Brookfield Property Partners (BPY) offers a big 5.2% dividend yield, and the company may be calling a bottom in the retail REIT market via its bid to acquire GGP Inc (GGP). However, the real winner may be Brookfield’s parent entity Brookfield Asset Management (BAM). This article provides an outlook for retail REITs, a review of the twisted conflicts of interest in this deal, and finally a few ideas on how income-focused investors may want to play this M&A deal and the retail REIT space in general.

Recent REIT Performance (It’s Been Ugly)

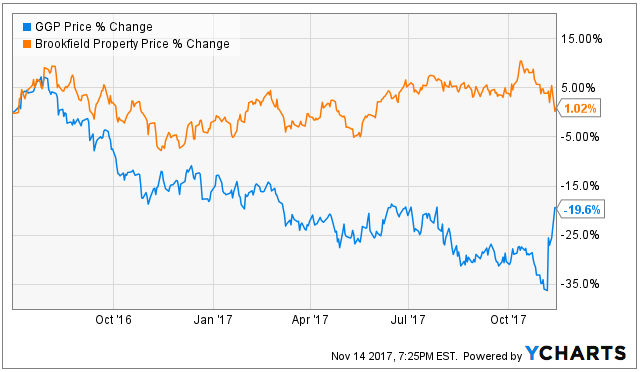

If you are not aware, there’s been a lot of carnage in the retail REIT space, as shown in the following chart.

The negative narrative has been twofold: First, the convenience of online shopping (such as Amazon) has been winning business away from “brick and mortar” stores, thereby negatively impacting the REITs that own them. And second, the “Donald Trump Rally" has favored growth stocks, which have outpaced traditionally safe-have dividend stocks, including many retail REITs. The profitability of many traditional shopping malls has been disrupted significantly.

Why GGP? Why Now?

By way of background, GGP (formerly General Growth Properties) is a $23 billion market cap, S&P 500 company that owns and operates best-in-class retail properties. Brookfield Property Partners (BPY) is a $5.8 billion company that owns, operates and develops a diversified portfolio of real estate assets (including office, retail, multifamily industrial, hospitality, self-storage and student housing). And just last weekend, BPY made a $14.8 billion bid to acquire the 66% of GPP that it doesn’t already own.

Keep in mind, BPY is the listed real estate arm of Brookfield Asset Management (BAM), a $41 billion alternative asset manager that has over $250 billion in assets under management. In fact, according to the BPY’s annual report, BAM recently had an “effective economic interest in our business of approximately 69%.” For reference, BAM’s other listed partnerships include Brookfield Renewable Partners (BEP), Brookfield Infrastructure Partners (BIP), and Brookfield Business Partners (BBU)).

On its website, Brookfield Asset Management describes itself as follows:

“First and foremost, we are value investors with a contrarian point of view. We have learned that some of the best opportunities are found in sectors or regions where capital is scarce.”

Similarly, Brookfield Property Partners describes itself as follows:

“Our objective is to generate attractive long-term returns… by acquiring high quality assets in resilient and dynamic market… and continually recycling capital from stabilized assets at or near peak values into higher-yielding strategies.”

Based on these descriptions, it is in Brookfield’s blood to buy low and sell high. And considering the dramatic selling pressure on retail REITs over the last year (including GGP), it makes perfect sense that Brookfield is interested in GGP. Specifically, with this attempted acquisition, Brookfield is basically proclaiming they believe retail REITs (specifically GGP) are near a market bottom. Further, GGP’s attractive locations fit well Brookfield’s expertise in owning and operating some of the world’s best-known commercial properties (more on this later).

Terms of the Deal:

According to the Wall Street Journal, Brookfield Property Partners has made a $14.8 billion offer (half in cash, half in equity) to acquire share the remaining 66% of GGP shares that it doesn’t already own. GGP investors could choose either cash or 0.9656 of a limited-partnership unit of Brookfield Property for each share, subject to proration that keeps the consideration of cash and units from each exceeding $7.4 billion. There is no guarantee that GGP will agree to the offer, but GGP shares were up significantly last week on reports of this news.

Conflicts of Interest (Follow the Money):

Before considering whether or not this offer price is a good deal for GGP shareholders, it’s helpful to understand the multiple conflicts of interest that exist in the relationship between Brookfield Asset Management, Brookfield Property Partners, and potentially GGP (if the deal goes through).

1. Management Fees Based on Total Capitalization: For starters, BPY pays BAM a management fee based on the total capitalization of BPY. This creates incentive for BAM to grow the capitalization of BPY whether or not it’s in the best interest of BPY shareholders because it increases the fees paid to BAM. According to the risk factors section in BPY’s annual report:

“Our organizational and ownership structure, as well as our contractual arrangements with Brookfield, may create significant conflicts of interest that may be resolved in a manner that is not in the best interests of our company or the best interests of our unitholders.”

More specifically, Brookfield Asset Management may be incentivized “to increase or maintain our company’s total capitalization over the near-term when other actions may be more favorable to our company or our unitholders.”

This is a conflict of interest, and it specifically calls into question BAM’s motivation for acquiring GGP via BPY.

2. Related Party Transactions: Another conflict of interest is related party transactions. Specifically, BPY has a management agreement with service providers that are wholly-owned subsidiaries of Brookfield Asset Management. These service providers are paid fees, determined by BAM, which ultimately benefit BAM.

3. Cash Distribution Policy: Considering BAM recently effectively owned approximately 69% of BPY, BAM receives a significant portion of the distributions paid by BPY (the distribution yield is currently 5.2%). This is a conflict of interest because BAM determines the distribution policy, and there is incentive to keep the distribution high, even if its not in the best interest of all unitholder because a significantly portion of that cash goes directly to BAM. BAM is incentivized to act in its best interest, NOT the best interest of BPY’s other shareholders.

4. Low Ball Offer: There is incentive for BAM (via BPY) to offer a “low-ball” price for GGP. Not only will this help BPY over GGP, but it will also help BAM over BPY. Any money saved with a low-ball offer can be used to pay more distributions (which go mostly to BAM), and it can also result in a higher incentive based management fee paid to BAM by BPY if they can effectively take credit for increasing the value of the acquired assets down the road (remember, the management fee is based on total capitalization and total capitalization growth).

Some analyst believe Brookfield has opened with a low bid price. According to the Wall Street Journal article, “analysts from Boenning & Scattergood said in a research note that a bid would have to be at least $30 a share to be successful, adding that Brookfield’s offer could prompt mall-centered real estate investment trust Simon Property Group Inc. to enter as a counter-bidder.”

Overall, there are multiple conflicts of interest involved with this transaction.

How are BPY and BAM “Spinning” the Deal:

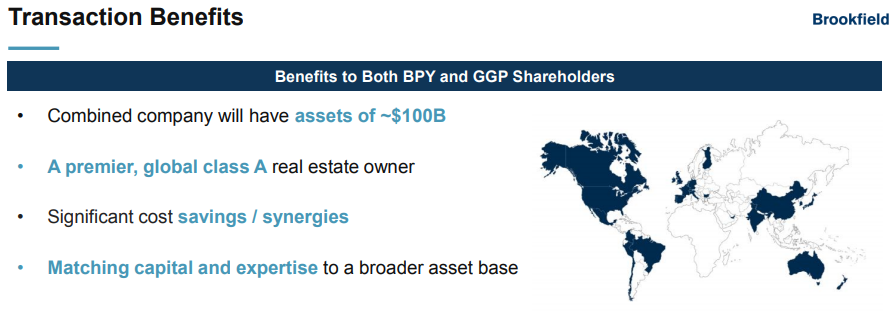

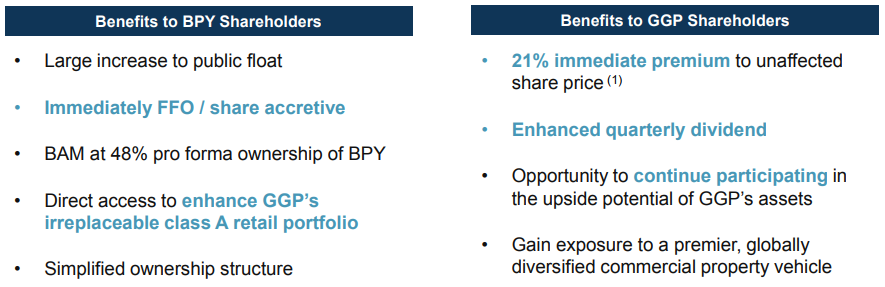

According to Brookfield, this deal will be “dividend accretive” to GGP shareholders immediately (i.e. BPY pays a higher dividend than GGP), it will benefit from synergies and economies of scale, and it will bring new expertise that GGP needs as it transforms its properties to be successful in an evolving retail world. For example, Brookfield has more experience owning and operation the type of experiential properties that GGP will need to transition to in order to be successful.

However, to play “devil’s advocate,” the “dividend accretive” thing may not be in the best interest of shareholders considering the conflicts of interest (i.e. it may be in the best interest of BAM, not BPY or GGP). Regarding the economies of scale, synergies and expertise—there may be some truth to this, but everyone says this every time there is an acquisition, but these benefits often don’t work out as well as expected. And in this case, there are more conflicts of interest than usual, as described above.

Takeaways:

In our view, the fact that BPY and BAM are considering investing in GGP suggests they believe the retail REIT market may be close to a bottom (this is what they do, they buy low and sell high). Further, the fact that BPY and BAM want to help GGP shift towards experiential also says a lot about how they believe the future of retail real estate will play out (i.e. experiential is important). Further still, the fact that they’re pursuing a higher-end REIT (GGP owns prime location properties, not off-the-beaten path properties) also says a lot about how they see the future of retail REITs playing out (i.e. location matters more now than ever).

With regards to GGP, we believe the shares could rise in the short-term if the deal looks likely to go through, if GGP asks for a better deal, or if Simon Property Group (for example) enters the fray and starts a bidding war. However, we could also see GGP fall if the deal gets called off. Based on the volatility, attractive entry points could arise if you are a contrarian income-focused investor. At the very least, it will be interesting to watch how this plays out.

And with regards to BPY, we believe it could be a decent high-income contrarian investment over the next 12-24 months (assuming their acquisition attempt is well-timed and market valuations improve), but we’re leary of BPY as a long-term investment because of the conflicts of interest. Specifically, we realize the Brookfield family is structured to benefit the lower-dividend-paying BAM first, and BPY is just a pawn in that game. If you agree with Brookfield’s notion that retail REITs may be bottoming, but you don’t want to invest in BAM (because the yield is too low—it’s 1.35%) or BPY or GGP (because of the conflicts) then you might consider investing in Whitestone (WSR). Whitestone is a higher-end, prime location, experiential REIT that pays a 7.8% monthly dividend, as we wrote about here:

We don’t own any of these REITs at this time, but we are watching closely, and we’ll post an update if/when we do take a position. All of our current holdings are available here.