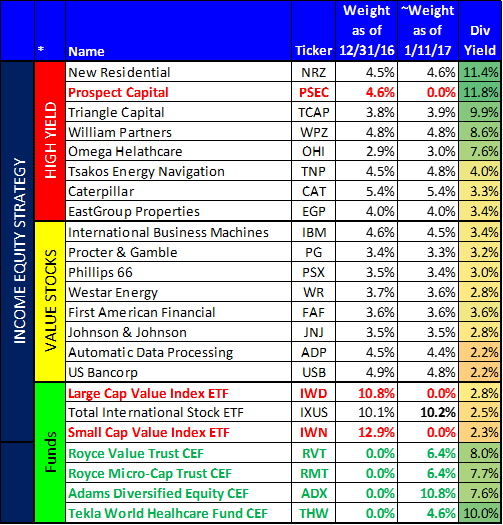

The purpose of this post is to provide an update on several new trades in the Blue Harbinger Income Equity strategy. Specifically, we have added several new attractive closed-end funds (CEFs) that offer very healthy yields. We also sold one of our biggest yielding individual stocks, and we provide a rationale for the sale.

The first series of trades relates to replacing two ETF holdings with three closed-end funds (CEF). These trades result in similar market exposures in terms of style and market capitalization. However, the newly purchased CEFs offer significantly higher yields which is one of the main objectives for the income-focused Blue Harbinger Income Equity strategy.

Bought: Royce Value Trust (RVT)

Bought: Royce Micro-Cap Trust (RMT)

First, we sold our Small Cap value ETF (IWN), and replaced it with two small cap funds: The Royce Value Trust (RVT) and The Royce Micro-Cap Trust (RMT). The main objective of these trades is to maintain similar market exposure with much higher yield. More specifically, the two new funds are small cap (like IWN was) but one of the new funds is slightly core/growth and the other is slightly core/value. In aggregate, they move our portfolio’s small cap exposure more towards the middle of growth/value (instead of more specifically tilted towards value as IWN was). However, we’re very comfortable with the switch from a contrarian standpoint given the very strong performance of small cap value at the end of 2016. Additionally, the two new funds offer other very attractive qualities, in our view, such as their deep discounts to NAV (which provides more upside potential, in our view). Additionally the active management team of the new CEFs add a lot of value for income-investors especially, and the fees are very reasonable for successful, active, small cap funds. Most importantly, these new trades help keep the aggregate yield of our Income Equity portfolio high (i.e. RMT yields 7.7% and RVT yields 8.0%). Full reports on both RMT and RVT are available here…

Bought: Adams Diversified Equity Fund CEF (ADX)

The next ETF to CEF trade is a sell of our Large Cap Value ETF (IWD) and replacing it with a buy of The Adams Diversified Equity Fund CEF (ADX). One of the main goals of this trade is to keep the yield of the Blue Harbinger Income Equity Fund high, so as to meet its objectives and the needs of readers (ADX yields 7.6%). Like our small cap CEF purchases, this large cap CEF purchase shift the style tilt slightly away from value and towards growth, and we’re comfortable with that from a contrarian standpoint given the strong performance of value stocks at the end of 2016. Besides its big 7.6% yield, we also like ADX because of it amazing long-term track record of quality management, and its attractive current discounted price versus its net asset value. We explain in detail why we like ADX in this full report…

Bought: Tekla World HealthCare Fund (THW)

The next trade is slightly more specific in that we purchased shares of the sector specific Tekla World HealthCare Fund (THW). This CEF yields an impressive 10.9%, and we purchased it as a contrarian play on the recently underperforming healthcare sector. The sector has been plagued by uncertainty, which we believe could be about to decline given the soon-to-be aligned White House and Congress. Specifically, the market hates uncertainty (which is why the sector has underperformed), but we may be about to get a big dose of clarity (with regards to the Affordable Care Act, and health care company corporate tax rates, for example) which could result in strong performance for healthcare stocks. We also like this fund because of its attractive discount to NAV, its careful generation of prudent distribution payments with reasonable amounts of leverage, and because it helps keep the yield in our Income Equity strategy high. You can read our full report on The Tekla World HealthCare Fund (THW) here…

Sold: Prospect Capital (PSEC)

Our final trade is that we sold Prospect Capital (PSEC) this morning. This is likely the most controversial trade because many investors love the big 11.8% yield (paid monthly) as well as PSEC’s great performance since February of 2016. However, we are electing to sell for a variety of reasons including valuation, our outlook for the business, and simply from a risk management standpoint.

Regarding valuation, the market may be getting a little too comfortable with PSEC thereby driving its price and valuation higher, and giving it less upside in our view. We purchased PSEC in early May of this year when the price was much lower than it is now, and we are comfortable taking profits now. We don’t necessarily believe a big price decline is imminent, we’d just rather invest our dollars in other opportunities as this time.

Regarding the market outlook for PSEC, it’s a business development company (BDC), and many BDCs trade similarly to high yield debt. And considering high yield debt just had a great year in 2016, we believe the prospects for higher risk investments (the kind that PSEC and high yield debt fund) are less attractive now than they were before. Further, as interest rates rise (the Fed has been raising, and is expected to keep raising) that slows the economy, and the companies that get hit first are the “riskiest” such as the types of companies that PSEC invests in.

Additionally, we sold PSEC for risk management purposes. PSEC was a large position in our Income Equity strategy (especially considering its price appreciation since we bought it), and as contrarians we believe it’s very unlikely for it to experience another run of big price appreciation like it has experienced since we bought it. Again, we don’t believe there is an imminent and dramatic price decline ahead for PSEC, we simply feel more comfortable allocating our investment dollars to other investments at this time.

We are currently working on a full write-up/report on why we sold PSEC, and we expect to have that complete within the next 24-48 hours, however we wanted to share the news (we sold PSEC) with subscribers as soon as possible. In the meantime, here is the new holdings list for the Blue Harbinger Income Equity Fund…