Stop Investing Like It’s 1985

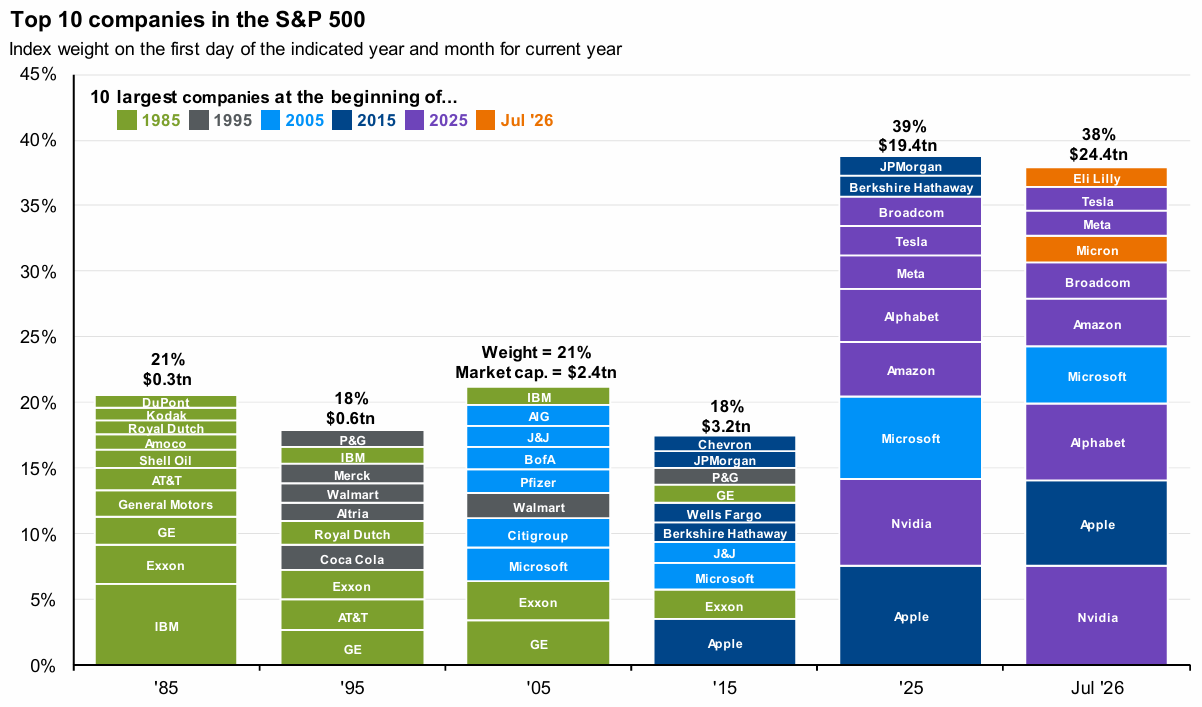

As you can see in the graphic below, the S&P 500 looks very different today than it did in 1985. Specifically, it’s a much more technology-driven market and economy. Shifting from 40+ year old investment strategies (that have been written about ad nauseum in text books over the years) can be hard. But not adjusting your investment strategies and portfolio can be downright painful.

For example, the top 10 S&P 500 companies in 1985 (see image above) involved a lot of physical labor like AT&T (hanging phone lines across the country) and General Motors (a lot of people worked hard on the auto manufacturing assembly lines in motor city). Today, the S&P 500 is increasingly dominated by technology stocks—a reflection of how dramatically the US economy has changed over the years.

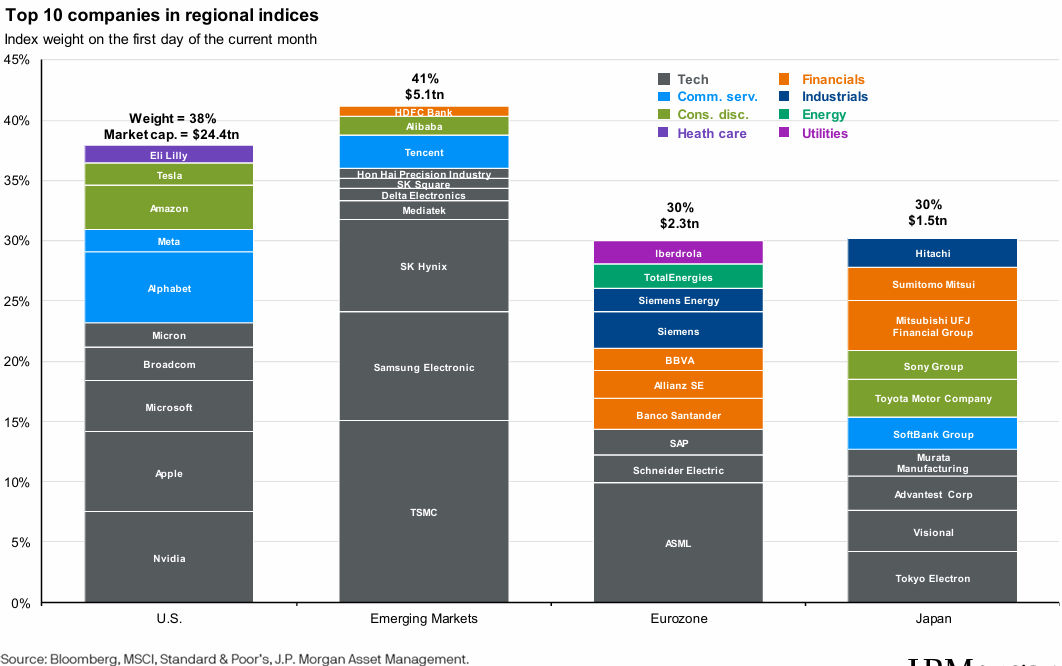

And it’s not only the US, enormous gains have been made for technology companies around the world, as you can see in the following graphic (for example, non-US chip manufacturers like Taiwan semiconductor and Samsung Electronics are major players in the global economy).

Change Is Hard…

…Valuing Tech Stocks Doesn’t Have To Be

The US has certainly faced a lot of growing pains as manufacturing has largely moved outside her borders over the decades, and technology growth has been largely concentrated in certain US geographies (for example, California is the headquarters for many major US tech companies).

But valuing tech stocks using the same price-to-earnings ratio benchmarks as the 1980’s doesn’t make a lot of sense considering tech businesses often have much higher growth rates (and it’s often much easier for technology companies to grow rapidly as compared to the physical manufacturing companies of the 1980’s).

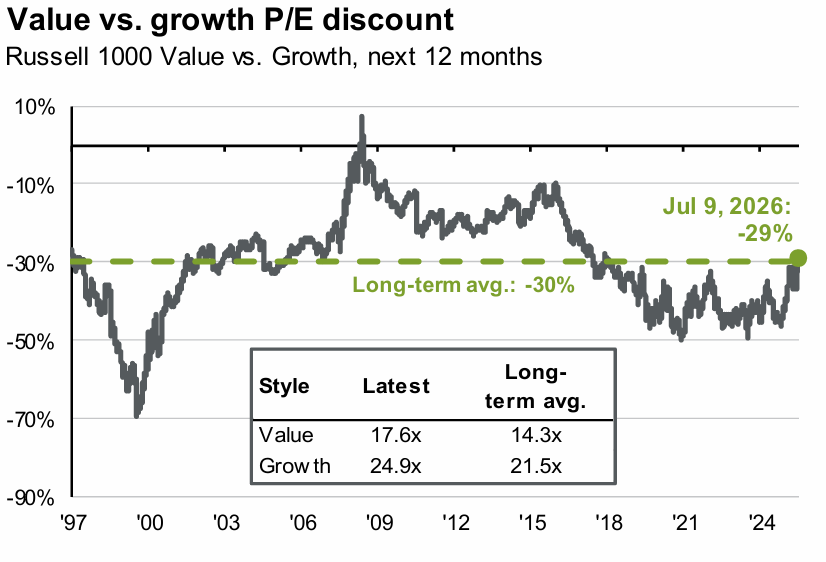

So when investors point to Value stocks as being relatively more attractive than growth stocks simply because they have a lower P/E ratio (see chart above) they’re often overlooking the fundamental differences between today’s tech-driven US economy. More specifically, tech stocks have much higher growth rates, and much bigger market opportunities, than the manufacturing businesses of the 1980’s.

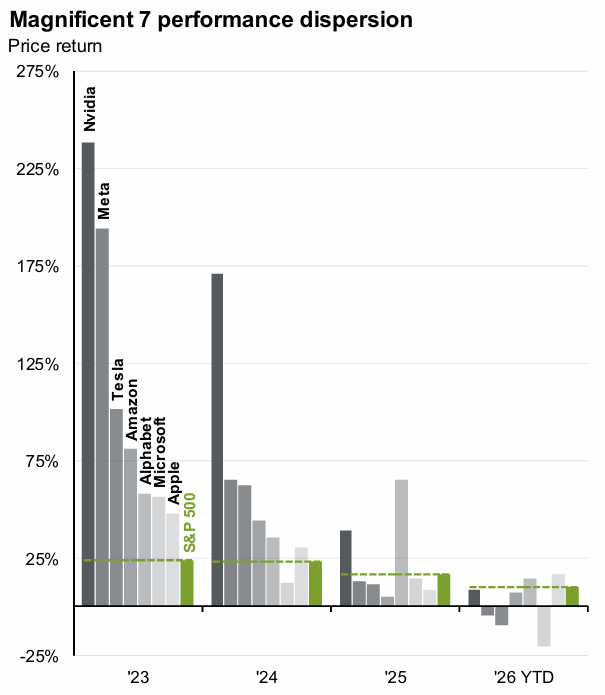

For example, you can see in the chart above that the tech-heavy US magnificent 7 stocks have been outperforming the rest of the S&P 500 for years, but they also have much higher earnings growth rates and thereby higher P/E ratios make sense (i.e. on a growth-adjusted basis, a higher P/E ratio is often better than a lower one—which goes against the simplicity of the market valuation norms of many decades prior).

Large Cap Tech Stocks are Healthy

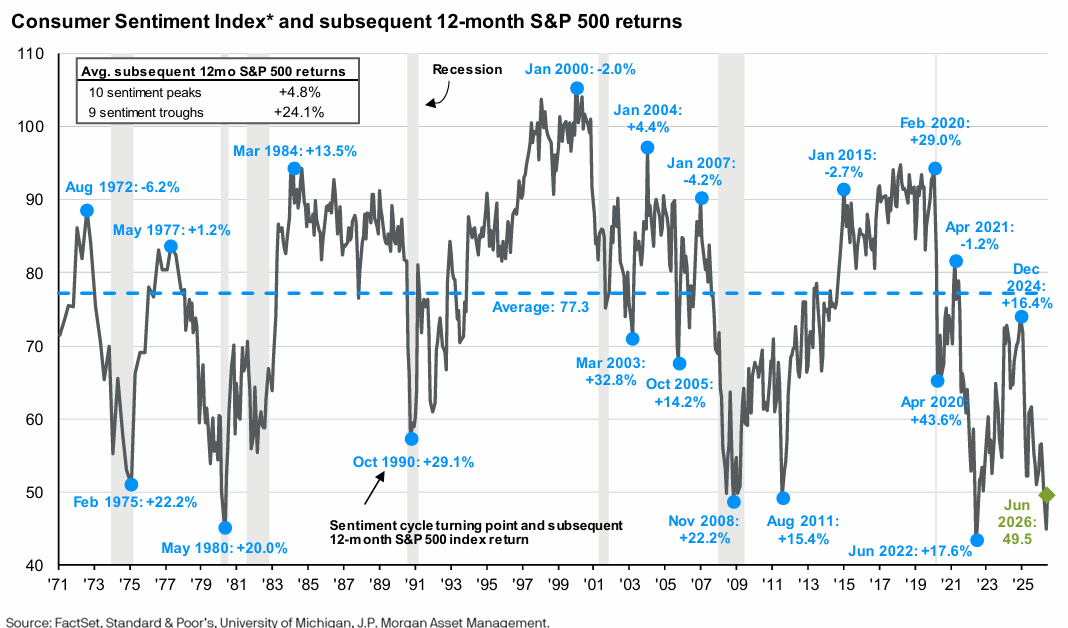

A lot of investors are ready to sell all their tech stocks because they “feel” the market has been to strong and we are due for a major pullback. For example, as you can see in the image below, consumer sentiment is extremely low right now by historical standards.

Yet low consumer sentiment is often the best time to buy (see chart above), and technology stocks look good. For example, despite having continuing strong growth and very reasonable P/E ratios, the tech-driven Mag 7 stocks have underperformed the market averages this year (as you can see in the following table).

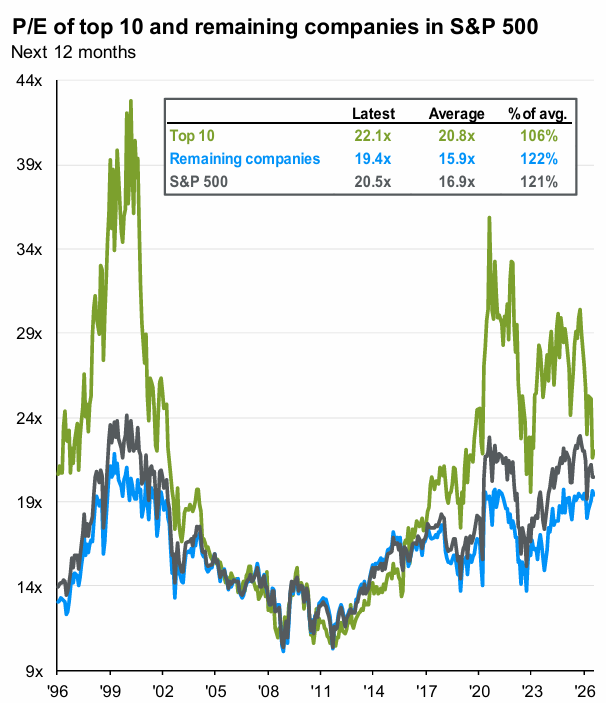

More specifically, you can see in this next chart that the P/E ratios of the top 10 US companies by market cap (which are mainly tech stocks, as we saw in the earlier graphic) have come down significantly on a P/E basis in recent months.

Comfort Stocks

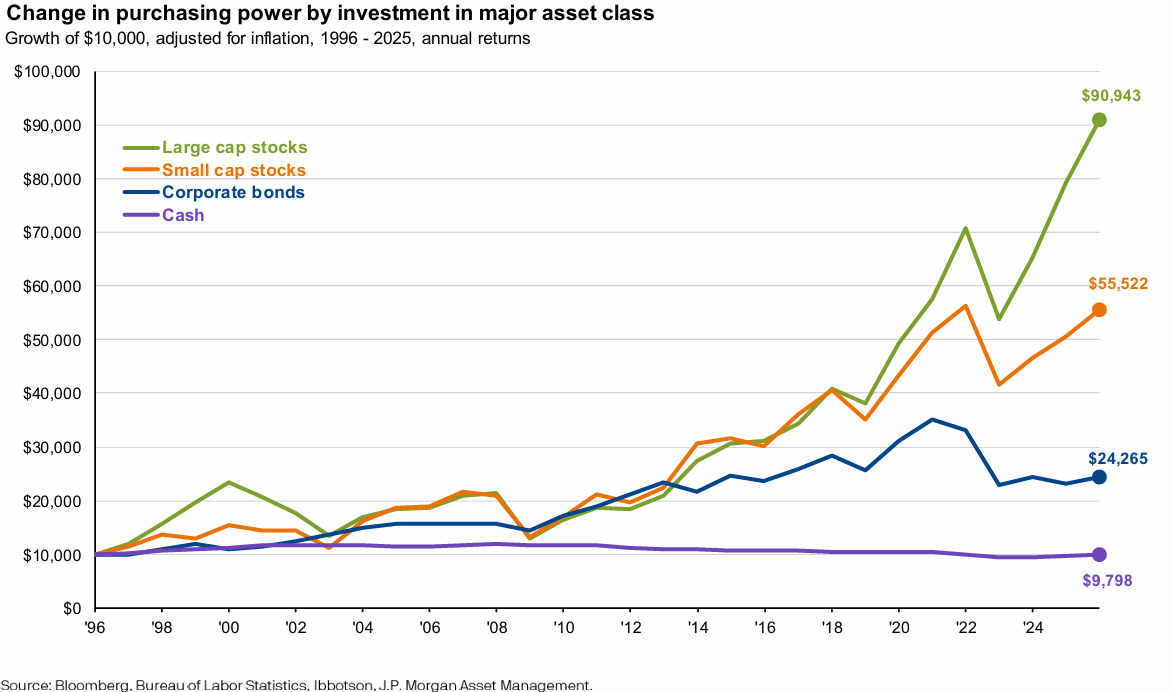

It can “feel” safe to own “value” stocks for their low P/E ratios. It can even feel really good to hold more cash (instead of stocks). But as you can see in this next chart, being too comfortable can cost you a lot of money over the years. A lot!

That’s not to say there is anything wrong with holding cash instead of investing in stocks (a little cash can create a safety net and/or be set aside for near-term expenses). And even bonds (instead of stocks) are starting to make a lot more sense for some people as yields have come up and stabilized (after a historically bad 2021 for bonds as the fed hiked rates at an unprecedented rate to fight the very inflation they created by lowering them so fast right after covid hit).

But if you are going to own stocks, it’s probably a good idea to own a healthy dose of large cap tech stocks, despite the constant fear mongering we hear about another tech bubble forming similar to the one at the turn of the century (which burst hard from 2000-2004).

Today’s growth stocks are much more profitable, have much more durable growth, and have attractive market opportunities to continue to grow into, such as the AI megatrend.

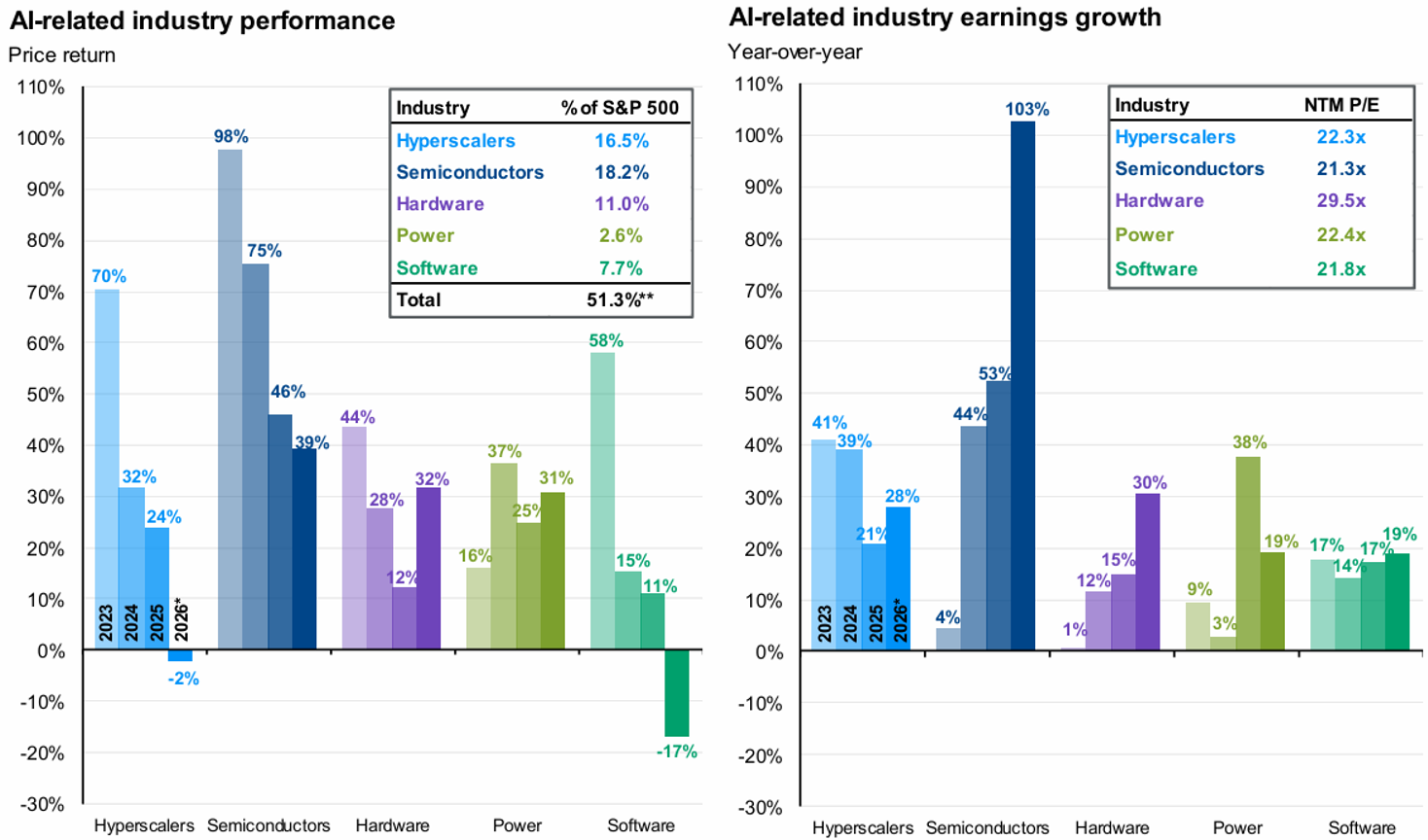

For example, you can see in the graphic above that AI earnings continues to grow, despite a pullback in share prices for some US megacap hyperscalers and software stocks, for instance.

The Bottom Line

If you are buying US manufacturing stocks with low price-to-earnings ratios because that’s what worked well in 1985—you need to reconsider. The US economy is now technology-driven and that is where the growth is concentrated. And you need growth to keep ahead of inflation (the government seems unlikely to reign in its spending).

Owning value stocks, or even bonds and a little cash, is fine. But if you are systematically omitting large cap growth stocks—you might want to reconsider. It’s not 1985.