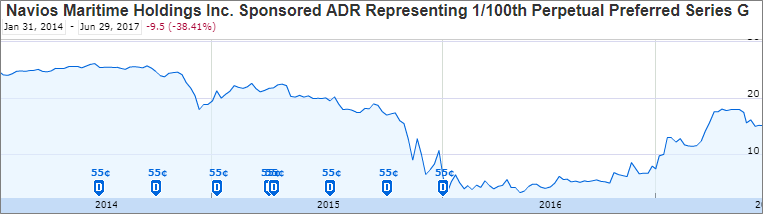

Navios currently offers common shares, preferred shares (Series H and G) and a variety of debt (bonds). Both the common and preferred shares have eliminated their dividend payments to preserve liquidity for higher priority cash needs like continuing operations and debt. However, both the industry and Navios in particular have been perking up and showing signs of improved life lately. Specifically, the following chart shows the price of Navios Series G preferred shares, and the value has been increasing.

Importantly, these are cumulative preferred shares meaning the company must repay the missed dividend payments (unless it files for bankruptcy and there are no assets remaining after reimbursing debt-holders). It also basically means the company must pay up on these missed dividends if it ever wants to issue equity in the public markets again. And the fact that the price has been perking up lately (along with improving macroeconomic conditions) is an indication that the company may actually resume the dividend payments.

However, if these preferred shares still seem too risky--we completely understand. In fact, you can invest more safely (i.e. higher in the capital structure) by owning Navios Bonds. Specifically, we like Navios 2019 Bonds that currently offer a 14.5% yield. You can read our full thesis on why we own these bonds here:

In a nutshell, we believe the bonds will pay in full (i.e. they are “money good”). Specifically, the bonds have not stopped paying their big interest payments, and the price will eventually climb all the way back to par, in our view. If you are an income-focused investor, you may consider investing in Navios preferred shares, but we have acually like the high-yield bonds even more.

Tsakos Energy Navigation Preferred (TNP-E) Yield: 9.2%

Tsakos is a provider of international seaborne crude oil and petroleum product transportation services. As we have mentioned previously, many investors are very afraid of the shipping industry right now, and this fear has created the attractive opportunity in Tsakos. You can read all of the details about why we like Tsakos right now in this members-only report from earlier this week:

In a nutshell, we believe Tsakos has plenty of liquidity to support both its common and preferred shares. In fact, we currently own the common shares (TNP). However, if you cannot stomach the volatility, and you want an even higher yield, the Series-E preferred shares are absolutely worth considering.

And as a reminder, you can view all of our current holdings here: Blue Harbinger Holdings List