CyrusOne Inc. (CONE) offers an attractive investment opportunity for investors seeking steady growing dividend income (it’s raised the dividend 7 years straight) along with the strong potential for capital gains (the growth outlook is attractive) and a likely buyout (it will get acquired at a premium price…a good thing) in the relatively near future. A significant push into Europe has been a drag on margins which remains a near term concern (i.e. a buying opportunity!). This article reviews the health of the business, valuation, risks, dividend safety, and concludes with our opinion about why CONE is worth considering if you are an income-focused investor.

CyrusOne (CONE), Yield: 3.1% Yield

CyrusOne Inc. is a REIT specializing in owning, operating and developing enterprise-class, carrier-neutral, multi-tenant and single-tenant data center properties. CONE boasts of nearly 1,000 customers that include 200 of the Fortune 1000 companies and nearly half of the Fortune 20 (or private or foreign enterprises of equivalent size). CONE’s portfolio comprises 47 data centers and two recovery centers located in 13 markets which includes 10 cities in the US, Frankfurt, London and Singapore.

A data center is a physical facility that provides organizations with secure, reliable and robust environments to house their servers, critical applications and data. The data centers include multiple layers of physical security, scalable cabinet space availability, on-site trained staff (24x7x365), dedicated areas for customer care and equipment staging, power systems and other fault-tolerant infrastructure systems. They are designed to provide the space, power, cooling and network connectivity necessary to efficiently operate mission-critical IT equipment. Data center REITs own and manage these facilities. The demand for secure and reliable data storage has exploded in recent years and is expected to continue to remain very strong. This is fueling demand and growth for data center REITs.

Geographically Diverse Portfolio with High Quality Customer Base

Geographically, CONE has presence across the globe, but North America is its largest market accounting for ~93% of its total rent as of 3Q19. It has properties in six of the largest metropolitan areas in the US (New York, Chicago, Houston, Phoenix, San Antonio and Dallas) and five of the largest metropolitan areas for Fortune 500 headquarters (New York, Houston, Dallas, Chicago and Cincinnati). CONE also has six operational properties in international markets including three in London, two in Frankfurt, one in Singapore along with properties under development in Dublin and Amsterdam.

(source: Company Presentation)

Moreover, CONE’s main differentiation relative to other data center REITs is its focus on serving large customers primarily fortune 1000 or equivalent size. Currently, it serves nearly 1,000 customers including nine of the top ten cloud companies. Around 77% of its annualized rent comes from the Fortune 1000 or other companies of equivalent size. It serves diverse industries, including information technology, financial services, energy, oil and gas, mining, medical, research and consulting services and consumer goods and services.

Strong Development Pipeline Provides Growth Visibility

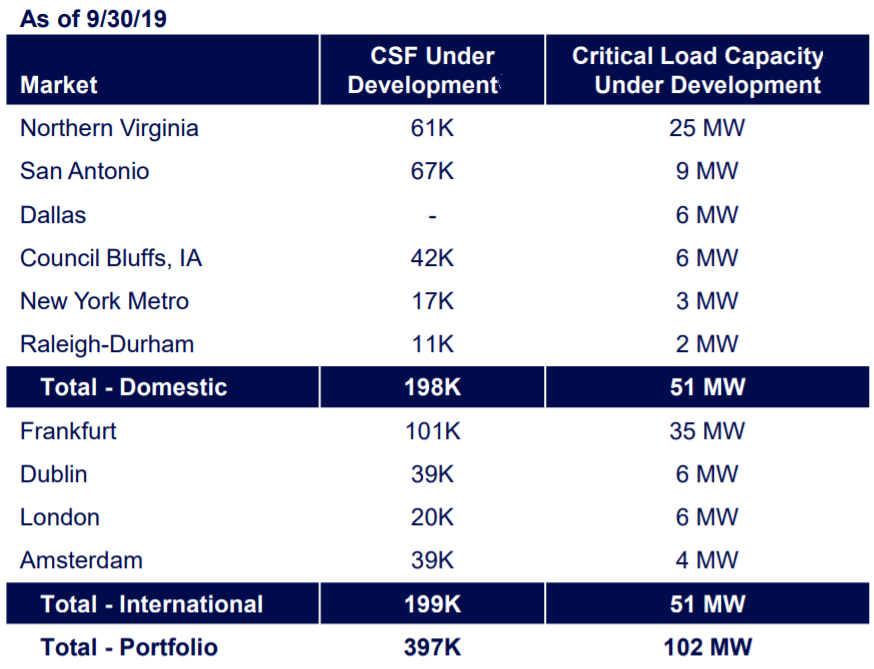

Given that CONE currently has the capacity of triple the size of its footprint with powered shell and land inventory, we believe it will experience significant growth in the years ahead. As of Q319, CONE had 1.7 million net rentable square feet (NRSF) of powered shell available for future development and approximately 489 acres of land that are available for future data center facility developments. Of which, 985K square feet of powered shell is currently under construction in Northern Virginia, San Antonio, Council Bluffs, Amsterdam, Dublin, Frankfurt and London. These development projects expected to deliver 397K CSF and 102 MW of power across both domestic and international markets. We note that the current development properties and available acreage were selected with a focus on markets with a strong presence of and high demand by Fortune 1000 companies and providers of cloud services. As a result, we believe that CONE’s development portfolio contains properties that are located in markets with attractive supply and demand conditions and that possess suitable sought after physical characteristics to support data center infrastructure.

(source: Company Presentation)

Robust Leasing Activity

3Q19 represented a robust leasing quarter for CONE, as the company signed leases totaling 35 MW and $52 million in annualized revenue, more than double the prior 4-quarter average. Notably, CONE’s leases were geographically diverse, including a significant impact from Europe. European performance as a whole performed far ahead of expectations, with revenues growing +81% yoy, and $40 million (40% of CONE’s total YTD bookings) in annualized revenue signed. Additionally, the company had significant success in leasing to enterprises and in Q319 it signed a record $23 million in annualized revenue to enterprise customers, which is 40% above the prior record. The growth in enterprise sales is particularly encouraging as the hyper-scale companies slowed their purchases in recent times. Management noted in their recent Q3 earnings call:

“We expect continued strong growth from enterprises in the coming years and are better positioned to capitalize on this demand than many other providers, especially as we now have a much larger international footprint.”

Expanding European Footprint to Capture Growing Demand

The company’s European business has taken off and we expect it to grow further given CONE’s significant expansion plans in the region. Regarding Europe’s performance during Q3, management noted the following:

“Europe, revenue grew 81% year-over-year and is now $70 million on an annualized run rate basis, which is nicely ahead of our expectations.”

CONE has a robust pipeline of data center development projects currently under construction in Frankfurt, London, Ireland and Netherlands which will increase the size of portfolio in Europe by nearly 50% to 150 MW compared to ~97 MW currently. This will represent ~17% of CONE’s total global footprint. There is substantial growth opportunity in Europe with significant demand from existing hyperscale customers. Additionally, the company’s sales force is pursuing local enterprises with an expected contribution over time similar to the US. Management expects Europe to be about 25% of its total revenue in 3 years.

Important to note, the significant push into Europe has elevated SG&A expenses which has been a drag on margins and is likely to remain so in the near term. We view this as an attractive buying opportunity because once the expansion is complete, we expect it to positively contribute toward both topline and bottom line growth.

(source: Company Presentation)

Favorable Industry Fundamentals Driving Demand for Data Centers

Fundamentals for data center real estate remain strong, supported by trends that particularly favor data center assets, including the exponential growth in global data, the growth of e-commerce and demand for outsourcing of data storage and cloud-based applications. CONE noted that it expects continued economic growth in the markets it operates in, which should result in ongoing positive demand for data center space as companies expand and upgrade information system platforms.

In the past, most enterprises opted to keep their data center requirements in-house. However, current trends are leading more enterprise chief information officers (CIOs) to either outsource their data center requirements, and use carrier-neutral colocation facilities. The global colocation data center market is expected to grow at a ~8.4% CAGR till 2023 to reach ~$38.8 billion versus $25.5 billion in 2018, according to market research firm IHS Markit. This will be driven by accelerating data growth from cloud providers and changing enterprise IT spending trends as traditional companies begin deploying hybrid IT infrastructures.

Large hyperscale cloud service providers (CSPs) such as Amazon, Google and Microsoft delivered ~35% growth in capex data center spending in 3Q19, investing ~$27 billion on building new and expanding centers as well as the products. The pace of data center capex spending by hyperscale operators is expected to continue going forward. CONE’s CEO Gary Wojtaszek also noted a significant opportunity in hyperscale CSPs during Q3 call:

“We expect that demand from hyper-scalers will begin to increase toward the second half of 2020 and we expect these companies will continue to contribute significantly to our growth as we expand internationally.”

The Internet of Things, 5G, autonomous vehicles and artificial intelligence are some other trends which are driving unprecedented growth of the digital economy, thereby driving demand for data centers.

Strong Relative Performance versus Key Competitors

CONE has outperformed across its Blue-Chip REIT peers and Data Center REIT peers during 3Q19 and is well positioned to maintain similar trajectory going forward. When compared across parameters such as revenue growth, EBITDA growth and FFO per share growth, CONE stood tall leading both Blue-Chip REIT and Data Center REIT universe. CONE is growing in the 20% range across all of its key financial metrics, which is 3 times faster than its direct peers and substantially faster than other REITs. The company noted that prior investments in business, specifically in boosting sales and operational capabilities is driving the outperformance compared to other REITs.

(source: Company Data)

Financial Strength – A Competitive Advantage

CONE achieved investment grade status during Q319 which will result in investment-grade index eligibility and improving access to capital at attractive rates. S&P upgraded CORE’s rating to BBB-minus a year ago and Fitch initiating coverage recently with the BBB-minus rating as well. With this, the company now has the 2 ratings needed for investment-grade index eligibility. The easy access to capital is important in a capital-intensive business such as CONE’s as it positions the company to continue to take advantage of strong secular demand trends in coming years. Unlike the high-yield market, the investment-grade bond market never shuts down, and in periods of economic distress or recession, it will give competitive advantage by providing access to capital to opportunistically acquire assets at discounted prices. CONE also noted that the investment grade status ensures estimated interest rate savings of ~50-100 bps compared to high yield market, resulting in higher normalized FFO per share. This equates to $5-10 million in annual interest savings for every $1billion in incremental debt or 4-9 cents per share based on Q319 share count.

As seen in the figure below, there is no debt maturity untll 2023 and CONE has ~$1.25 billion in available liquidity.

(source: Company Presentation)

Valuation:

On a Price to Adjusted Funds from Operations basis (“AFFO”) basis, CONE is inexpensive relative to its peer group average. As seen below, CONE trades at P/AFFO multiple of 16.8x, which is ~17% discount to its peer group average multiple of ~20.3x. This despite its strong growth prospects wherein it is forecasted to be the fastest growing (both in terms of revenue and EBITDA) data center REIT in 2020. In our view, the discount should narrow given CONE’s strong growth potential. This should result in strong capital gains for investors.

(source: Thomson Reuters)

Dividend Safety:

We note that CONE has delivered strong annual dividend growth since its IPO in 2013, raising its dividend for the last seven consecutive years. The dividend has grown from $0.64 in 2013 to $1.92 in 2019 representing a CAGR of ~17% during 2013-2019 and. At today’s price near $64.86, CONE’s current yield equates to ~3.08%. The company estimates its normalized FFO payout ratio to be ~54% for this year. The normalized FFO is expected to register a growth of ~8% for 2019 and another 10% in 2020 as per analyst estimates taken from Thomson Reuters. This suggests that CONE should be able to raise the dividend again next year. CONE has no debt maturing until 2023 which provides it with ample cash flow to not only pay its dividend but continue to raise it over time. This makes us conclude that CONE’s dividend is safe, and we are likely to see meaningful increases over time. This makes the stock attractive for those seeking current income and dividend growth.

(source: Company Data)

A Potential Buyout Target

CONE is a potential buyout target, and this is a good thing for investors. Specifically, scale is an advantage in the data center world, and CONE is still relatively small relative to some peers (for example Digital Realty and Equinox). And as larger peers look to grow, they look to smaller players as acquisition targets. For example, the share price of CONE got a strong bump months ago when it was reported as a potential buyout target, but the shares have since declined in value again, thereby adding a margin of safety for investors in our view. Given the competitive environment, we expect that CONE will eventually get acquired at a premium price by a larger peer, whereby shareholders would receive a significantly higher price for their existing CONE shares. And even if CONE doesn’t get acquired, it remains an attractive, long-term, dividend-growth investment.

Risks:

Technology disruption: The current market environment is favorable for data center operators as enterprise and IT customers continue to outsource and decentralize their IT operations. We acknowledge that this could reverse, pushing companies back to sourcing their own requirements internally, thereby decreasing demand for data center space.

Reduction in IT spending: A worldwide recession could cause businesses to suddenly reduce their spending on IT infrastructure. Any reduction in IT spending could reduce demand for outsourced data center spaces which could adversely impact CONE’s operations.

Dilution Risk: Higher-than-expected investment to support the Europe expansion raises concern about higher level of equity dilution, which could negatively impact shareholders’ return. However, with investment grade status the accessibility to debt markets will improve and dilution risk should abate.

Competition: CONE competes with numerous data center providers, many of whom own properties similar to CONE in the same metropolitan areas. Many of these competitors have developed and continue to develop additional data center space. If the supply of data center space continues to increase as a result of these activities or otherwise, rental rates may be reduced which will negatively impact operating results.

Conclusion:

CyrusOne Inc. is a data center REIT focused on serving large enterprise specifically Fortune 1000 companies. CONE offers a very attractive dividend yield of 3.1% (especially considering its continuing track record of dividend growth) along with strong potential for capital appreciation, as well as the potential for a very sharp share price increase if it becomes the acquisition target of a larger REIT. The stock is trading at discount to its peer group average despite being the fastest growth data center REIT compared to its peers. The market is skeptical in light of elevated SG&A expenses to ramp European operations which are likely to be a drag on margins (we view this as a buying opportunity). However, execution from the management team has been solid thus far as evidenced by strong growth in European operations. We see the concerns as overblown, and in or view current levels provide long-term income focused investor with a very attractive entry point.