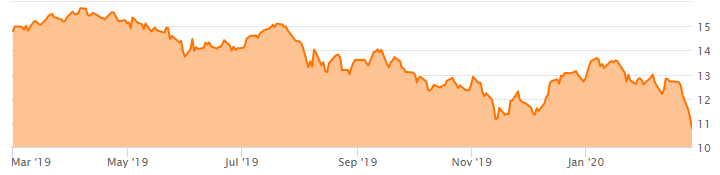

Just last week, the S&P 500 was trading at 19 times forward earnings, its highest level since 2002. And considering the bull market began almost 11 years ago, it seemed plausible we were due for a pull back (i.e. the usual drumbeat of fear mongering media pundits was increasingly sounding credible). It was as if the market was looking for a reason to sell off, and it seems to have found it in the growing coronavirus concerns (for example, Microsoft just warned it will miss guidance because of coronavirus impacts). And as you can see in the following chart, the sell off has been ugly.

And as investors take note of their declining account balances, they’re often gripped by two all-too-common notions: One, should I sell everything and head for the hills? Or two, should I start greedily buying this dip as others are so fearful? In our view, the answer to these questions is more nuanced. Specifically, it’s okay to be a little bit opportunistic here, but for goodness sake—don’t lose sight of your long-term investment goals.

For example, if you’ve had a little extra cash in your account that you’ve been meaning to invest—now is a better time to buy than just last week simply by virtue of the fact that prices are lower. But it you are an income-focused investor, that doesn’t mean go dumping 100% of your nest egg into volatile zero-dividend growth stocks just because you think we’re due for a rebound. That’s crazy. Rather, disciplined, goal-focused long-term investing has proven to be a winning strategy over and over again throughout history

Unfortunately, it’s volatile times like these when investors make trading mistakes. It’s almost as if the sensationalized fear-mongering media punditry encourages panic and bad decisions. Investors need to remember that the media is not acting in your best interest. Again, it’s okay to be a little bit opportunistic in the market here, but don’t lose sight of your long-term goals.

In that vein, we are sharing 100 big-dividend stocks that have sold off hard over the last week. And then 10 stocks in particular from the list that we find particularly attractive from an opportunistic standpoint, so long as they fit with your personal long-term investment plan and objectives.

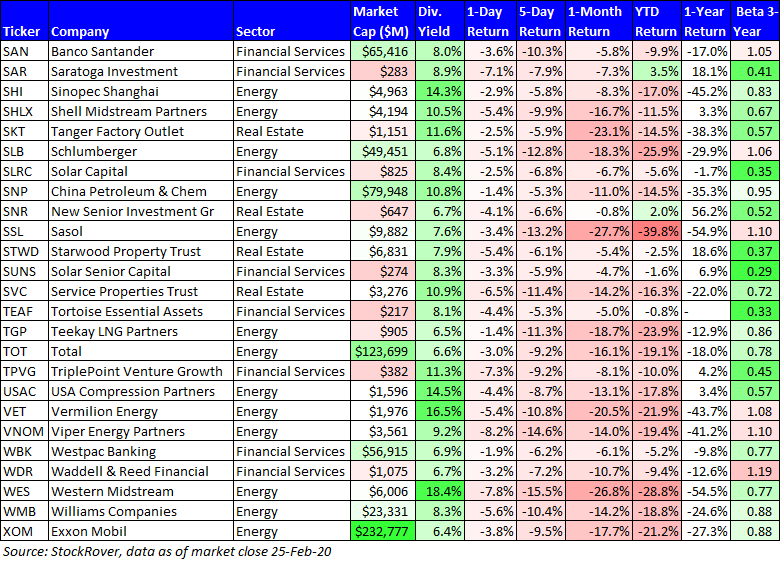

100 Big-Dividend Stocks Down Big This Week:

Top 10 Big Dividend Stocks Worth Considering

From the list of 100+, we have selected 10 that are particularly attractive and worth considering if you are an income-focused investor…

10. EPR Properties (EPR), Yield: 7.2%

EPR Properties (EPR) is a triple-net lease specialty REIT focusing on experiential real estate (including property types such as theaters, eat and play, ski, attractions, experiential lodging, gaming, fitness and wellness, cultural and live venues). We wrote about EPR in great detail just two months ago, whereby we concluded it was starting to get attractive as the share price had declined somewhat. However, the share price has since fallen significantly lower and the yield has mathematically risen dramatically.

EPR announced earnings earlier this week whereby they met FFO expectations but issued conservative guidance. And between that announcement and the market wide sell off, EPR shares have fallen hard, despite the healthy businesses. If you are looking to opportunistically add shares to your portfolio (in a manner consistent with your long-term goals), EPR is worth considering.

9. Enterprise Products Partners (EPD), Yield: 7.5%

Enterprise Products Partners is a best-in-class American oil and natural gas midstream service provider. As we recently wrote in great detail, It was attractive two weeks ago when it offered a yield of 6.8%. However, as the market has sold off, the yield has mathematically risen to 7.5% (as price falls, yield goes up), and the business remains attractive

Specifically, its fee based operating income (85% of mix) adds significant stability to cash flows. Also EPD’s planned capital expenditures will lead to growth in volumes, cash flows and distributions in the near to medium term. Further still, given the stability and growth profile of the cash flows, the distribution yield of now 7.5% is highly attractive.

8. Main Street Capital (MAIN), Yield: 6.3%

Main Street Capital is an internally-managed business development company (BDC). Its main business is to provide debt and equity capital to middle market and lower middle market companies. Main Street has a long-history of managing a healthy well-diversified investment portfolio, as well as paying steady big dividends to investors. Because of the attractiveness of the business, it consistently trades at a higher price-to-book valuation than almost all of its BDC peers, and this is one of the most common investor concerns (i.e. I like the business, but the valuation is already so rich).

Recently, Main Street shares have sold off particularly hard thereby affording investors a little margin of safety for some opportunistic buying, if they are so inclined. We wrote our last full report on Main Street in the second half of 2019 (and you can view that report here), but the main takeaway was:

“Main Street Capital is an attractive internally managed BDC… Its dividend is safe and growing, and its debt plus equity strategy has allowed higher returns for investors and provides further justification for its price-to-book ratio. Over the long-term, we expect MAIN to continue to outperform most of its peers while continuing to pay high quality growing dividends.”

Since that report, Main Street’s healthy business has continued to post strong net investment income, and just this Wednesday announced more steady monthly dividends for April, May and June. If you are looking to opportunistically deploy a little capital (in a manner that is consistent with your own personal investment strategy) Main Street is worth considering, especially after the recent indiscriminate market wide sell off.

7. Exxon Mobil (XOM), Yield: 6.4%

Exxon Mobil is a hated stock for a variety of reasons, including the fact that lower energy prices have delivered a hit to cash flows, as well as the fact that the coronavirus may deliver a hit to global demand, and the immense selling pressure by the continuing massive wave of fossil fuel divestment by large asset owners (e.g. pension plans).

The good news (for Exxon Mobil investors) is that demand is not going away for decades (alternative energy sources can’t yet compete economically), and the business enjoys a very healthy balance sheet and vast economies of scale versus other smaller energy industry peers. We recently completed a full report on Exxon Mobile (which is available here), and concluded that report by explaining:

“Exxon Mobil is one of the best options in the energy sector for investors seeking big healthy growing dividend payments and attractive price appreciation potential. We believe a variety of factors… have combined to create this attractive buying opportunity… Overall, the negative narrative and very weak performance of the Energy Sector… have created some very attractive big-dividend buying opportunities, including Exxon Mobil.”

If you are looking for a big steady dividend that has recently sold off hard, Exxon Mobil is absolutely worth considering.

6. Ares Capital (ARCC), Yield: 9.0%

Next on our list is another attractive big-safe-dividend-paying BDC, Ares Capital. In our previous full report on Ares, we concluded that we liked the business, but were uncomfortable with the price because it was at the higher end of the historical range. However, since that time, and particularly over the last week, the price has come down, the dividend yield has gone up, and the business remains attractive. In particular, Ares has one of the longest investing tenures in the BDC industry (coupled with a consistent track record), as well as an ongoing history of stable income generation.

Some investors are highly cautious about investing in BDCs such as Ares because of the perceived risks associated with the middle market companies to which Ares provides financing. However, interestingly and worth noting, Ares has recently been securing its own financing by issuing investment grade bonds. And the investment grade status is a clear indication from the market that Ares’ business is stable and less risky than the high yield market and the middle market companies to which Ares in turn provides financing. Ares had been on our watchlist for some time before the price finally fell enough to warrant a buy, and the recent sell off is providing income-focused investors another bite at the the apple.

5. The WIlliams Companies (WMB), Yield:

Williams Companies Inc. is engaged in energy infrastructure business, primarily in the US. It owns and operates interstate natural gas pipelines and undertakes operations such as compression, processing, transmission. The Company’s assets handle close to 30% of US’ natural gas. The company announced healthy earnings and expectation beating revenues just two weeks ago, but the share price has gotten caught up in the indiscriminate selling.

The yield is steady backed by long-term fee based agreements, so the business has less near and intermediate-term exposure to commodity prices. Our last full report on WMB was in September (access that report here). The yield has risen significantly, creating an attractive entry point. We own these shares.

4. Nuveen Preferred & Income Fund (JPS), Yield: 6.8%

This is a healthy income-producing closed-end fund (“CEF”) that we currently own, and it is trading at a compelling discount to its net asset value (i.e. and attractive buying opportunity).

The fund primarily invests in investment grade preferred debt securities, convertible debt securities, and convertible preferred securities that are rated BBB/Baa or better by S&P, Moody's, or Fitch. It is designed specifically for income. And the recent sell off (and discount to NAV) is making for a very attractive buying opportunity.

3. Saratoga Investment Corp (SAR), Yield: 8.6%

The yield on this small (yet highly attractive) business development company has risen as the market has sold off indiscriminately.

The business is strong, and we like that the comp;any is able to benefit from multiple SBA licenses (which by the way is more beneficial to SAR than it would be to larger BDCs because they’re enough to meaningfully move the needle in a positive way for SAR). We continue to own shares of Saratoga, and you can read our previous full report here. Given the recent sell off, the shares currently present an attractive buying opportunity.

2. Energy Transfer (ET), Yield: 11.3%

Simply put, these shares are trading too low. The market hates anything in the energy sector right now, but it shouldn’t hate Energy Transfer considering its very steady fee based business with very little exposure to commodity prices.

We own these shares, and you can access our last full report on Energy Transfer here.

1. BlackRock Multi-Sector Income (BIT), Yield: 9.1%

If it is big safe yield (at a discounted price) that you are looking for, this closed-end fund is absolutely worth considering, especially after the recent sell-off. Not only does is trade at an attractive price (because of overly fearful selling), but the price is below Net Asset Value which makes this investment even more attractive.

The primary objective of the BlackRock Multi-Sector Income Trust (BIT) is to seek high current income, with a secondary objective of capital appreciation. We currently own these shares, and you can access our last full report here.

Takeaways:

The market has sold off hard over the last week, and no one knows where it is going next (if anyone tells you they can predict short-term market moves—they’re wrong—they cannot). However, we do know that disciplined, goal-focused, long-term investing has proven to be a winning strategy over and over again throughout history. We also know that a lot of big-dividend investments have sold off hard recently, thereby driving their dividend yields mathematically higher. We’re not suggesting anyone ditch their long-term investment strategy to try to take advantage of recent market volatility. However, we do believe it’s okay to get a little bit opportunistic as opportunities present themselves (so long as it’s consistent with your long-term goals), and the ideas we’ve highlighted in the article are particularly attractive right now (versus their prices last week, and their long-term value), and they’re worth considering for a spot in your prudently-diversified, long-term, income-focused investment portfolio.

Note: view all of our current holdings via our Portfolio Tracker here.