Overview:

Omega Healthcare Investors (OHI) is a big dividend (7.2% yield) REIT that focuses on skilled nursing facilities. The last year has been volatile for Omega as it suspended its customary dividend increases in order to work through challenges related to the draconian financial pressures faced by several of its property operators/tenants. However, it appears Omega has resolved its biggest operator challenge, and is now positioned to soon return to growth (both funds from operations (FFO) and dividend growth) pending any near-term setbacks. After reviewing Omega’s big risks, this article considers what could actually go right for the REIT, and concludes with our views on the viability of Omega as an income-producing investment.

Recent Share Price Performance and Commentary:

As a general rule, REITs are not supposed to be very volatile investments because of their attractive steady income payments. However, here is a look at the recent wild ride for Omega’s share price.

Most of the volatility was due to challenges faced by Omega’s property operators, as we wrote about in detail HERE and HERE. In a nutshell, operators have been under pressure to cut costs because reimbursement rates (both private insurers and particularly Medicaid) have not been rising as fast as costs/healthcare inflation.

But according to this week’s quarterly earnings conference call, Omega’s most troubled operator (Orianna) has finally been resolved. According to CEO Taylor Pickett:

“All of the 42 Orianna facilities have been transitioned or sold” and “Consistent with all of our prior estimates, final rent and rent equivalent received from the Orianna portfolio is approximately $33 million.”

This is a very good thing because it removes a big uncertainty investors were concerned with. Further, Pickett went on to say:

“We're for sure we're going to be net acquirers in a meaningful way in 2019.”

Omega isn’t out of the woods yet (for example operator “Daybreak” is still a big troubled concern, more on this later), but a return to net acquisitions could bode very well for the future of Omega’s stock price and the eventually return to dividend increases.

What Are The Big Risks?

However, before we start celebrating the “all clear” for Omega, it’s worthwhile to consider several of the big risks that this healthcare REIT still faces. For example…

Legal Costs have been significantly larger than expected lately and a drag on earnings. Specifically, the lawyers have gotten involved with the distressed operator challenges. According to the quarterly call, legal costs were a detractor. Specifically:

“Our adjusted FFO of $0.73 per share is $0.04 less than our third quarter adjusted FFO of $0.77 per share. The difference consists of approximately $0.02 per share for increased legal costs related to the conclusion of the Orianna work-up and non-executive employee bonuses related to a three-year incentive plan payout and approximately $0.02 per share related to uncollected Daybreak obligations.”

As Omega continues to work through more operators challenges, legal fees will likely continue to be a detractor. The good news is that these expenses are largely “one time” in nature, and once they’re over, they’re not expected to repeat.

More Distress (Daybreak): Orianna has been the biggest thorn in Omega’s side, but Daybreak is another operator posing challenges. During the call, analysts asked more than half a dozen times about the risks of Daybreak (another significant operator struggling financially) and what difficulties it could bring. Management remained confident that they’d work through the challenges, but it’s a significant risk factor to keep on your radar. The good news is that long-term demographics (an aging population with growing healthcare needs) are on Omega’s side, and reimbursement rates (particularly in Texas) are expected to show a little more slack for operators. Further still, despite all the negativity, Omega worked through the Orianna situation to a reasonable conclusion, thereby giving us some increased confidence for Daybreak.

Bad Property Acquisitions pose another risk to be aware of. Just because Omega expects to be a net acquirer of properties in 2019, that’s no guarantee that they’ll all be great investments. Per the call, the yield range on the properties being acquired in the market will be around 9%. This gives a good indication that they’re risky (they yield a lot more than US treasuries, for example). And if property spreads blow out further, that could create growing challenges for Omega. The good news remains that healthcare reimbursement rates will eventually rise (just not as fast as operators want) and demographics will also help.

The Upcoming MedEquities Acquisition poses another risk. Med Equities (MRT) is a healthcare REIT that Omega expects to acquire in 2019. Acquisitions always pose a variety of risks ranging from over paying, to integration challenges, to the risk of the deal falling apart. Omega is already counting on revenue from MedEquities in the 2019 FFO guidance they’ve provided, so if the deal falls apart, that could impact Omega’s FFO negatively.

High Debt and High Payout Ratios pose another risk for Omega. For example, per the quarterly call:

“Approximately 80% of our $4.6 billion in debt, is fixed and our net debt to adjusted annualized EBITDA was 5.5 times and our fixed charge coverage ratio was 3.8 times.”

And while that is a significant amount of debt, management notes that

“When adjusting for Orianna and the Daybreak, fourth quarter cash shortfall the known revenue on the new builds and removing revenue related to our fourth quarter asset sales our pro forma leverage would be roughly 5.17 times.”

Better, but still a lot of leverage, especially considering the riskiness of the assets (high debt levels could further postpone dividend increase even if/when Omega returns to growth).

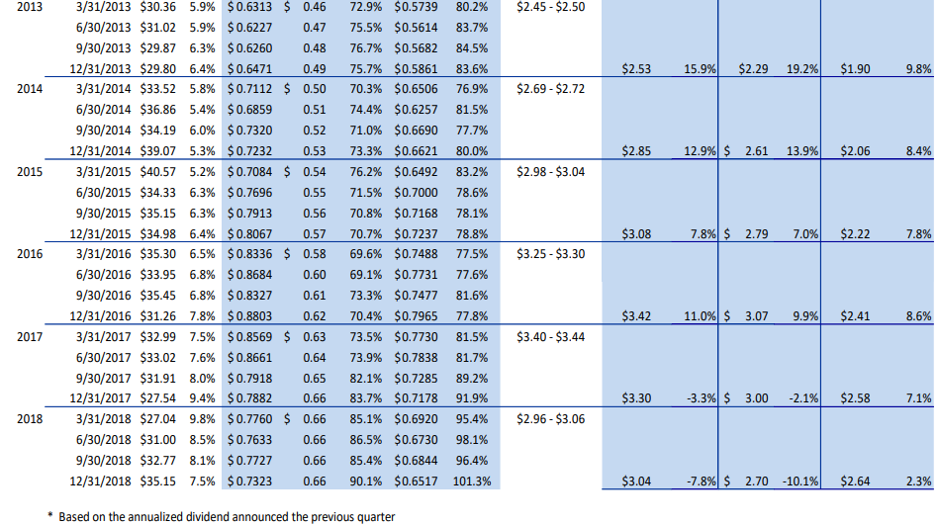

From a dividend payout perspective, the margin of safety on the dividend has decreased, as shown in the following table.

As the table shows, in recent quarters, the FAD and AFFO payout ratios have increased. The good news is that a lot of that increase is due to temporary challenges, which are being resolved (such as one time legal expenses related to Orianna), and Omega expects to return to growth, eventually.

What Could Go Right?

With all the uncertainty and volatility surrounding Omega, it can be a worthwhile exercise to consider what could actually go right.

Valuation Expansion: A quick look at the table above shows that Omega is relatively inexpensive on a price to Adjusted Funds From Operations (“AFFO”) basis, relative to its own history. Granted, relative to 2019 estimates, the shares are not the cheapest they’ve ever been, but they are still relatively attractively priced, in our view. Obviously, part of the reason for the relatively low price to AFFO ratios is the perceived risk. But of course, as a contrarian value investor, the best time to buy is usually when prices are lower (not higher). Management has proven their ability and skill in working through challenging market conditions.

A Return to Growth: Omega’s 2019 outlook is solid (2019 AFFO guidance is $3.00 to $3.12). And beyond 2019, assuming the reimbursement challenges will eventually stabilize, and assuming the demographics will continue to be on Omega’s side, there is plenty of room for long-term growth, significant share price increases, and the eventual resumption of healthy dividend increases. As we mentioned earlier, management expects to once again be a net acquirer of properties—a good sign for growth.

Future Dividend Increases: Omega wants to grow the dividend. It’s been stuck at $0.66 per quarter for over a year as management works through the risks and challenges described above. We believe management will eventually resume regular dividend increases, and we don’t expect any dividend cuts. Once management finishes working through current operator challenges, they’ll start paying down debt, building up the margin of safety on dividend payout ratios, and eventually start increasing the quarterly dividend again. And the share price will rise significantly right along with it.

Conclusion (How We’re Playing It):

As many of our readers know, after owning Omega for many months, we recently had the shares called away from us at $38 as part of an income-generating covered call option that we sold. We followed that trade with another one… we subsequently sold income-generating put options last month with a strike price of $36 and an expiration date of February 15th. Those shares may well get put to us before they expire this week, depending on how the share price moves. If the shares don’t get put to us, we’ll give some serious consideration to buying the shares outright, or perhaps selling more income-generating put options which will give us another chance to own Omega at an even lower price (we’d consider selling March or April puts, roughly 5-10% below the current market price). As a reminder, the premium income available in the options market is higher than normal for Omega because of the volatility and uncertainty.

If you can look past the near-term volatility and uncertainty, Omega is an attractive leader in the skilled nursing facilities REIT industry supported by long-term demographics and ongoing reimbursement rate increases from insurers (albeit lower increases than Omega and its operators would prefer). And the REIT structure allows investors to keep collecting big steady dividend payments. The recent post-earnings-announcement sell-off has created an increasingly attractive entry point for long-term income-focused investors, in our view.