This stable, growth-oriented, industrial REIT, is trading at an attractive discount. Not only does it have long-term leases with investment-grade tenants at attractive rentals, but it’s also offering an attractive 4.4% dividend yield—significantly higher than peers. In this report, we analyze the company’s income profile, growth and dividend prospects, and finally conclude with our opinion about investing in this attractive opportunity from a risk versus reward perspective.

Overview:

Monmouth Real Estate Investment Corp (MNR) is an industrial REIT. It owns Industrial buildings which it leases out primarily to investment-grade tenants. It earns revenue primarily from rental operations which include rent and revenue reimbursement. MNR has over 22 million square feet of area available for lease and over 99% has been occupied by tenants. It currently has 114 properties located across the United States with a focus in Florida and Texas. The average lease expiration term is 7.6 years, and the average rent per square feet is around $6.25. FedEx is Monmouth’s largest tenant (with 47% of the total leasable square footage leased out to Fedex and its subsidiaries). Fedex and related entities account for approximately 60% of the company’s total revenue. While a single customer accounting for 60% is an unusually high customer concentration, the leases are long term in nature with an investment grade client, thereby providing significant stability.

Source: Monmouth Real Estate Investment Corporation

Industrial REITs – An attractive sub-space in the REIT world

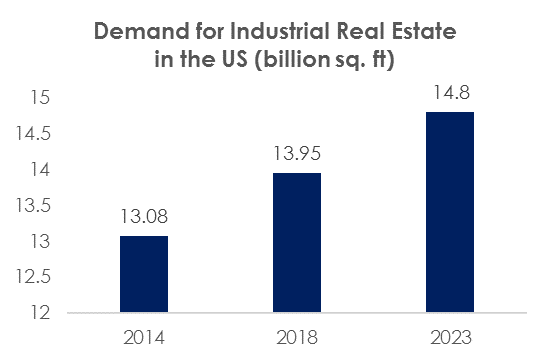

Industrial REITS have been the fastest growing sub-industry of the vast REIT space as a result of secular growth in supply chain investments driven by online retail and digital transformation in traditional industries.

source: WSJ

source: NAREIT T-Tracker

As mentioned above, the demand for supply chain assets in the US is being driven significantly by robust growth in e-commerce as well as an increased desire on the part of traditional businesses to offer faster, more reliable, last mile delivery to customers. While the organic growth trends of Fedex have lost some momentum in the near term, the company’s medium to long term growth prospects are solid driven by strong growth in online retail, and it will continue to make investments in its infrastructure.

source: Pitney Bowes Parcel Shipping Index

source: eMarketer

MNR outperforms its industry on rentals and occupancy levels

Monmouth’s average rental per square footcoutperforms the market. As evident in the chart below, the company’s average rent per sq. ft of $6.25 is in the top quartile of the industrial REIT sector. Additionally, average occupancy in the overall Industrial REIT sector in the US in FY 19 was 96.1%. Comparatively, MNR has continuously reported better occupancy numbers of above 98%.

(Source: NAREIT, Cushman & Wakefield Research and Individual Company Reports)

Further, MNR primarily strikes long-term leases for its properties with Investment grade tenants. This allowed MNR to report much lower declines in rentals than the rest of the industry during the last downturn. Not surprisingly, the company was one of the outstanding REITs that did not cut its dividend during the 2008/09 recession. On the flip side, the company’s growth in rent per sq. can also be more muted than its more volatile peers.

(Source: Company Reports, JLL)

Scaling up through acquisitions:

MNR has been in an expansionary mode for the last five years. Management has been focusing on acquiring new properties funded by a mix of stock and debt. Over the last five years, total asset base has grown at a CAGR of 20%. The company must regularly raise capital in order to expand because they pay out 90% of the funds generated from operations as dividends. The growth of assets has led to CAGR in Fund Flow of Operations (FFO) of more than 22% during the same period. In the past year, the number of properties increased from 111 to 114 with an increase in total square foot leasable area of over 1 million.

(Source: Monmouth Real Estate Investment Corporation, Company reports)

In FY19, Fund flow from Operations (FFO) reported a jump of over 16% year-over-year. Despite the increase, FFO per share declined marginally in FY 19. This was due to issuance of 9.2 million shares by the company last year. It also raised around $60 million through preference share allotment. The company will not likely issue more equity in 2020 and at the same acquisitions in the pipeline should add to FFO per share. The company has a consistent history of FFO and dividend per share growth over the last few years as evident in the chart above.

Sustained growth in dividends at attractive yields:

MNR has maintained consistency in dividend per share over the last nearly 3 decades. The company is currently providing a dividend yield of 4.4% to its investors which is considerably more than the NAREIT index and especially more than the dividend yield offer by the industrial REIT sector as a whole. Typically, industrial REITs have offered lower yields due to faster FFO growth and acquisition activity they have exhibited. In this context, MNR’s 4.4% yield is highly attractive in our opinion. Finally, an analysis of the dividend yields of competitors and MNR indicates that the yield gap between the company and peers has expanded recently, providing an opportunity to take exposure to the company at an attractive relative valuation.

(Source: NAREIT)

Risks:

Customer concentration…

MNR is substantially dependent upon FedEx for revenue. The company leases out close to 47% of its space and generate around 60% of its revenue from Fedex. Strategic and operational changes at Fedex could have real ramifications for the company. Having said that, given the company’s average remaining lease term of around 7.6 years, we believe in practical terms, the associated risks are minimal in the near to medium time frame.

Demand and Supply Imbalance…

Over the last several years, warehouse and distribution real estate market has been tight with limited inventory available in the market. The limited supply has been good for industrial REITs. However, as with any industry, optimism in the market is leading to new supply and if supply ends up surpassing demand in a significant way, there will be pressure on rentals. Again, MNR’s long term lease contracts will allow the company to better navigate a difficult market than the industry.

Conclusion:

Monmouth operates in an attractive sub-space of the REIT industry (Industrials) with ample opportunities to grow its asset base and income steam. The company primarily has investment grade clients and has inked long term leases at attractive rentals. At the same time, the company’s 4.4% dividend yield leads its peers and even the overall REIT average despite a consistent history of growth. While the company does employ more leverage than peers, the quality of its assets, clients and contracts offsets risks that arise out of financial leverage. If you are looking for an attractive, healthy-dividend, growing REIT to add to your portfolio, Monmouth offers a compelling risk-versus-reward opportunity, and a very nice yield.