Adobe Stock: Obliterated by AI

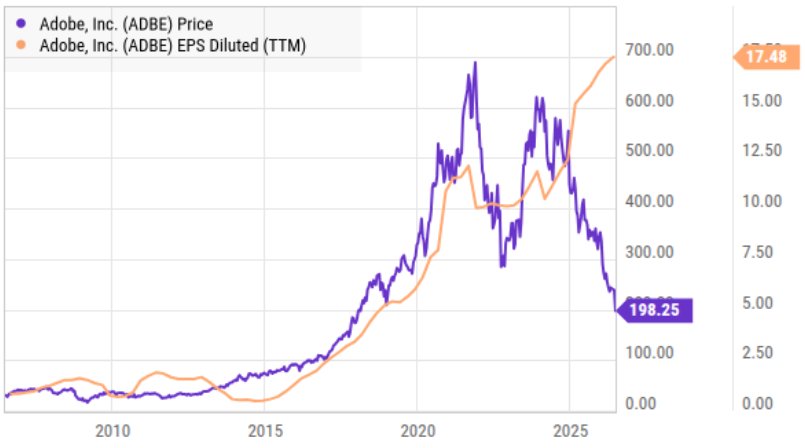

Adobe shares are down 70% since January 2024. The once beloved, recurring-revenue, software darling has experienced dramatic valuation multiple compression as investors realize not much is going to stop the runaway disruption of AI. But how much multiple compression is warranted? Or is Adobe simply on a slow path to extinction? This report reviews Adobe’s business, the impacts of AI, the current valuation (forward earnings “expectations” now cover the cost of a share in under 8 years), the risks, and then concludes with my strong opinion on investing.

About Adobe

Adobe is largely a subscription-based software company that provides creative and digital marketing tools, such as:

Creative Cloud: Adobe Photoshop, Adobe Illustrator, Adobe Premiere Pro, Adobe After Effects, Adobe Lightroom, Adobe InDesign and Adobe Express).

Adobe Acrobat (and Document Cloud). This is Adobe's PDF and document-management business (including Acrobat Pro, Acrobat Standard, Acrobat AI Assistant, and E-signature services).

Adobe Experience Platform (and Digital Experience subscriptions): These are enterprise subscriptions sold to large companies and marketing organizations (including Adobe Experience Platform, Adobe Experience Manager, Analytics products, Journey orchestration tools, and “GenStudio” offerings).

In fiscal year 2025, Adobe broke down its subscription revenue into two parts: $16.3B from its “Customer Group” and $6.5B from its “Business Professionals & Consumers” group.

AI Impacts on Adobe’s Business

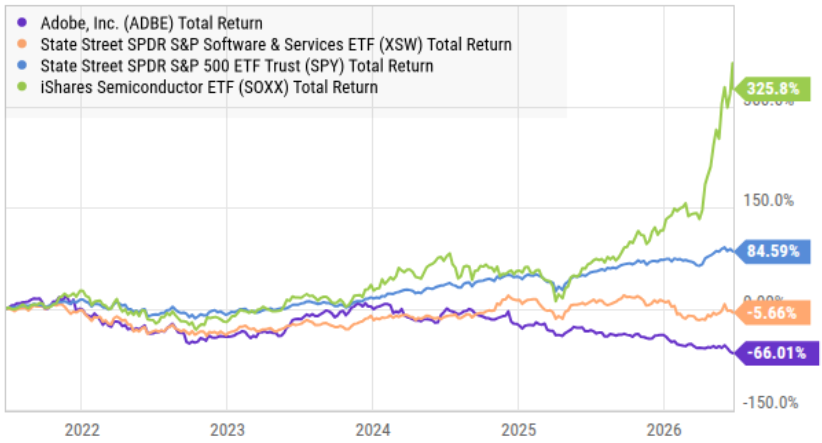

As you can see in the chart below, the market’s reaction to AI has been mostly negative for Adobe (purple line), as investment dollars have shifted away from software stocks in general (orange line, (XSW)), and into more pureplay AI stocks (for example, the semiconductor industry (SOXX)—which powers the high compute demands of AI—is up big (see green line)).

However in reality, AI’s impact on Adobe’s business has been both positive and negative (see examples below).

On the positive side, Adobe is embracing and integrating AI throughout its product ecosystem. For example, Adobe launched Firefly (a family of AI tools) and added AI capabilities to Photoshop, Illustrator, Premiere Pro, Acrobat, and other products. These features can make users more productive (by automating repetitive tasks and accelerating content creation) and also allow Adobe to introduce premium features and usage-based pricing, creating new monetization opportunities.

Further, Adobe’s emphasis on “commercially safe,” licensed training data provides a competitive advantage (considering enterprise customers have been concerned about copyright and potential legal risks of AI).

And further still, AI may even expand Adobe’s total addressable market (“TAM”). For example, many creative tools historically required significant technical expertise, but AI may lower the barrier to entry (thereby enabling more users to create content and potentially increasing demand for Adobe’s ecosystem—a good thing!).

On the negative side, however, AI also introduces serious threats. The most significant is that AI reduces the value of traditional creative software by making content creation much easier. Competing platforms can now generate images, videos, and marketing content with minimal user expertise. And if content creation becomes increasingly automated, some users may no longer need the full capabilities of Adobe’s professional tools.

Also, AI basically creates a whole new wave of less expensive competitors for Adobe—considering the barriers to entry are now lower.

AI Strikes Fear in the Software Industry

As we saw in the earlier chart, the rise of AI has shaken software investor confidence (i.e. software stocks are down big, while pureplay AI stocks are up big). You can see this more precisely in the following software stocks table (lots of companies are down big, while the S&P 500 is up).

Basically, investors increasingly fear the commoditization of software by AI, and thereby reducing pricing power and barriers to entry (that had previously benefited software companies like Adobe for many years). Businesses that once commanded premium valuation multiples have seen those valuations compress significantly (as will be discussed in the valuation section of this report).

Adobe has become one of the most visible examples of this phenomenon; despite continued business growth, its stock has significantly underperformed expectations because investors fear AI.

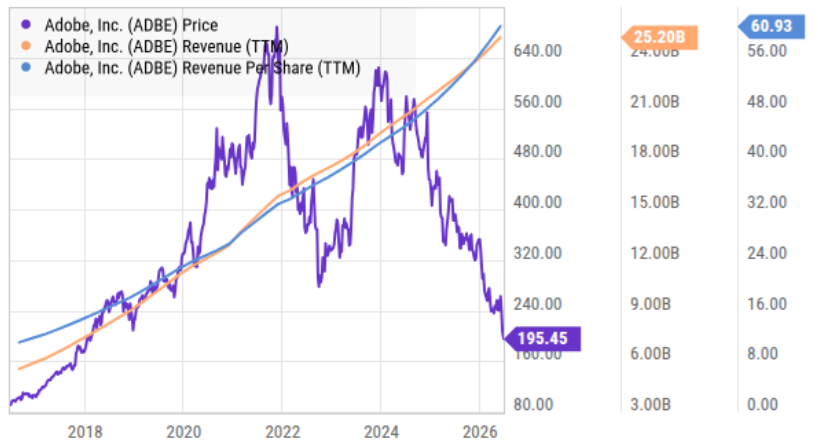

Adobe’s Growth

Despite investor concerns, Adobe continues to grow. Revenue has steadily increased, subscription revenue remains strong, and the company continues to generate substantial free cash flow.

More specifically, Creative Cloud remains a powerful franchise (with millions of subscribers worldwide) and Acrobat and Document Cloud continue to expand (as organizations increasingly rely on digital documents and workflow automation). Further, the Digital Experience segment also remains an important growth driver (basically helping enterprises manage customer interactions and marketing campaigns).

In a nutshell, Adobe has continued to grow (revenue and earnings) in recent years, while also maintaining strong and increasing profitability (see gross and net margins in the earlier table) while also continuing to invest heavily in innovation and AI. Typically, these are all very good things—but the valuation tells another story (see below).

Valuation

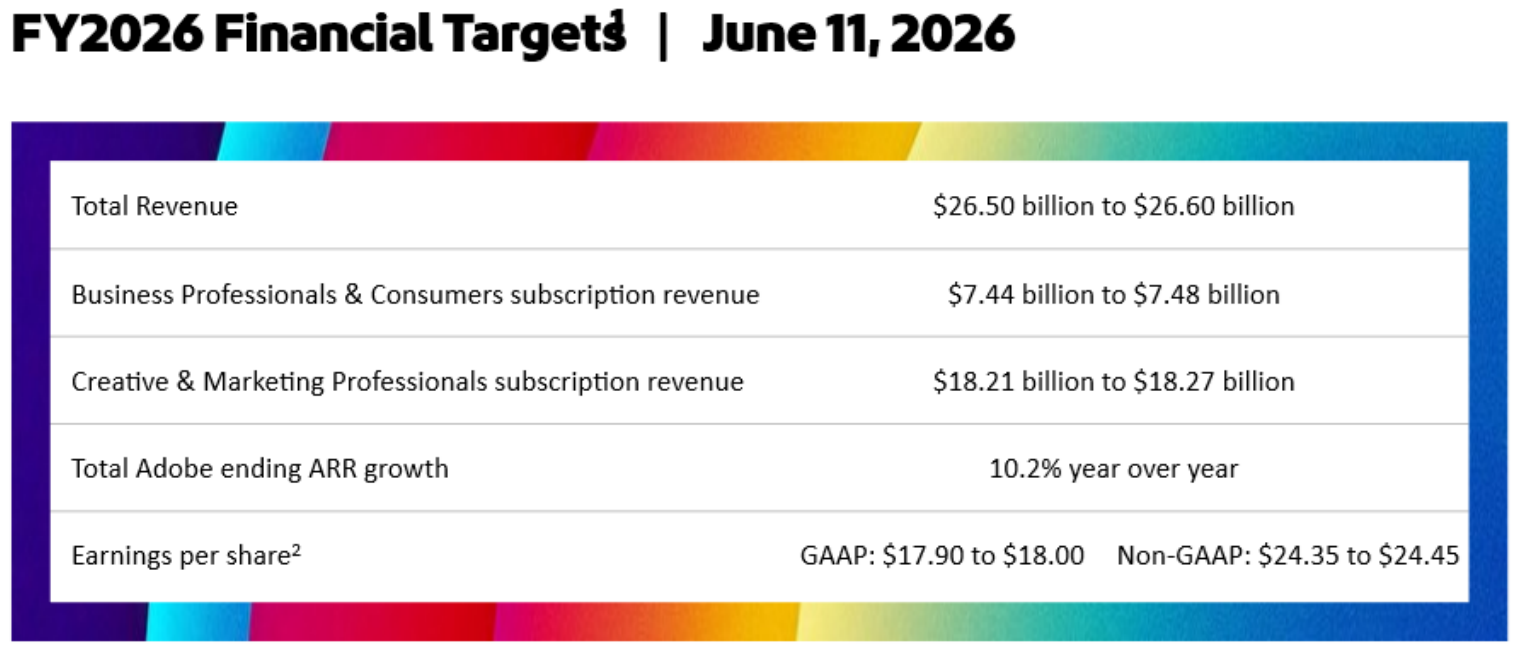

As you can see in the graphic above, Adobe is targeting earnings per share (non-GAAP) of around $24.40—which compares favorably to the current share price of just $195. In fact, that means it would take just under 8 years for Adobe’s net income to cover the cost of a share—and that’s assuming it doesn’t continue to grow. In reality, the company continues to grow at or around 10% per year (see earlier table). In plain English—Adobe shares are really cheap. Yet unlike just about every other business in the world—when stock shares go on sale—people run and hide!?

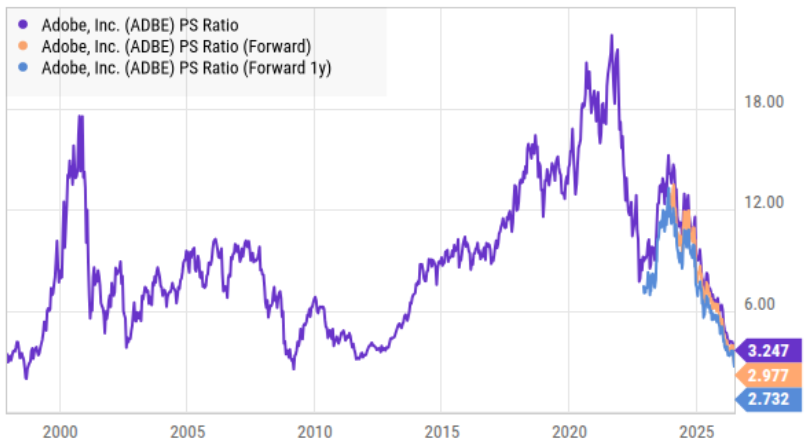

For a little more perspective, you can see in the chart above that Adobe’s price-to-sales ratios have plummeted, despite its very high net profit margin and high earnings growth trajectory. In fact, it now trades at a forward PEG ratio (price-earnings to growth) of less than one (currently 0.6x, see earlier table). Unless Wall Street is wrong (which they can be) and Adobe’s revenues and profits start to decline really fast (again, they’re both currently growing)—these shares are an absolute steal at this price.

Major Risks

The largest risk facing Adobe is AI-driven disruption. Or as the current valuation suggests—AI related “extinction” (in less than 8 years). If AI ultimately replaces—rather than complements—Adobe is in trouble. However, the reality is Adobe is incorporating AI into every major product it sells.

Another risk is increased competition from AI-native companies that may offer lower-cost alternatives. Fortunately however, Adobe has the advantage of a large customer base (a competitive advantage new competitors don’t have) that allow it to quickly understand and deploy opportunities within its ecosystem. Nonetheless, Adobe faces execution risks—as it attempts to balance innovation within its existing businesses.

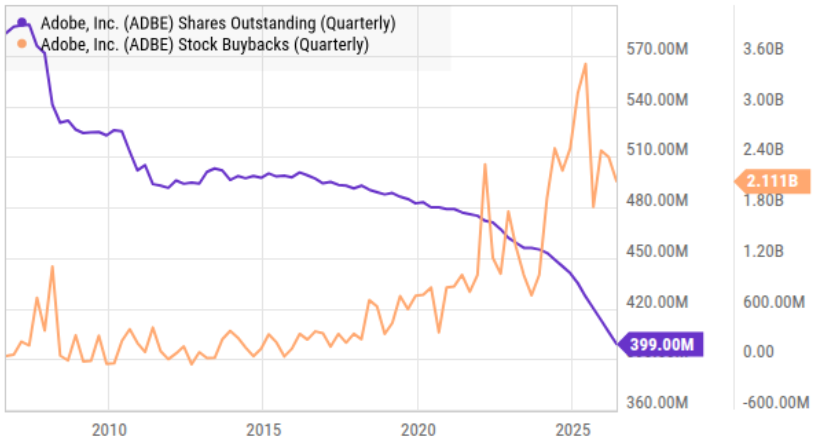

Capital allocation presents another concern. In hindsight, some of Adobe’s share repurchases in 2021—2022 were poorly timed, occurring when the stock traded at historically elevated valuations. Adobe spent billions repurchasing shares before the stock subsequently declined substantially.

Finally, slowing economic growth (or reduced corporate spending) could negatively affect subscription growth and enterprise demand. However, Adobe’s subscription model (and very high profit margin) does help it weather (financially) economic cycle storms better than most.

The Bottom Line

AI has software investors spooked. Especially as once dominant industry darlings (such as Adobe)—who previously commanded rich valuation multiples (before AI, SaaS companies were the “it” stocks for many investors)—have fallen back to earth (valuations are no longer “rich,” they are now downright “cheap”).

The question is whether software companies will fail to evolve in a world disrupted by AI. My guess is that Adobe (with it’s healthy subscription revenue and strong financial position) will continue to evolve to meet industry challenges (it just won’t be achieving the same insane high growth numbers as certain semiconductor stocks—which is totally fine, all things considered). And Adobe won’t being going totally extinct in less than 8 years (as its P/E ratio suggests).

As an investor, you’d be crazy to not at least consider investing in the AI megatrend (the AI train continues to have a lot of room to run), but rather than pouring 100% of your wealth into pureplay AI stocks (which are the “it” stocks now), it can make a lot of sense to diversify into a few deeply discounted, high-profit-margin, growth stocks, such as Adobe. Because when money starts flowing out of pureplay AI stocks (even small changes in growth expectations can cause big declines in pureplay AI growth stocks), you are going to want to have some of your money invested somewhere else. And if you are looking for attractive contrarian opportunities, Adobe shares are absolutely worth considering.